Answered step by step

Verified Expert Solution

Question

1 Approved Answer

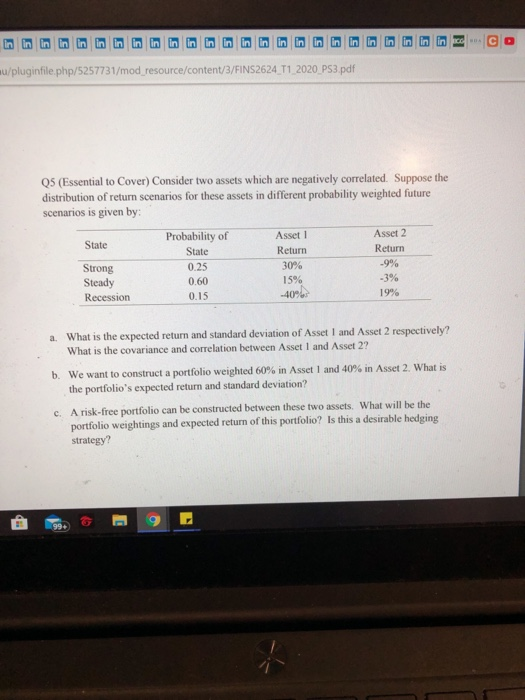

need help with this question pls /pluginfile.php/5257731/mod_resource/content/3/FINS2624_T1_2020 PS3.pdf Q5 (Essential to Cover) Consider two assets which are negatively correlated Suppose the distribution of retum scenarios

need help with this question pls

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

QlikView For Finance

Authors: B. Diane Blackwood

1st Edition

1784395749, 978-1784395742