Answered step by step

Verified Expert Solution

Question

1 Approved Answer

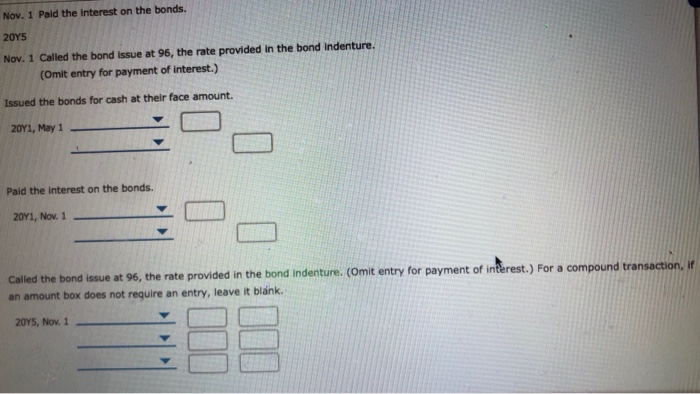

Nov. 1 Paid the interest on the bonds. 2045 Nov. 1 Called the bond issue at 96, the rate provided in the bond Indenture. (Omit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Clinical Audit For Doctors

Authors: Dr. Bob Ghosh, Sir Liam Donalson, Dr. Chen Sheng Low, Margaret Keane, Dr. Bhoresh Dhamija

1st Edition

1906839018, 978-1906839017