Answered step by step

Verified Expert Solution

Question

1 Approved Answer

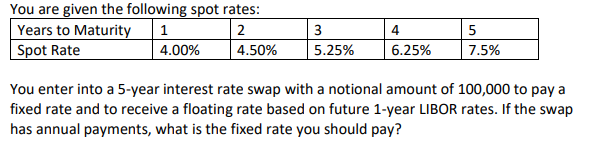

NO EXCEL SOLUTION THANKS You are given the following spot rates: Years to Maturity 1 Spot Rate 4.00% 4.50% 5 5.25% 6.25% 7.5% You enter

NO EXCEL SOLUTION THANKS

You are given the following spot rates: Years to Maturity 1 Spot Rate 4.00% 4.50% 5 5.25% 6.25% 7.5% You enter into a 5-year interest rate swap with a notional amount of 100,000 to pay a fixed rate and to receive a floating rate based on future 1-year LIBOR rates. If the swap has annual payments, what is the fixed rate you should payStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Empire In Pawn Being Lectures And Essays On Indian Colonial And Domestic Finance Preference Free Trade Etc

Authors: A. J. (Alexander Johnstone) Wilson

1st Edition

1290631565, 9781290631563