Answered step by step

Verified Expert Solution

Question

1 Approved Answer

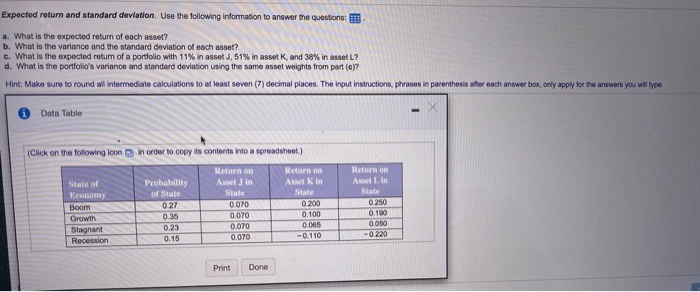

needed helping solving and explanation for all parts Expected return and standard deviation. Use the following information to answer the questions: a. What is the

needed helping solving and explanation for all parts

Expected return and standard deviation. Use the following information to answer the questions: a. What is the expected return of each asset? b. What is the variance and the standard deviation of each asset? c. What is the expected return of a portfolio with 11% in asset J, 51% in asset K, and 38% in asset L? d. What is the portfolio's variance and standard deviation using the same asset weights from part (c)? Hint: Make sure to round all intermediate calculations to at least seven (7) decimal places. The input instructions, phrases in parenthesis after each answer box, only apply for the answers you will type - Data Table (Click on the following icon in order to copy its contents into a spreadshoot) State of Economy Boom Growth Stagnant Recension Probability of State 027 0.35 0.23 0.15 Return on Asset Jin State 0.070 0.070 0.070 0.070 Return on Aset Kin State 0 200 0.100 0.005 -0.110 Return on As Lio Sale 0.250 0.180 0.010 -0.220 Print Done Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management In The Public Sector Tools Applications And Cases

Authors: Xiaohu Wang

1st Edition

0765616785, 9780765616784