Answered step by step

Verified Expert Solution

Question

1 Approved Answer

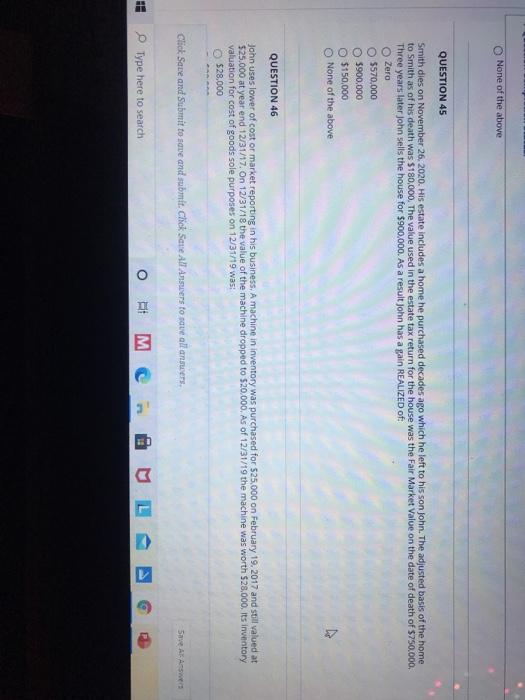

None of the above QUESTION 45 Smith dies on November 26, 2020. His estate includes a home he purchased decades ago which he left to

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Auditors Guide Of 1869 A Review And Computer Enhancement Of Recently Discovered Old Microfilm Of Americas First Book On Auditing By H J Mettenheimer

Authors: Peter L. McMickle, Paul H. Jensen

1st Edition

0367534622, 978-0367534622