Answered step by step

Verified Expert Solution

Question

1 Approved Answer

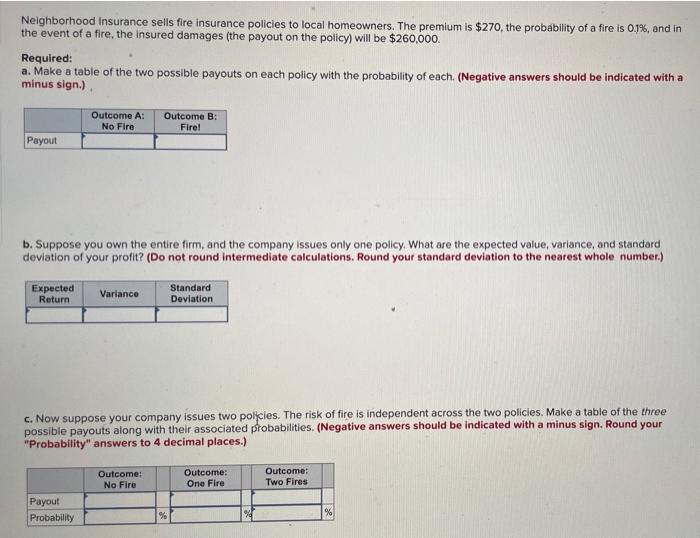

Neighborhood Insurance sells fire insurance policies to local homeowners. The premium is $270, the probability of a fire is 0.1%, and in the event of

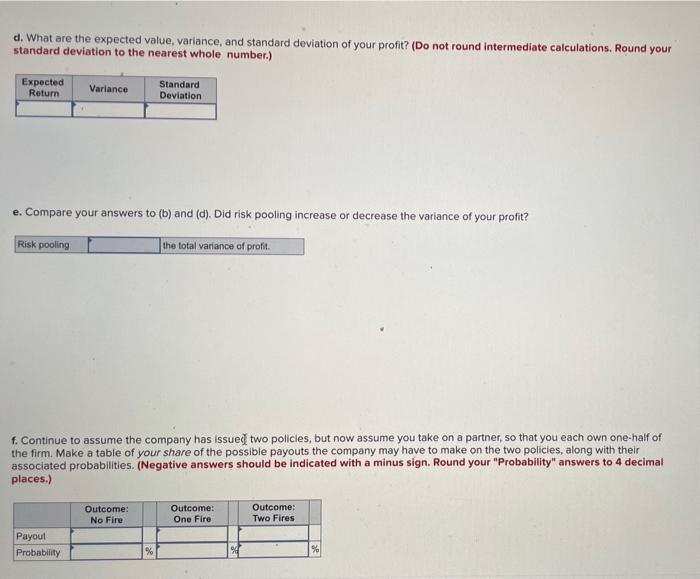

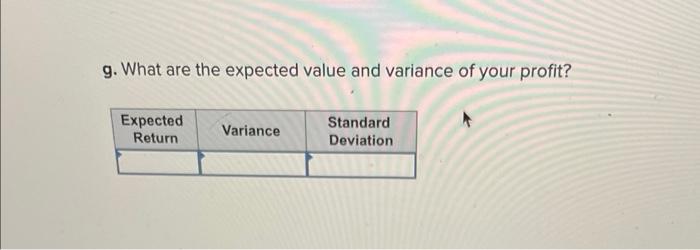

Neighborhood Insurance sells fire insurance policies to local homeowners. The premium is $270, the probability of a fire is 0.1%, and in the event of a fire, the insured damages (the payout on the policy) will be $260,000. Required: a. Make a table of the two possible payouts on each policy with the probability of each. (Negative answers should be indicated with a minus sign.) b. Suppose you own the entire firm, and the company issues only one policy. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) c. Now suppose your company issues two poljcies. The risk of fire is independent across the two policies. Make a table of the three possible payouts along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) d. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) e. Compare your answers to (b) and (d). Did risk pooling increase or decrease the variance of your profit? f. Continue to assume the company has issued two policies, but now assume you take on a partner, so that you each own one-half of the firm. Make a table of your share of the possible payouts the company may have to make on the two policies, along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) g. What are the expected value and variance of your profit? Neighborhood Insurance sells fire insurance policies to local homeowners. The premium is $270, the probability of a fire is 0.1%, and in the event of a fire, the insured damages (the payout on the policy) will be $260,000. Required: a. Make a table of the two possible payouts on each policy with the probability of each. (Negative answers should be indicated with a minus sign.) b. Suppose you own the entire firm, and the company issues only one policy. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) c. Now suppose your company issues two poljcies. The risk of fire is independent across the two policies. Make a table of the three possible payouts along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) d. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) e. Compare your answers to (b) and (d). Did risk pooling increase or decrease the variance of your profit? f. Continue to assume the company has issued two policies, but now assume you take on a partner, so that you each own one-half of the firm. Make a table of your share of the possible payouts the company may have to make on the two policies, along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) g. What are the expected value and variance of your profit

Neighborhood Insurance sells fire insurance policies to local homeowners. The premium is $270, the probability of a fire is 0.1%, and in the event of a fire, the insured damages (the payout on the policy) will be $260,000. Required: a. Make a table of the two possible payouts on each policy with the probability of each. (Negative answers should be indicated with a minus sign.) b. Suppose you own the entire firm, and the company issues only one policy. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) c. Now suppose your company issues two poljcies. The risk of fire is independent across the two policies. Make a table of the three possible payouts along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) d. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) e. Compare your answers to (b) and (d). Did risk pooling increase or decrease the variance of your profit? f. Continue to assume the company has issued two policies, but now assume you take on a partner, so that you each own one-half of the firm. Make a table of your share of the possible payouts the company may have to make on the two policies, along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) g. What are the expected value and variance of your profit? Neighborhood Insurance sells fire insurance policies to local homeowners. The premium is $270, the probability of a fire is 0.1%, and in the event of a fire, the insured damages (the payout on the policy) will be $260,000. Required: a. Make a table of the two possible payouts on each policy with the probability of each. (Negative answers should be indicated with a minus sign.) b. Suppose you own the entire firm, and the company issues only one policy. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) c. Now suppose your company issues two poljcies. The risk of fire is independent across the two policies. Make a table of the three possible payouts along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) d. What are the expected value, variance, and standard deviation of your profit? (Do not round intermediate calculations. Round your standard deviation to the nearest whole number.) e. Compare your answers to (b) and (d). Did risk pooling increase or decrease the variance of your profit? f. Continue to assume the company has issued two policies, but now assume you take on a partner, so that you each own one-half of the firm. Make a table of your share of the possible payouts the company may have to make on the two policies, along with their associated probabilities. (Negative answers should be indicated with a minus sign. Round your "Probability" answers to 4 decimal places.) g. What are the expected value and variance of your profit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Portfolio Performance Measurement And Benchmarking

Authors: Jon Christopherson, David Carino, Wayne Ferson

1st Edition