Question

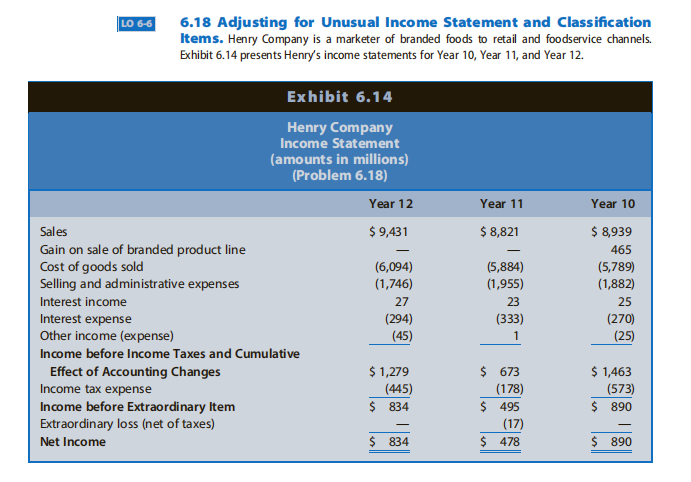

Notes to the fifinancial statements reveal the following information: 1. Gain on sale of a portion of the branded product line. In Year 10, Henry

Notes to the fifinancial statements reveal the following information:

1. Gain on sale of a portion of the branded product line. In Year 10, Henry completed

the sale of a portion of one of its branded product lines for $735 million. The transaction

resulted in a pretax gain of $464.5 million. The sale did not qualify as a discontinued

operation. Henry did not disclose the tax effect of the gain reported in Exhibit 6.14.

2. Extraordinary loss. In Year 11, Henry experienced an extraordinary loss when a subsidi

ary was expropriated during a military coup in a previously stable country. The loss was

$17 million, net of income taxes of $10 million. Note: Recently, U.S. GAAP and IFRS have

prohibited the extraordinary item classifification, which in the past was used to segregate

peripheral gains and losses that were unusual in nature and infrequent in occurrence.

Very few items were reported as extraordinary. Treat this item as you would treat any

infrequent peripheral gain or loss.

3. Sale and promotion costs. In Year 11, Henry changed the classifification of certain sale

and promotion incentives provided to customers and consumers. In the past, Henry clas

sifified these incentives as selling and administrative expenses (see Exhibit 6.14), with the

gross amount of the revenue associated with the incentives reported in sales. Beginning

in Year 11, Henry changed to reporting the incentives as a reduction of revenues. As a

result of this change, the fifirm reduced reported revenues by $693 million in Year 12,

$610 million in Year 11, and $469 million in Year 10. The fifirm stated that selling and

administrative expenses were correspondingly reduced such that net earnings were not

affected. Exhibit 6.14 already reflflects the adjustments to sales revenues and selling and

administrative expenses for Years 10 through 12.

4. Tax rate. The U.S. federal statutory income tax rate was 35% for each of the years pre

sented in Exhibit 6.14.

REQUIRED

a. Discuss whether you would adjust for each of the following items when using earnings

to forecast the future profifitability of Henry:

1. Gain on sale of a portion of the branded product line

2. Extraordinary loss

b. Indicate the adjustment you would make to Henrys net income for each item in Requirement a.

c. Discuss whether you believe the reclassifification adjustments made by Henry for the sale

and promotion incentive costs (Item 3) are appropriate.

d. Prepare a common-size income statement for Year 10, Year 11, and Year 12 using the

amounts in Exhibit 6.14. Set sales equal to 100%. Round percentages to one decimal

point.

e. Repeat Requirement d after making the income statement adjustments in Requirement b.

f. Assess the changes in the profifitability of Henry during the three-year period.

6.18 Adjusting for Unusual Income Statement and Classification Items. Henry Company is a marketer of branded foods to retail and foodservice channels. Exhibit 6.14 presents Henry's income statements for Year 10, Year 11, and Year 12. 6.18 Adjusting for Unusual Income Statement and Classification Items. Henry Company is a marketer of branded foods to retail and foodservice channels. Exhibit 6.14 presents Henry's income statements for Year 10, Year 11, and Year 12Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microfinance Handbook An Institutional And Financial Perspective

Authors: Joanna Ledgerwood

1st Edition

0821343068, 978-0821343067