NEED HELP WITH QUESTIONS 5 - 11

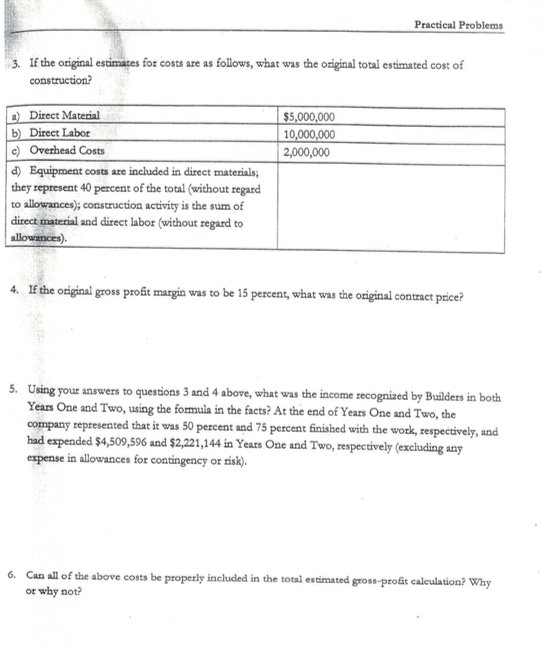

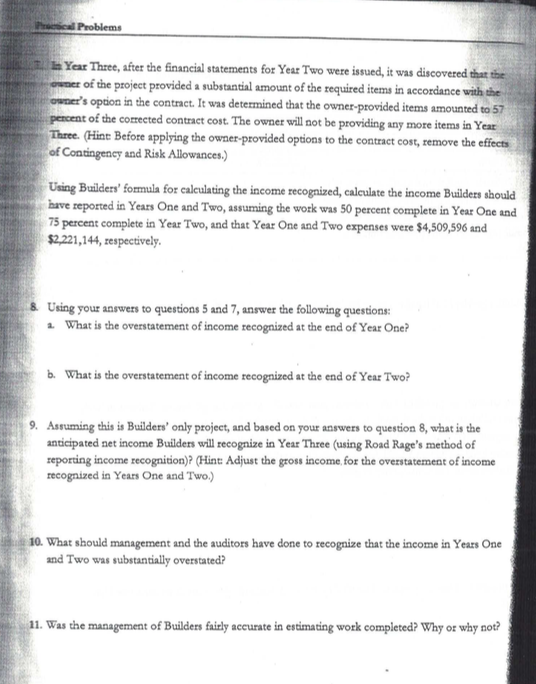

Practical Problems VII. PRACTICAL PROBLEMS Practical Problem 1 Read and complete the following exercise Road Rage, Inc., is in the business of designing, constructing, and inspecting highways. Road Rage has three wholly owned subsidiary companies, each of which performs one of the functions mentioned above. These three subsidiaries are Engineering, Inc.; Builders, Inc.; and Inspectors, Inc. Road Rage is a publicly held company and files consolidated financial statements. In 20X1, Road Rage, through its subsidiary, Builders, Inc. (Builders), signed a fixed price contract for the construction of an interstate highway. The project was to be completed three years hence. All of the long-term projects of Builders (greater than one year) are reported on the percentage-of-completion method of accounting Under the terms of the contract, Builders was to provide all the necessary equipment, machinery, and materials. However, the contract gave the owner of the project the option to furnish some of the necessary items itself and to reduce the contract costs and gross margin appropriately. The contract required Builders to obtain property and personal injury liability insurance. In addition, the contract provided that any costs arising from changes in governmental regulations would be reimbursed fully by the owner of the project. Builders recognized income in each of the first two years of the contract based on the following formula: Fixed contract price Total costs of construction Total estimated gross profit Estimated percentage of work completed Year-to-date gross profit Prior year-to-date gross profit Actual.costs for period Income recognized in current period Total costs of construction were based on the following: Practical Problems 1. Direct material 2. Direct labor 3. Overhead costs 4. Equipment design allowance: anticipated routine design changes in the development process and mechanical specifications (3 percent of equipment costs) 5. Conceptual design allowance: normal growth during the engineering design phase (15 percent of material and labor costs) 6. Construction quantity allowance material and labor associated with anticipated concrete waste and overpour, piping drop-offs and waste, insulation fabrication cut-offs, and other damages (5 percent of construction activity accounts) 7. Escalation allowance: cost increases due to anticipated inflation (12 percent of equipment costs plus 15 percent of construction activity accounts 8. Contingency allowance: unforeseeable costs due to human error in the estimation process (2.9 percent of base costs of construction) 9. Risk allowance costs of unforeseeable events such as labor disputes, unusually bad weather, runaway inflation, or changes in govemmental regulations (4 percent of base cost of contract) The base cost of the contract included items 1 through 3 above. Items 4 through 7 were identified with particular items of work Road Rage did not bid for the contract for this project and therefore, represents that it would not inflate projected costs unnecessarily. Builders has only constructed one bridge prior to this contract. All of the allowances in the estimated contract costs are within the normal industry standards. Questions: 1. Is the percentage of completion method of accounting proper for this project? a. If so, why? b. State the primary requirement that must be met in order for a company to use the percentage-of- completion method of accounting, 2 Is Builders' method of recognizing income for the current period correct? Practical Problems 3. If the original estimates for costs are as follows, what was the original total estimated cost of construction? $5,000,000 10,000,000 2,000,000 2) Direct Material b) Direct Labor c) Overhead Costs d) Equipment costs are included in direct materials; they represent 40 percent of the total (without regard to allowances), construction activity is the sum of direct material and direct labor (without regard to allowances) 4. If the original gross profit margin was to be 15 percent, what was the original contract price? 