Answered step by step

Verified Expert Solution

Question

1 Approved Answer

need solution for C,D and E. please explain in details. It is very urgent C. Consider an FRA that: Expires/settles in 30 days. Is based

need solution for C,D and E. please explain in details. It is very urgent

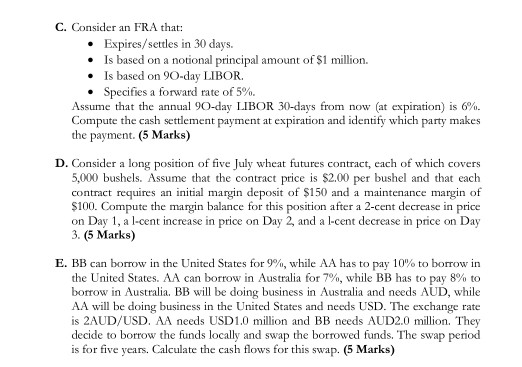

C. Consider an FRA that: Expires/settles in 30 days. Is based on a notional principal amount of $1 million. Is based on 90-day LIBOR. Specifies a forward rate of 5%. Assume that the annual 90-day LIBOR 30-days from now (at expiration) is 6%. Compute the cash settlement payment at expiration and identify which party makes the payment. (5 Marks) D. Consider a long position of five July wheat futures contract, each of which covers 5,000 bushels. Assume that the contract price is $2.00 per bushel and that each contract requires an initial margin deposit of $150 and a maintenance margin of $100. Compute the margin balance for this position after a 2-cent decrease in price on Day 1, a l-cent increase in price on Day 2, and a l-cent decrease in price on Day 3. (5 Marks) E. BB can borrow in the United States for 9%, while AA has to pay 10% to borrow in the United States. AA can borrow in Australia for 7%, while BB has to pay 8% to borrow in Australia. BB will be doing business in Australia and needs AUD, while AA will be doing business in the United States and needs USD. The exchange rate is 2AUD/USD. AA needs USD1.0 million and BB needs AUD2.0 million. They decide to borrow the funds locally and swap the borrowed funds. The swap period is for five years. Calculate the cash flows for this swap. (5 Marks) C. Consider an FRA that: Expires/settles in 30 days. Is based on a notional principal amount of $1 million. Is based on 90-day LIBOR. Specifies a forward rate of 5%. Assume that the annual 90-day LIBOR 30-days from now (at expiration) is 6%. Compute the cash settlement payment at expiration and identify which party makes the payment. (5 Marks) D. Consider a long position of five July wheat futures contract, each of which covers 5,000 bushels. Assume that the contract price is $2.00 per bushel and that each contract requires an initial margin deposit of $150 and a maintenance margin of $100. Compute the margin balance for this position after a 2-cent decrease in price on Day 1, a l-cent increase in price on Day 2, and a l-cent decrease in price on Day 3. (5 Marks) E. BB can borrow in the United States for 9%, while AA has to pay 10% to borrow in the United States. AA can borrow in Australia for 7%, while BB has to pay 8% to borrow in Australia. BB will be doing business in Australia and needs AUD, while AA will be doing business in the United States and needs USD. The exchange rate is 2AUD/USD. AA needs USD1.0 million and BB needs AUD2.0 million. They decide to borrow the funds locally and swap the borrowed funds. The swap period is for five years. Calculate the cash flows for this swapStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ACC 120 Wake Tech Financial Accounting W Connect Plus Access

Authors: J. David Spiceland

1st Edition

1308168926, 978-1308168920