Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Need working out to understand Question 6 (this question has three parts (a), (b) & (c)) (a) There are three securities (A, B and C)

Need working out to understand

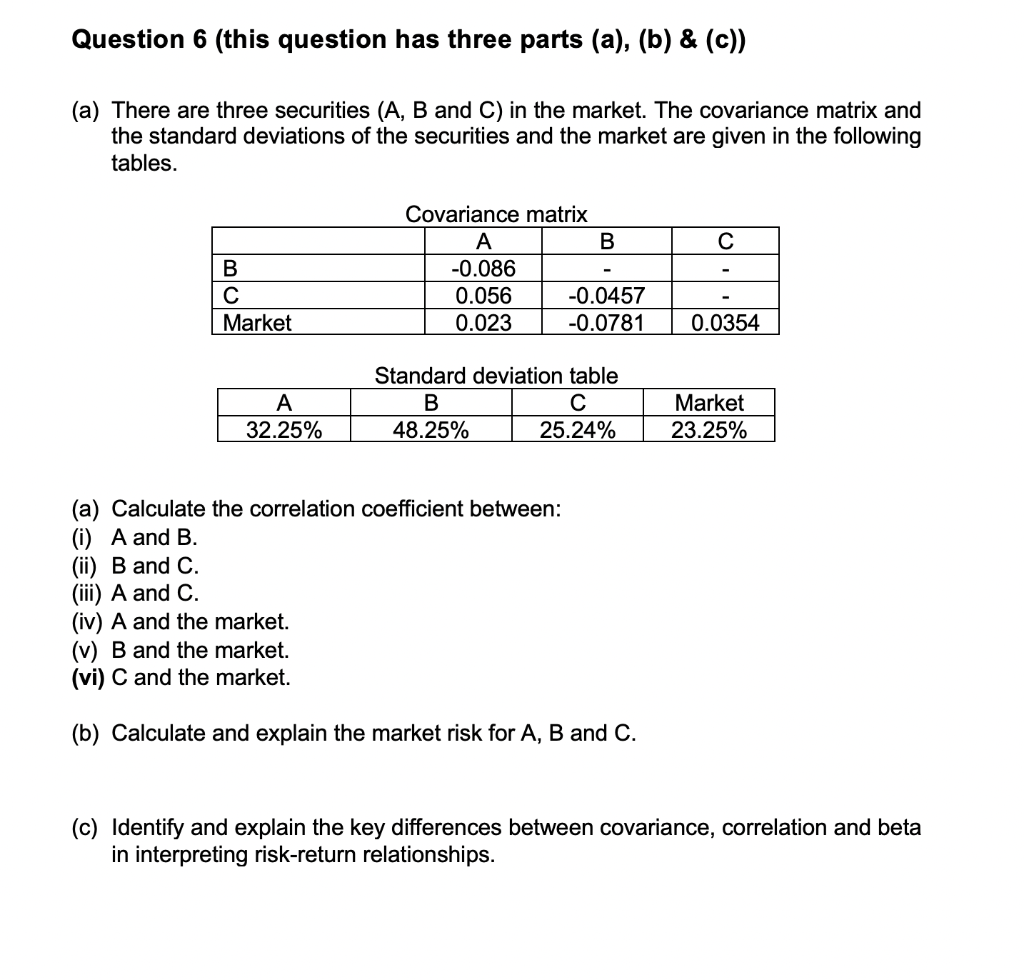

Question 6 (this question has three parts (a), (b) & (c)) (a) There are three securities (A, B and C) in the market. The covariance matrix and the standard deviations of the securities and the market are given in the following tables. B C Market Covariance matrix A B -0.086 0.056 -0.0457 0.023 -0.0781 0.0354 A 32.25% Standard deviation table B 48.25% 25.24% Market 23.25% (a) Calculate the correlation coefficient between: (i) A and B. (ii) B and C. (iii) A and C. (iv) A and the market. (v) B and the market. (vi) C and the market. (b) Calculate and explain the market risk for A, B and C. (c) Identify and explain the key differences between covariance, correlation and beta in interpreting risk-return relationships

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Introduction To Financial Markets A Quantitative Approach

Authors: Paolo Brandimarte

1st Edition

1118014774, 9781118014776