5. Using your answers to questions 3 and 4 above, what was the income recognized by Builders in both Years One and Two, using the formula in the facts? At the end of Years One and Two, the company represented that it was 50 percent and 75 percent finished with the work, respectively, and had expended $4,509,596 and $2,221,144 in Years One and Two, respectively (excluding any expense in allowances for contingency or risk). 6. Can all of the above costs be properly included in the total estimated gross-profit calculation? Why or why not? cel Problems is Year Three, after the financial statements for Year Two were issued, it was discovered that the owner of the project provided a substantial amount of the required items in accordance with the owner's option in the contract. It was determined that the owner provided items amounted to 57 percent of the corrected contract cost. The owner will not be providing any more items in Year Three. (Hint Before applying the owner-provided options to the contract cost, remove the effects of Contingency and Risk Allowances.) Using Builders' formula for calculating the income recognized, calculate the income Builders should have reported in Years One and Two, assuming the work was 50 percent complete in Year One and 75 percent complete in Year Two, and that Year One and Two expenses were $4,509,596 and $2,221,144, respectively. & Using your answers to questions 5 and 7 answer the following questions 1 What is the overstatement of income recognized at the end of Year One? b. What is the overstatement of income recognized at the end of Year Two? 9. Assuming this is Builders' only project, and based on your answers to question 8, what is the anticipated net income Builders will recognize in Year Three (using Road Rage's method of reporting income recognition) (Hint: Adjust the gross income for the overstatement of income recognized in Years One and Two.) 10. What should management and the auditors have done to recognize that the income in Years One and Two was substantially overstated? 11. Was the management of Builders fairly accurate in estimating work completed? Why or why not? Practical Problems VII. PRACTICAL PROBLEMS Practical Problem 1 Read and complete the following exercise Road Rage, Inc., is in the business of designing, constructing, and inspecting highways. Road Rage has three wholly owned subsidiary companies, each of which performs one of the functions mentioned above. These three subsidiaries are Engineering, Inc.; Builders, Inc.; and Inspectors, Inc. Road Rage is a publicly held company and files consolidated financial statements. In 20X1, Road Rage, through its subsidiary, Builders, Inc. (Builders), signed a fixed price contract for the construction of an interstate highway. The project was to be completed three years hence. All of the long-term projects of Builders (greater than one year) are reported on the percentage-of-completion method of accounting Under the terms of the contract, Builders was to provide all the necessary equipment, machinery, and materials. However, the contract gave the owner of the project the option to furnish some of the necessary items itself and to reduce the contract costs and gross margin appropriately. The contract required Builders to obtain property and personal injury liability insurance. In addition, the contract provided that any costs arising from changes in governmental regulations would be reimbursed fully by the owner of the project. Builders recognized income in each of the first two years of the contract based on the following formula: Fixed contract price Total costs of construction Total estimated gross profit Estimated percentage of work completed Year-to-date gross profit Prior year-to-date gross profit Actual.costs for period Income recognized in current period Total costs of construction were based on the following: Practical Problems 1. Direct material 2. Direct labor 3. Overhead costs 4. Equipment design allowance: anticipated routine design changes in the development process and mechanical specifications (3 percent of equipment costs) 5. Conceptual design allowance: normal growth during the engineering design