Answered step by step

Verified Expert Solution

Question

1 Approved Answer

NG MODEL & THE GREEKS Consider a European option on a non-dividend paying stock where the current stock price is $30, the strike price is

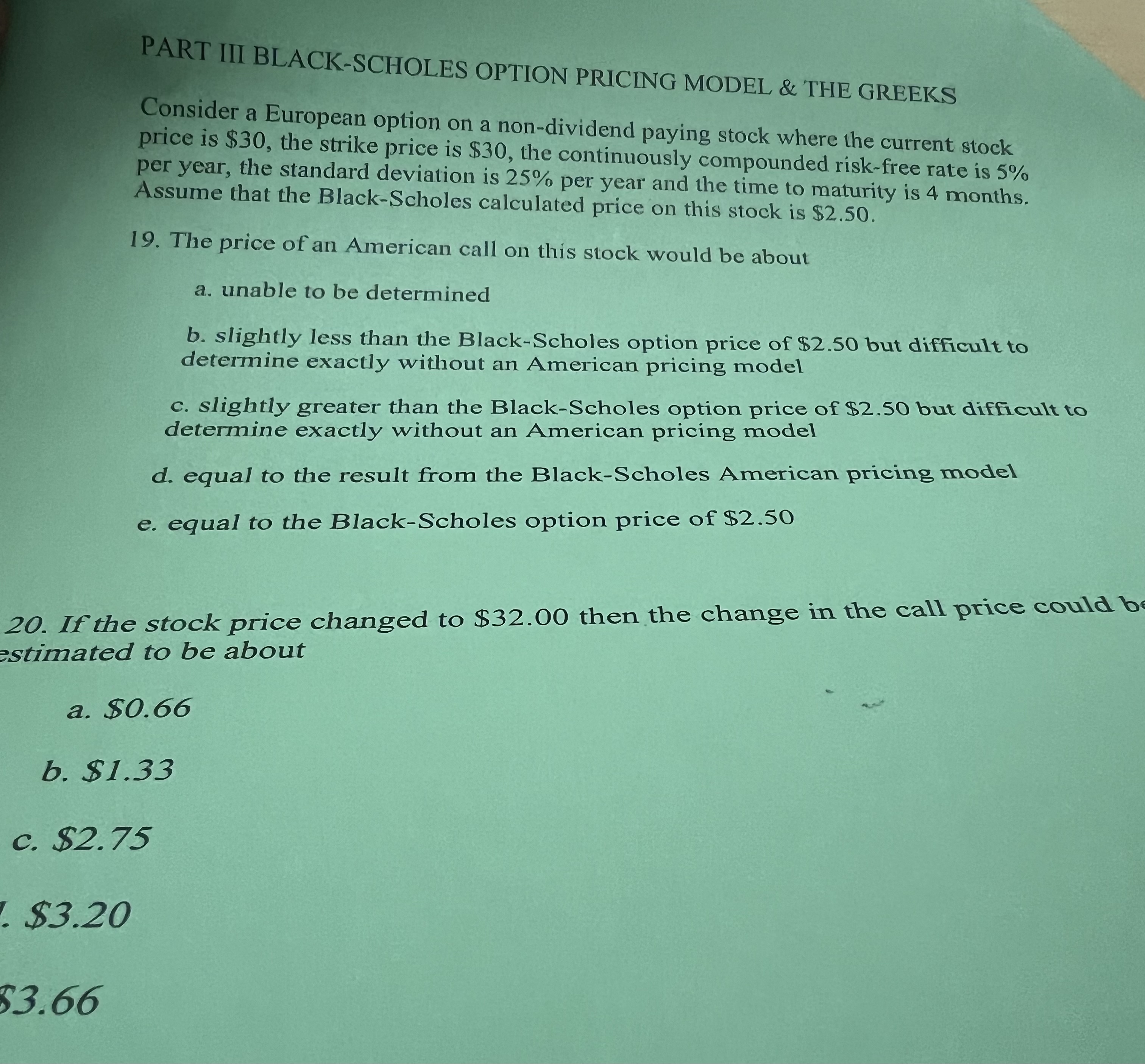

NG MODEL \& THE GREEKS Consider a European option on a non-dividend paying stock where the current stock price is $30, the strike price is $30, the continuously compounded risk-free rate is 5% per year, the standard deviation is 25% per year and the time to maturity is 4 months. Assume that the Black-Scholes calculated price on this stock is $2.50. 19. The price of an American call on this stock would be about a. unable to be determined b. slightly less than the Black-Scholes option price of $2.50 but difficult to determine exactly without an American pricing model c. slightly greater than the Black-Scholes option price of $2.50 but difficult to determine exactly without an American pricing model d. equal to the result from the Black-Scholes American pricing model e. equal to the Black-Scholes option price of $2.50 20. If the stock price changed to $32.00 then the change in the call price could b stimated to be about a. $0.66 b. $1.33 c. $2.75 $3.20 33.66

NG MODEL \& THE GREEKS Consider a European option on a non-dividend paying stock where the current stock price is $30, the strike price is $30, the continuously compounded risk-free rate is 5% per year, the standard deviation is 25% per year and the time to maturity is 4 months. Assume that the Black-Scholes calculated price on this stock is $2.50. 19. The price of an American call on this stock would be about a. unable to be determined b. slightly less than the Black-Scholes option price of $2.50 but difficult to determine exactly without an American pricing model c. slightly greater than the Black-Scholes option price of $2.50 but difficult to determine exactly without an American pricing model d. equal to the result from the Black-Scholes American pricing model e. equal to the Black-Scholes option price of $2.50 20. If the stock price changed to $32.00 then the change in the call price could b stimated to be about a. $0.66 b. $1.33 c. $2.75 $3.20 33.66 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Secured Finance Transactions Key Assets And Emergin Markets

Authors: Paul U Ali

1st Edition

1905783108, 978-1905783106