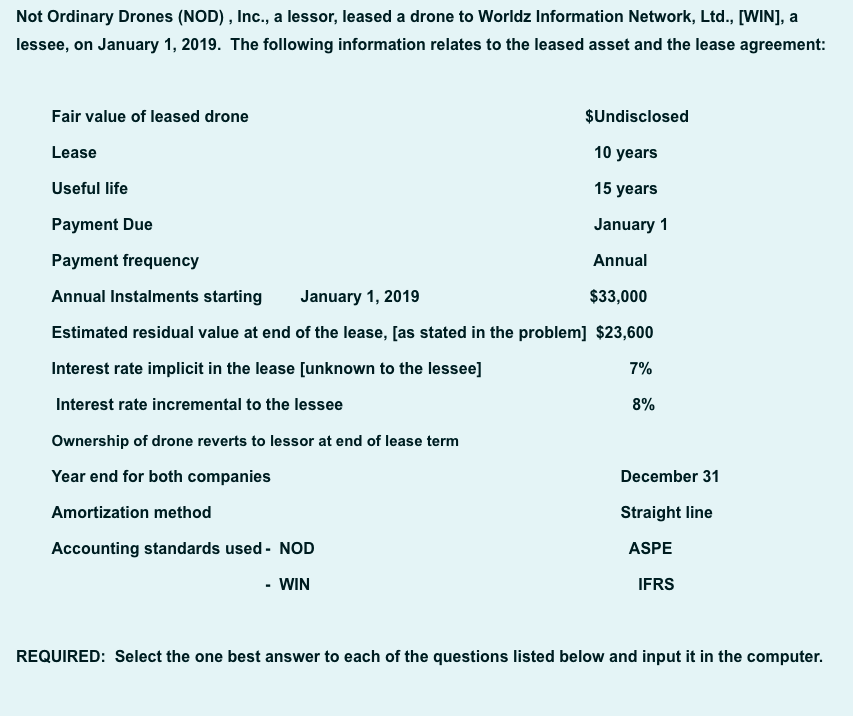

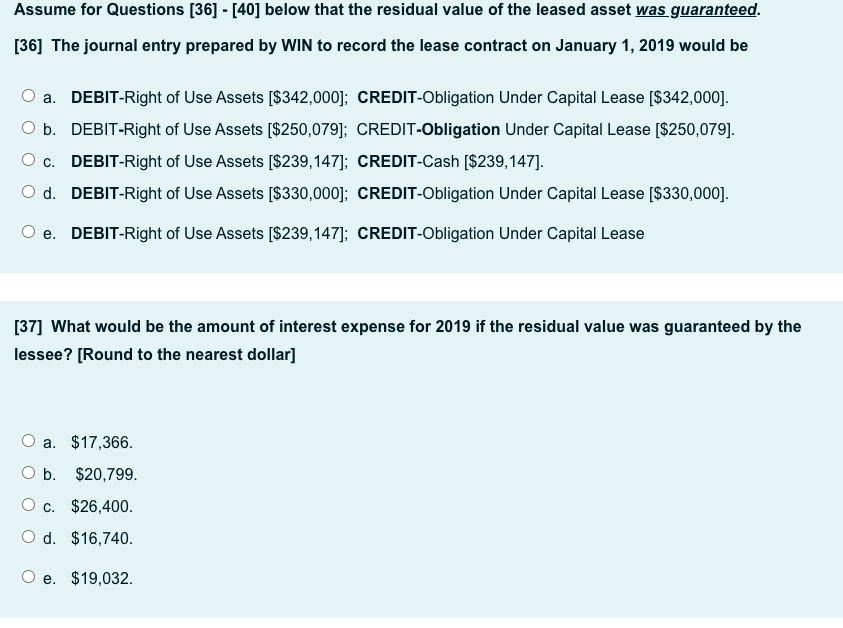

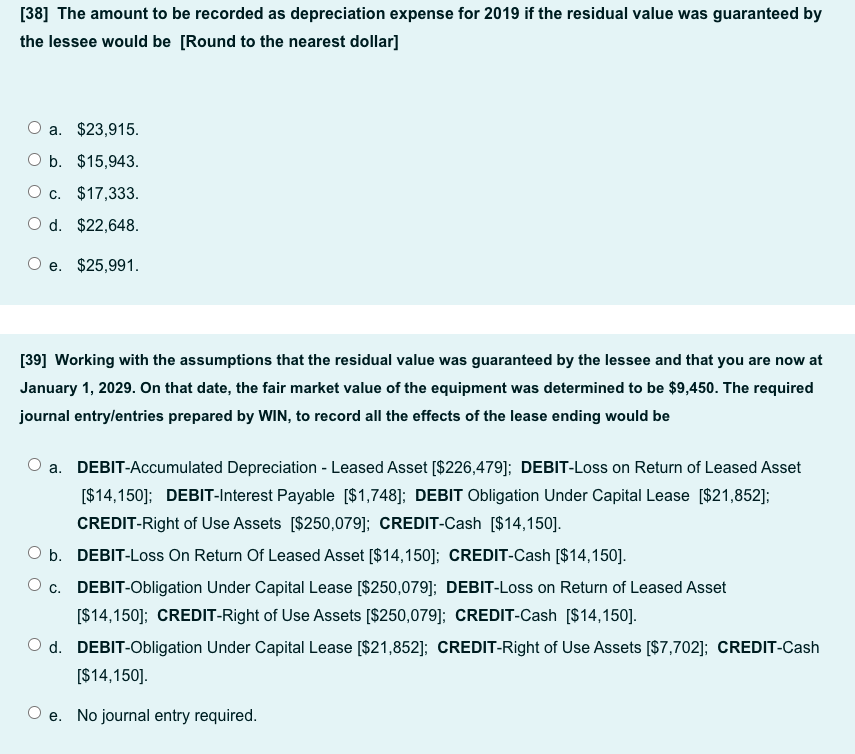

Not Ordinary Drones (NOD), Inc., a lessor, leased a drone to Worldz Information Network, Ltd., [WIN], a lessee, on January 1, 2019. The following information relates to the leased asset and the lease agreement: Fair value of leased drone Lease $Undisclosed 10 years 15 years Useful life Payment Due January 1 Payment frequency Annual Annual Instalments starting January 1, 2019 $33,000 Estimated residual value at end of the lease, [as stated in the problem] $23,600 Interest rate implicit in the lease [unknown to the lessee) 7% Interest rate incremental to the lessee 8% Ownership of drone reverts to lessor at end of lease term Year end for both companies Amortization method Accounting standards used - NOD - WIN December 31 Straight line ASPE IFRS REQUIRED: Select the one best answer to each of the questions listed below and input it in the computer. Assume for Questions [36] - [40] below that the residual value of the leased asset was guaranteed. [36] The journal entry prepared by WIN to record the lease contract on January 1, 2019 would be a. DEBIT-Right of Use Assets [$342,000); CREDIT-Obligation Under Capital Lease ($342,000). O b. DEBIT-Right of Use Assets [$250,079); CREDIT-Obligation Under Capital Lease [$250,079). O c. DEBIT-Right of Use Assets [$239, 147]; CREDIT-Cash [$239, 147]. O d. DEBIT-Right of Use Assets [$330,000); CREDIT-Obligation Under Capital Lease ($330,000). e. DEBIT-Right of Use Assets [$239,147]; CREDIT-Obligation Under Capital Lease [37] What would be the amount of interest expense for 2019 if the residual value was guaranteed by the lessee? [Round to the nearest dollar] a. $17,366. b. $20,799. c. $26,400. d. $16,740. e. $19,032. [38] The amount to be recorded as depreciation expense for 2019 if the residual value was guaranteed by the lessee would be [Round to the nearest dollar] a. $23,915. O b. $15,943. O c. $17,333. O d. $22,648. e. $25,991. [39] Working with the assumptions that the residual value was guaranteed by the lessee and that you are now at January 1, 2029. On that date, the fair market value of the equipment was determined to be $9,450. The required journal entrylentries prepared by WIN, to record all the effects of the