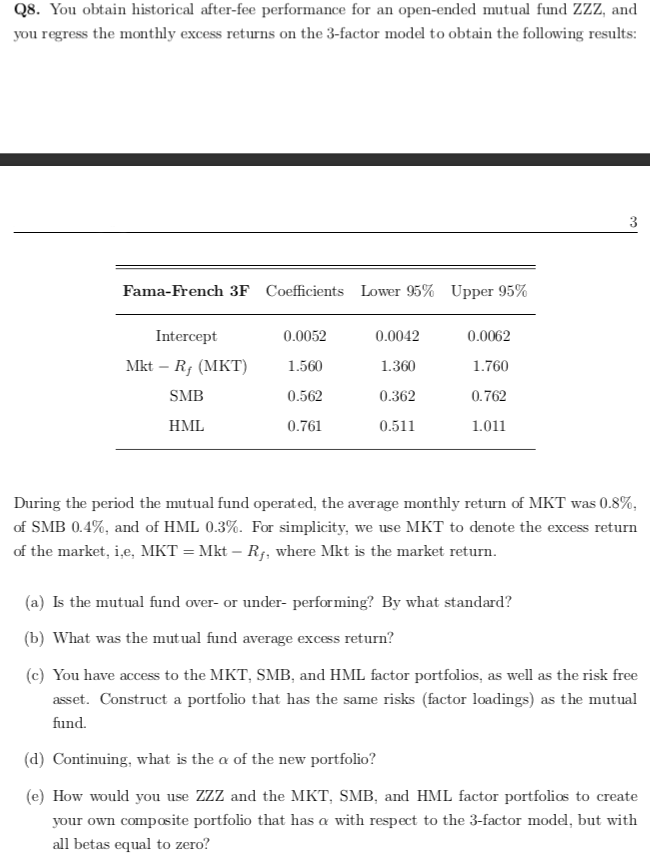

Question

No one answered my question in the past 24 hours. :( Please, if you could help, that would be much appreciated. I just need help

No one answered my question in the past 24 hours. :( Please, if you could help, that would be much appreciated. I just need help with part a in this question. I have posted the rest of the parts in other questions, too. Thank you in advance for your help, and I promise to give you a thumbs up for your time!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Unretirement How Baby Boomers Are Changing The Way We Think About Work Community And The Good Life

Authors: Chris Farrell

1st Edition

1632863235,1620401584