phase (15 percent of material and labor costs) 6. Construction quantity allowance material and labor associated with anticipated concrete waste and overpour, piping drop-offs and waste, insulation fabrication cut-offs, and other damages (5 percent of construction activity accounts) 7. Escalation allowance: cost increases due to anticipated inflation (12 percent of equipment costs plus 15 percent of construction activity accounts 8. Contingency allowance: unforeseeable costs due to human error in the estimation process (2.9 percent of base costs of construction) 9. Risk allowance costs of unforeseeable events such as labor disputes, unusually bad weather, runaway inflation, or changes in govemmental regulations (4 percent of base cost of contract) The base cost of the contract included items 1 through 3 above. Items 4 through 7 were identified with particular items of work Road Rage did not bid for the contract for this project and therefore, represents that it would not inflate projected costs unnecessarily. Builders has only constructed one bridge prior to this contract. All of the allowances in the estimated contract costs are within the normal industry standards. Questions: 1. Is the percentage of completion method of accounting proper for this project? a. If so, why? b. State the primary requirement that must be met in order for a company to use the percentage-of- completion method of accounting, 2 Is Builders' method of recognizing income for the current period correct? Practical Problems 3. If the original estimates for costs are as follows, what was the original total estimated cost of construction? $5,000,000 10,000,000 2,000,000 2) Direct Material b) Direct Labor c) Overhead Costs d) Equipment costs are included in direct materials; they represent 40 percent of the total (without regard to allowances), construction activity is the sum of direct material and direct labor (without regard to allowances) 4. If the original gross profit margin was to be 15 percent, what was the original contract price? 5. Using your answers to questions 3 and 4 above, what was the income recognized by Builders in both Years One and Two, using the formula in the facts? At the end of Years One and Two, the company represented that it was 50 percent and 75 percent finished with the work, respectively, and had expended $4,509,596 and $2,221,144 in Years One and Two, respectively (excluding any expense in allowances for contingency or risk). 6. Can all of the above costs be properly included in the total estimated gross-profit calculation? Why or why not? cel Problems is Year Three, after the financial statements for Year Two were issued, it was discovered that the owner of the project provided a substantial amount of the required items in accordance with the owner's option in the contract. It was determined that the owner provided items amounted to 57 percent of the corrected contract cost. The owner will not be providing any more items in Year Three. (Hint Before applying the owner-provided options to the contract cost, remove the effects of Contingency and Risk Allowances.) Using Builders' formula for calculating the income recognized, calculate the income Builders should have reported in Years One and Two, assuming the work was 50 percent complete in Year One and 75 percent complete in Year Two, and that Year One and Two expenses were $4,509,596 and $2,221,144, respectively. & Using your answers to questions 5 and 7 answer the following questions 1 What is the overstatement of income recognized at the end of Year One? b. What is the overstatement of income recognized at the end of Year Two? 9. Assuming this is Builders' only project, and based on your answers to question 8, what is the anticipated net income Builders will recognize in Year Three (using Road Rage's method of reporting income recognition) (Hint: Adjust the gross income for the overstatement of income recognized in Years One and Two.) 10. What should management and the auditors have done to recognize that the income in Years One and Two was substantially overstated? 11. Was the management of Builders fairly accurate in estimating work completed? Why or why not