lease ending would be a. DEBIT-Accumulated Depreciation - Leased Asset ($226,479); DEBIT-Loss on Return of Leased Asset [$14,150); DEBIT-Interest Payable ($1,748]; DEBIT Obligation Under Capital Lease [$21,852]; CREDIT-Right of Use Assets [$250,079]; CREDIT-Cash [$14,150]. b. DEBIT-Loss On Return Of Leased Asset ($14,150); CREDIT-Cash [$14,150]. OC. DEBIT-Obligation Under Capital Lease [$250,079]; DEBIT-Loss on Return of Leased Asset [$14,150]; CREDIT-Right of Use Assets [$250,079); CREDIT-Cash [$14,150]. O d. DEBIT-Obligation Under Capital Lease [$21,852); CREDIT-Right of Use Assets [$7,702); CREDIT-Cash [$14,150]. e. No journal entry required. [40] Now assume for this Question that the lease agreement contained a bargain purchase option of $18,000 at the end of the lease term instead of a residual value of $23,600. Further assume that WIN recorded the leased asset at $285,488 on January 1, 2019. What would be the amount for depreciation expense which WIN would record in 2019? [Round to the nearest dollar). a. $26,749. O b. $28,738. O c. $17,833. O d. $19,033 Oe. None of the above. Assume for Questions [41] - [46] below that the residual value of the leased asset was not guaranteed. [41] How should WIN classify the lease? a. A capital lease because the lease term is less than the useful life of the asset. O b. A capital lease because the contract terms meet one of the criteria specified by ASPE. OC. An operating lease because the ownership rights are not acquired by the lessee. O d. An operating lease because NOD is not applying IFRS 16. e. A capital lease because the lease term does not meet the short lease term or low value exemptions provided for under IFRS-16. [42] The journal entry prepared by WIN to record the lease contract on January 1, 2019 would be O a. DEBIT-Right of Use Assets [$260,000); CREDIT-Obligation Under Capital Lease [$260,000). O b. DEBIT-Right of Use Assets [$250,090]; CREDIT-Obligation Under Capital Lease [$250,090]. OC. DEBIT-Right of Use Assets [$250,090]; CREDIT-Cash [$250,090). O d. DEBIT-Right of Use Assets [$239,147]; CREDIT-Obligation Under Capital Lease [$239,147]. Oe. DEBIT-Right of Use Assets [$330,000); CREDIT-Obligation Under Capital Lease [$330,000). [43] The journal entry prepared by WIN to record any other transaction related to the lease