Answered step by step

Verified Expert Solution

Question

1 Approved Answer

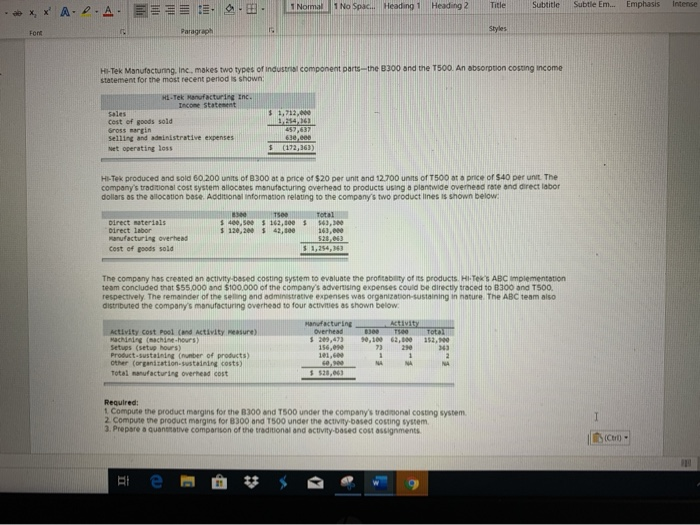

Normal 1 No Spac... Heading 1 Heading 2 Title Subtitle Subtle Em... Emphasis intense - XX A..A. EEEE. - - Hi-Tek Manufacturing, Inc. makes two

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Benefit Analysis With Reference To Environment And Ecology

Authors: James H. Meisel, K. Puttaswamaiah

1st Edition

1138521329, 978-1138521322