Answered step by step

Verified Expert Solution

Question

1 Approved Answer

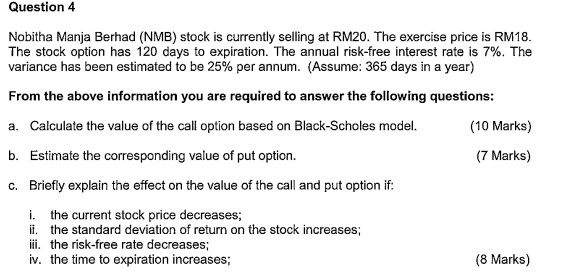

Nobitha Manja Berhad (NMB) stock is currently selling at RM20. The exercise price is RM18. The stock option has 120 days to expiration. The annual

Nobitha Manja Berhad (NMB) stock is currently selling at RM20. The exercise price is RM18. The stock option has 120 days to expiration. The annual risk-free interest rate is 7%. The variance has been estimated to be 25% per annum. (Assume: 365 days in a year) a. Calculate the value of the call option based on Black-Scholes model. b. Estimate the corresponding value of put option. c. Briefly explain the effect on the value of the call and put option if: i. the current stock price decreases: ii. the standard deviation of return on the stock increases: iii. the risk-free rate decreases: iv. the time to expiration increases; Nobitha Manja Berhad (NMB) stock is currently selling at RM20. The exercise price is RM18. The stock option has 120 days to expiration. The annual risk-free interest rate is 7%. The variance has been estimated to be 25% per annum. (Assume: 365 days in a year) a. Calculate the value of the call option based on Black-Scholes model. b. Estimate the corresponding value of put option. c. Briefly explain the effect on the value of the call and put option if: i. the current stock price decreases: ii. the standard deviation of return on the stock increases: iii. the risk-free rate decreases: iv. the time to expiration increases

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Principals Guide To School Budgeting

Authors: Richard D. Sorenson, Lloyd M. Goldsmith

3rd Edition

1506389457, 978-1506389455