Question

NOTE: I'm sorry to whoever asked for more information. This is the whole this, there is no more information than this. Please do try to

NOTE: I'm sorry to whoever asked for more information. This is the whole this, there is no more information than this. Please do try to help though. You are to prepare an algorithmic impact assessment for the TechnoTec business proposal outlined in the Appendices. This will include: a) An explanation of how technology can help decision making (informed by the scholarly literature and real-world examples) explaining positive and negative aspects of the ethical challenges this can create. b) Analysis of the strengths and weaknesses (including unfairness, discrimination and biases) of the technology in the business proposal c) Analysis of the business, ethical and cybersecurity risks TechnoTec faces if it were to implement the business proposal in its current form d) Recommend a security program (including team building and development) for the business proposal e) Recommendations on how to alter/improve the algorithm so that it can mitigate the risks and better achieve the goals of the business proposal

Appendix 1: NoFlake Business Case: TechnoTec has decided to develop an innovative financial product for consumers, NoFlake. The management has understood that borrowers who are at greater risk of having money stolen from them by hackers (or other forms of cyberattacks) are less likely to be able to re-pay their debts and are more likely to be a vector for infiltration of TechnoTecs IT systems. Therefore, to create a competitive advantage over the industry leaders, NoFlake will use an artificial intelligence engine to analyse both the credit risk and the cyber-security maturity of their borrowers How Does NoFlake Work? The AI engine uses an algorithm (see Appendix 2) to generate a predictive risk score between -100 and +100 for each potential borrower (with positive 100 being awarded to thelowest-risk borrowers and negative 100 being awarded to the highest-risk borrowers). The development team hired Swizzle Pty Ltd to collect training data for the algorithm. Swizzle uses individual backpackers (paid minimum wage) to conduct surveys on major public streets in capital cities. Financial Analysis of NoFlake: TechnoTec currently pays 20 employees an average of $76,000 per year to determine which loan applicants should be approved, of which only two employees would be needed after NoFlake is introduced. NoFlake has two main goals: 1) to outperform human credit risk analysts by at least 20% (i.e. that the rate of loan non-repayments by applicants selected by NoFlake will be below 5.6% vs the current non-repayment rate of 7%); and 2) to lower by at least 40% (i.e. $600,000) the annual losses incurred by TechnoTec as a result of cyber-attackers gaining access to its internal systems using the legitimate log-in details of its customers. In 2020, TechnoTec lost $1.5m from such cyberattacks.

On a loan-book totalling $50 million, the expected annual savings from NoFlake are: $50,000,000 * 0.014 (credit benefits) + $600,000 (cyber-security benefits) + $76,000 * 18 (labour cost savings) = $2,668,000. Given an expected cost of development of $1 200 000 and ongoing operational costs of $300,000, over a five-year period, the expected savings from implementing NoFlake are: $2,668,000 * 5 ($1,200,000 + ( $300,000 *5)) = $10,640,000. This equates to an 887% return on initial development costs, or 177% per annum over five years.

Additional revenues could be generated by licencing the algorithm to third-party financial institutions (such as mortgage brokers) and paying a trailing commission to those brokers based on the value of the loans they originate which are approved by the algorithm. Those brokers would need to be trained in how to gather and fill in the information needed from borrowers to enable the algorithm to make its decisions.

