Answered step by step

Verified Expert Solution

Question

1 Approved Answer

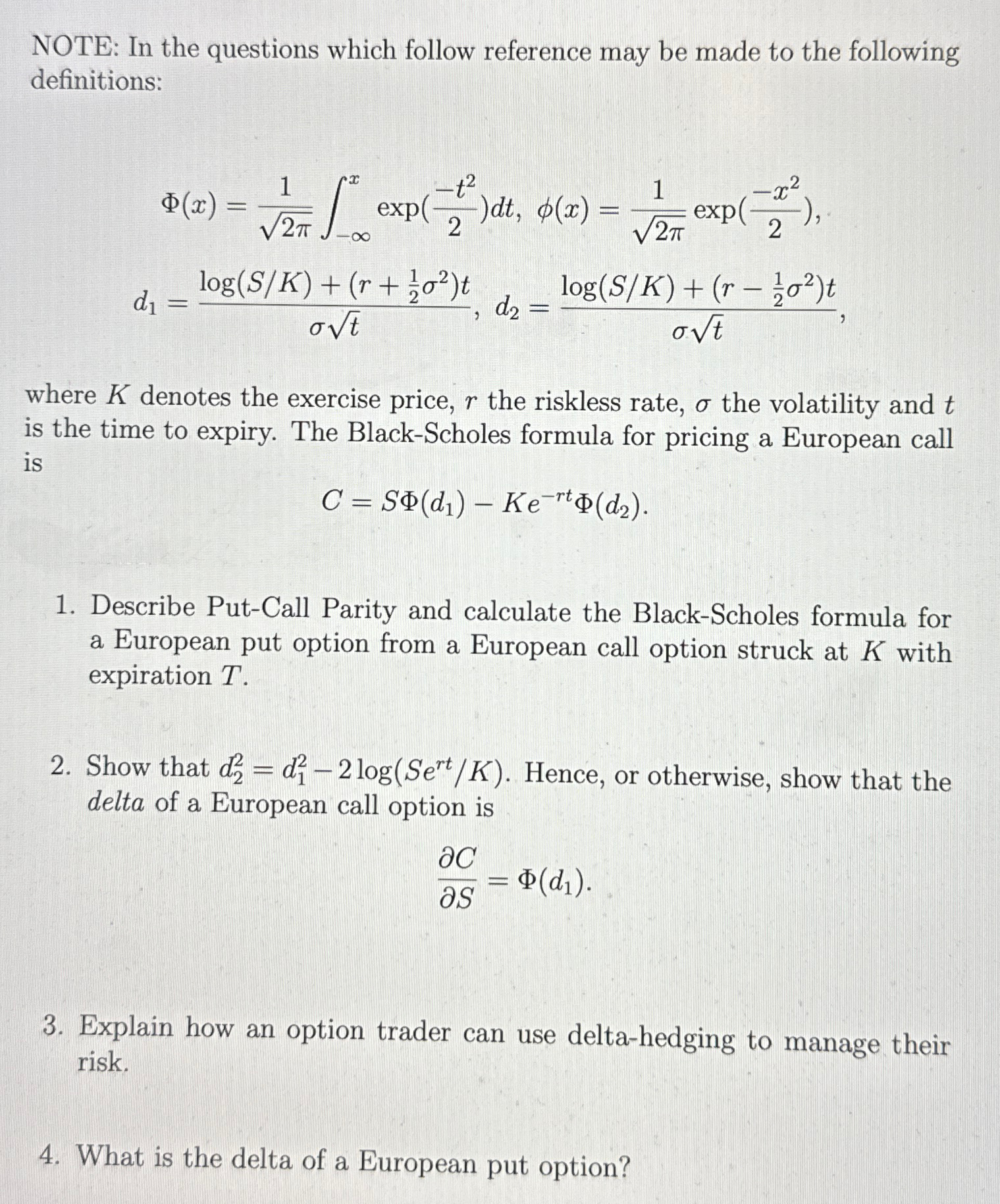

NOTE: In the questions which follow reference may be made to the following definitions: ( x ) = 1 2 2 - x exp (

NOTE: In the questions which follow reference may be made to the following definitions:

expexp

where denotes the exercise price, the riskless rate, the volatility and is the time to expiry. The BlackScholes formula for pricing a European call is

Describe PutCall Parity and calculate the BlackScholes formula for a European put option from a European call option struck at with expiration

Show that Hence, or otherwise, show that the delta of a European call option is

Explain how an option trader can use deltahedging to manage their risk.

What is the delta of a European put option?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Complete Direct Investing Handbook

Authors: Kirby Rosplock

1st Edition

1119094712, 978-1119094715