contract on January 1, 2019. a. DEBIT-Cash [$33,000); CREDIT-Obligation Under Capital Lease [$33,000). O b. DEBIT-Obligation Under Capital Lease [$33,000); CREDIT-Cash [$33,000). OC. DEBIT-Executory Costs-Capital Lease ($33,000); CREDIT-Cash ($33,000). Od. DEBIT-Interest Expense ($33,000); CREDIT-Cash [$33,000). e. No journal entry required as there was no other transaction on January 1, 2019. [44] Assume for this Question only that at the time of entering into this lease contract, NOD was aware that WIN was operating under severe financial difficulties and thus determined that the credit risk associated with this lease was not normal when compared with the risk of collection of other similar receivables. How should NOD classify this lease? a. Classify as a finance type lease. O b. Classify as a capital, manufacturer/dealer type lease. O c. Classify as a direct sales capital lease. O d. Classify as an operating lease. Oe. None of the above. [45] Regardless of your answer in [44] above, assume that NOD classifies the lease as a capital lease. Determine the fair value of the drone leased. O a. $330,000 O b. $353,600. O c. $495,000. O d. $518,600. Oe. None of the above. [46] Regardless of your answer in [44] above, assume that NOD classifies the lease as a capital lease. The company operates at a 20% gross profitability rate and sells the drones in the market at a price of $260,000 each. Further assume that the estimated residual value amounting to $23,600 was not guaranteed. Under these assumptions, the journal entry prepared by NOD to record the lease contract on January 1, 2019 would be a. DEBIT-Lease Receivable [$353,600); DEBIT-Cost of Goods Sold ($196,003]; CREDIT-Sales Revenue [$248,003); CREDIT-Inventory [$208,000); CREDIT-Unearned Interest Revenue [$93,600]. O b. DEBIT-Lease Receivable [$330,000); DEBIT-Cost of Goods Sold ($208,000); CREDIT-Sales Revenue [$260,000); CREDIT-Inventory [$208,000); CREDIT-Unearned Interest Revenue [$70,000). OC. DEBIT-Lease Receivable [$260,000); DEBIT-Cost of Goods Sold ($208,000); CREDIT-Sales Revenue ($260,000); CREDIT-Inventory [$208,000). d. DEBIT-Lease Receivable [$353,500); DEBIT-Cost of Goods Sold ($208,000); CREDIT-Sales Revenue ($260,000); CREDIT-Inventory [$208,000); CREDIT-Unearned Interest Revenue [$93,600]. e. None of the above