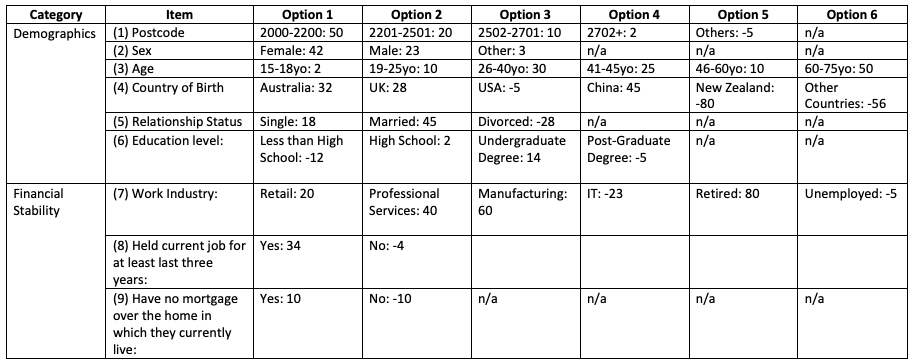

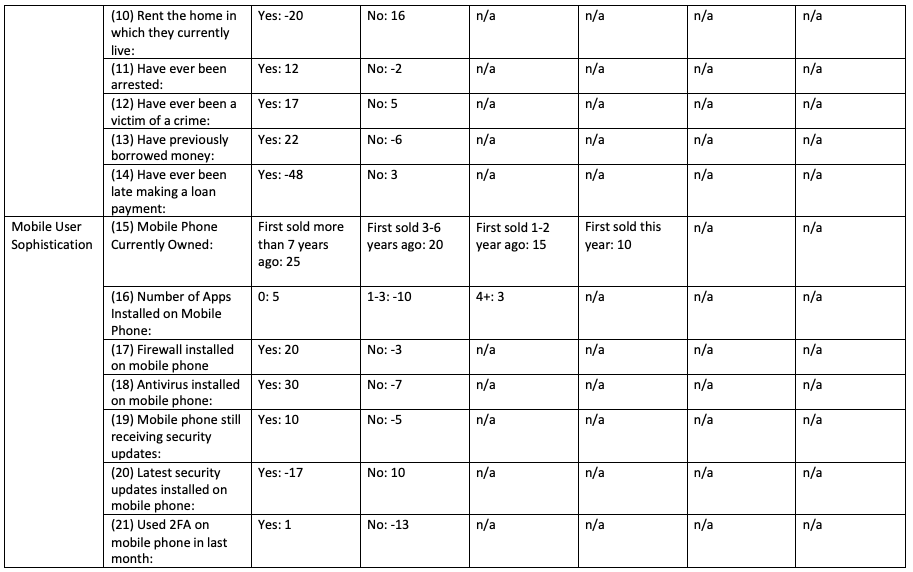

Appendix 2: NoFlake Algorithm: Overall Score = (0.35 * Demographics) + (0.2 * Financial Stability) + (0.1 * Mobile User Sophistication) - (0.3 * Cyber-Security Sophistication) - 0.25 Demographic Score = Item Scores (1) + (2) + (3) + (4) + (5) + (6) Financial Stability Score = Item Scores (7) + (8) + (9) + (10) + (11) + (12) + (13) + (14) Mobile User Sophistication Score = Item Scores (15) + (16) + (17) + (18) + (19) + (20) + (21) + (22) Cyber-Security Sophistication Score = Item Scores (23) + (24) + (25)

