Answered step by step

Verified Expert Solution

Question

1 Approved Answer

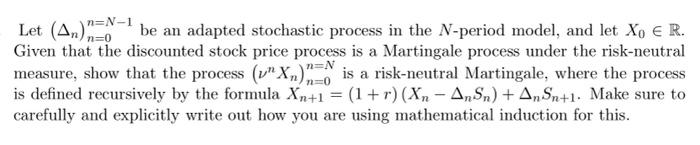

n=N-1 Let ( An),1=0 be an adapted stochastic process in the N-period model, and let Xo E R. Given that the discounted stock price process

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Engineering Mathematics

Authors: Dennis G Zill, Warren S Wright

5th Edition

1449679781, 9781449679781