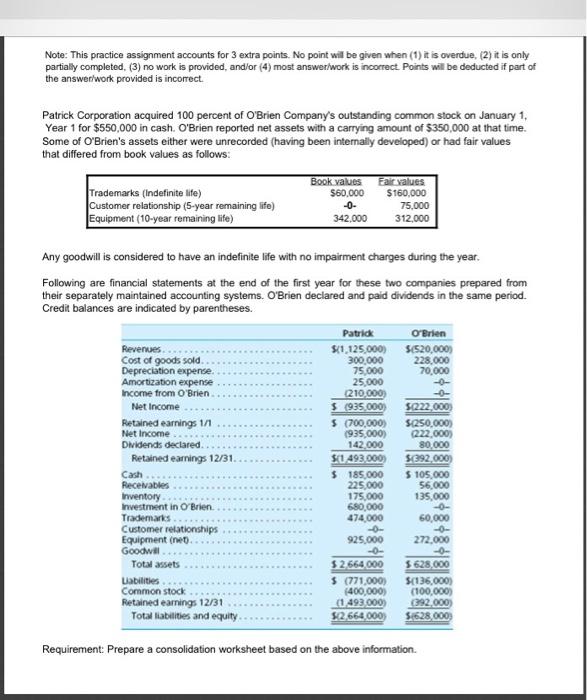

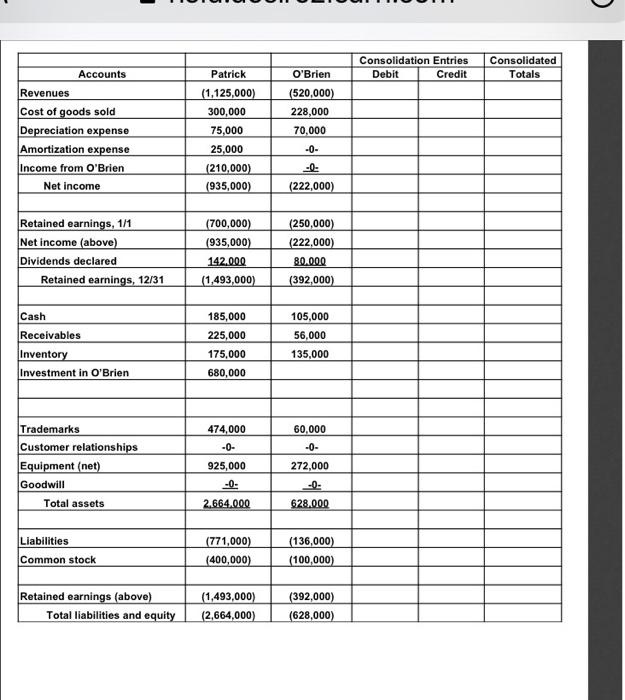

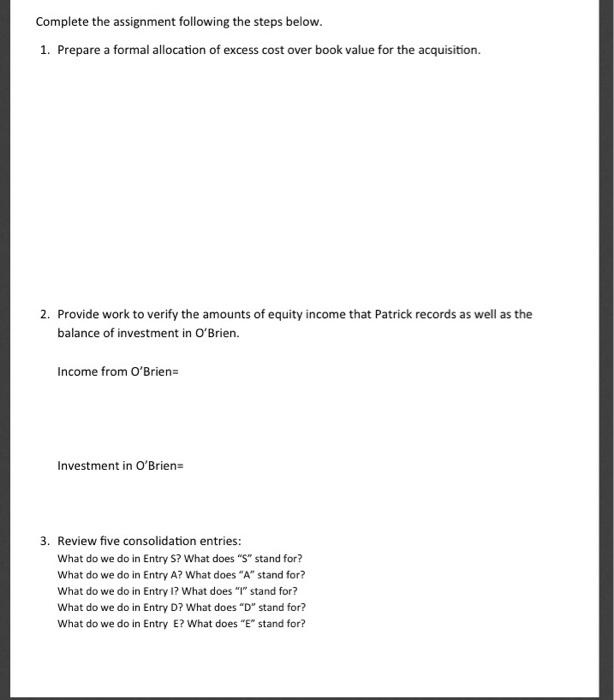

Note: This practice assignment accounts for 3 extra points. No point will be given when (1) it is overdue, (2) it is only partially completed, (3) no work is provided, and/or (4) most answer/work is incorrect Points will be deducted if part of the answer work provided is incorrect. Patrick Corporation acquired 100 percent of O'Brien Company's outstanding common stock on January 1, Year 1 for $550,000 in cash. O'Brien reported net assets with a carrying amount of $350,000 at that time. Some of O'Brien's assets either were unrecorded (having been internally developed) or had fair values that differed from book values as follows: Trademarks (Indefinite life) Customer relationship (5-year remaining life) Equipment (10-year remaining life) Book values $60.000 -0- 342,000 Fair values $160,000 75,000 312,000 Any goodwill is considered to have an indefinite life with no impairment charges during the year. Following are financial statements at the end of the first year for these two companies prepared from their separately maintained accounting systems. O'Brien declared and paid dividends in the same period. Credit balances are indicated by parentheses. Patrick O'Brien Revenues $1.125.000) $520,000) Cost of goods sold 300.000 228.000 Depreciation expense. 75.000 70,000 Amortization expense 25,000 -0- Income from O'Brien 210.000 Net Income $(935.000) 50222,000) Retained earnings 1/1 5 (700,000) $250.000) Net Income 1935,000) 222.000) Dividends declared 142.000 80,000 Retained earnings 12/31 $1493 000) S292.000) Cash $185.000 $ 105.000 Recevables 225.000 56.000 Inventory 175.000 135,000 Investment in O'Brien 680,000 -0- Trademarks 474,000 60,000 Customer relationships Equipment (net 925,000 272.000 Goodwill -0- Total assets 52664.000 5 628.000 Labilities (771,000) $(136,000) Common stock (400,000) (100,000) Retained earnings 12/31 (1493 000) 392.000 Total liabilities and equity $12.668.000 5628,000 Requirement: Prepare a consolidation worksheet based on the above information U Consolidation Entries Debit Credit Consolidated Totals O'Brien Accounts Revenues Cost of goods sold Depreciation expense Amortization expense Income from O'Brien Net income Patrick (1,125,000) 300,000 75,000 25,000 (210,000) (935,000) (520,000) 228,000 70,000 -0- -0- (222,000) Retained earnings, 1/1 Net income (above) Dividends declared Retained earnings, 12/31 (700,000) (935,000) 142.000 (1,493,000) (250,000) (222,000) 80.000 (392,000) Cash Receivables 185,000 225,000 175,000 680,000 105,000 56,000 135,000 Inventory Investment in O'Brien 474,000 -0- 60,000 -0- Trademarks Customer relationships Equipment (net) Goodwill Total assets 925,000 272,000 -0. 2.664.000 628.000 Liabilities Common stock (771,000) (400,000) (136,000) (100,000) Retained earnings (above) Total liabilities and equity (1,493,000) (2,664,000) (392,000) (628,000) Complete the assignment following the steps below. 1. Prepare a formal allocation of excess cost over book value for the acquisition. 2. Provide work to verify the amounts of equity income that Patrick records as well as the balance of investment in O'Brien. Income from O'Brien Investment in O'Brien 3. Review five consolidation entries: What do we do in Entry S? What does "S" stand for? What do we do in Entry A? What does "A" stand for? What do we do in Entry I? What does "T" stand for? What do we do in Entry D? What does "D" stand for? What do we do in Entry E? What does "E" stand for