Category Demographics Financial Stability Option 1 (1) Postcode 2000-2200: 50 (2) Sex Female: 42 (3) Age 15-18yo: 2 (4) Country of Birth Australia: 32 (5) Relationship Status (6) Education level: Single: 18 Less than High School: -12 (7) Work Industry: Retail: 20 (8) Held current job for Yes: 34 at least last three years: (9) Have no mortgage Yes: 10 over the home in which they currently live: Item Option 2 2201-2501: 20 Male: 23 19-25yo: 10 UK: 28 Married: 45 High School: 2 Professional Services: 40 No: -4 No: -10 Option 3 2502-2701: 10 Other: 3 26-40yo: 30 USA: -5 Divorced: -28 Undergraduate Degree: 14 Manufacturing: 60 n/a Option 4 2702+: 2 n/a 41-45yo: 25 China: 45 n/a Post-Graduate Degree: -5 IT: -23 n/a Option 5 Others: -5 n/a 46-60yo: 10 New Zealand: -80 n/a n/a Retired: 80 n/a Option 6 n/a n/a 60-75yo: 50 Other Countries: -56 n/a n/a Unemployed: -5 n/a Mobile User Sophistication (10) Rent the home in which they currently live: (11) Have ever been arrested: (12) Have ever been a victim of a crime: (13) Have previously borrowed money: (14) Have ever been late making a loan payment: (15) Mobile Phone Currently Owned: (16) Number of Apps Installed on Mobile Phone: (17) Firewall installed on mobile phone (18) Antivirus installed on mobile phone: (19) Mobile phone still receiving security updates: (20) Latest security updates installed on mobile phone: (21) Used 2FA on mobile phone in last month: Yes: -20 Yes: 12 Yes: 17 Yes: 22 Yes: -48 First sold more than 7 years ago: 25 0:5 Yes: 20 Yes: 30 Yes: 10 Yes: -17 Yes: 1 No: 16 No: -2 No: 5 No: -6 No: 3 First sold 3-6 years ago: 20 1-3: -10 No: -3 No: -7 No: -5 No: 10 No: -13 n/a n/a n/a n/a n/a First sold 1-2 year ago: 15 4+: 3 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a First sold this year: 10 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a (22) Use mobile banking: Cyber-Security (23) Cryptocurrency Sophistication: wallet app installed on mobile phone: (24) Ever purchased a cryptocurrency: (25) Self-rated cyber- security knowledge: Yes: 24 Yes: 53 Yes: 36 1-4: 13 No: -5 No: -34 No: -18 5-7: 8 n/a n/a 8-10: -5 n/a n/a n/a n/a n/a n/a Category Demographics Financial Stability Option 1 (1) Postcode 2000-2200: 50 (2) Sex Female: 42 (3) Age 15-18yo: 2 (4) Country of Birth Australia: 32 (5) Relationship Status (6) Education level: Single: 18 Less than High School: -12 (7) Work Industry: Retail: 20 (8) Held current job for Yes: 34 at least last three years: (9) Have no mortgage Yes: 10 over the home in which they currently live: Item Option 2 2201-2501: 20 Male: 23 19-25yo: 10 UK: 28 Married: 45 High School: 2 Professional Services: 40 No: -4 No: -10 Option 3 2502-2701: 10 Other: 3 26-40yo: 30 USA: -5 Divorced: -28 Undergraduate Degree: 14 Manufacturing: 60 n/a Option 4 2702+: 2 n/a 41-45yo: 25 China: 45 n/a Post-Graduate Degree: -5 IT: -23 n/a Option 5 Others: -5 n/a 46-60yo: 10 New Zealand: -80 n/a n/a Retired: 80 n/a Option 6 n/a n/a 60-75yo: 50 Other Countries: -56 n/a n/a Unemployed: -5 n/a Mobile User Sophistication (10) Rent the home in which they currently live: (11) Have ever been arrested: (12) Have ever been a victim of a crime: (13) Have previously borrowed money: (14) Have ever been late making a loan payment: (15) Mobile Phone Currently Owned: (16) Number of Apps Installed on Mobile Phone: (17) Firewall installed on mobile phone (18) Antivirus installed on mobile phone: (19) Mobile phone still receiving security updates: (20) Latest security updates installed on mobile phone: (21) Used 2FA on mobile phone in last month: Yes: -20 Yes: 12 Yes: 17 Yes: 22 Yes: -48 First sold more than 7 years ago: 25 0:5 Yes: 20 Yes: 30 Yes: 10 Yes: -17 Yes: 1 No: 16 No: -2 No: 5 No: -6 No: 3 First sold 3-6 years ago: 20 1-3: -10 No: -3 No: -7 No: -5 No: 10 No: -13 n/a n/a n/a n/a n/a First sold 1-2 year ago: 15 4+: 3 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a First sold this year: 10 n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a (22) Use mobile banking: Cyber-Security (23) Cryptocurrency Sophistication: wallet app installed on mobile phone: (24) Ever purchased a cryptocurrency: (25) Self-rated cyber- security knowledge: Yes: 24 Yes: 53 Yes: 36 1-4: 13 No: -5 No: -34 No: -18 5-7: 8 n/a n/a 8-10: -5 n/a n/a n/a n/a n/a n/a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Essential Credit Repair Handbook

Authors: Deborah McNaughton

1st Edition

160163160X, 978-1601631602