Answered step by step

Verified Expert Solution

Question

1 Approved Answer

No need to explain. Please answer all the questions correctly. Thank you in advance. eBook Problem 4-6 Calculation of Gain or Loss and Net Capital

No need to explain. Please answer all the questions correctly. Thank you in advance.

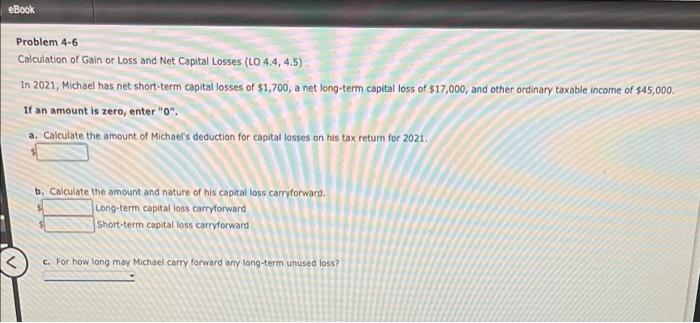

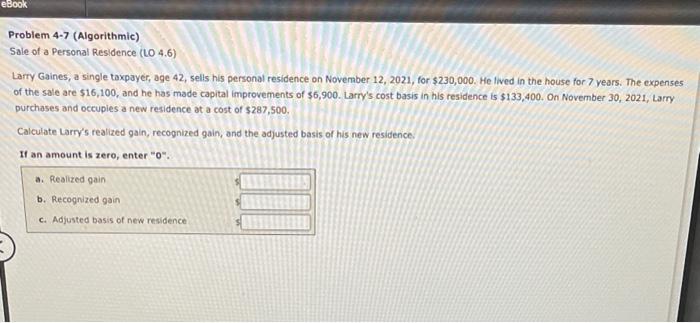

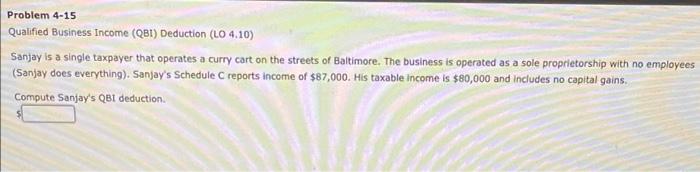

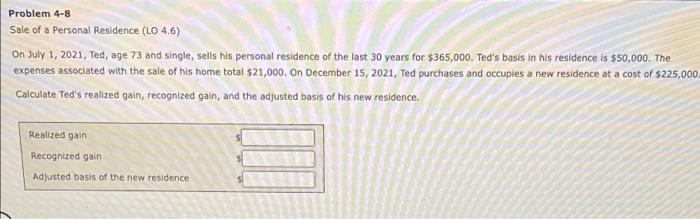

eBook Problem 4-6 Calculation of Gain or Loss and Net Capital Losses (LO 4.4, 4.5) In 2021, Michael has net short-term capital losses of $1,700, a net long-term capital loss of $17,000, and other ordinary taxable income of $45,000 If an amount is zero, enter "0". a. Calculate the amount of Michael's deduction for capital losses on his tax return for 2021. b. Calculate the amount and nature of his capital loss carryforward Long-term capital loss carryforward Short-term capital loss carryforward c. For how long may Michael carry forward any long-term unused loss? eBook Problem 4-7 (Algorithmic) Sale of a Personal Residence (LO 4.6) Larry Gaines, a single taxpayer, age 42, sells his personal residence on November 12, 2021, for $230,000. He lived in the house for 7 years. The expenses of the sale are $16,100, and he has made capital improvements of $6,900. Larry's cost basis in his residence is $133,400. On November 30, 2021, Larry purchases and occuples a new residence at a cost of $287,500, Calculate Larry's realized gain, recognized gain, and the adjusted basis of his new residence If an amount is zero, enter "o". a. Realized gain b. Recognized gain c. Adjusted basis of new residence Problem 4-15 Qualified Business Income (QB1) Deduction (LO 4.10) Sanjay is a single taxpayer that operates a curry cart on the streets of Baltimore. The business is operated as a sole proprietorship with no employees (Sanjay does everything). Sanjay's Schedule C reports income of $87,000. His taxable income is $80,000 and includes no capital gains. Compute Sanjay's Qet deduction a Problem 4-8 Sale of a personal Residence (LO 4.6) On July 1, 2021, Ted, age 73 and single, sells his personal residence of the last 30 years for $365,000. Ted's basis in his residence is $50,000. The expenses associated with the sale of his home total $21,000, On December 15, 2021, Ted purchases and occupies a new residence at a cost of $225,000 Calculate Ted's realized gain, recognized gain, and the adjusted basis of his new residence. Realized gain Recognized gain Adjusted basis of the new residence Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quality Auditing Note Book Journal Notes Checklist Questions Observations Evidence Log

Authors: Just Visualize It, The Quality Guy

1st Edition

1726688402, 978-1726688406