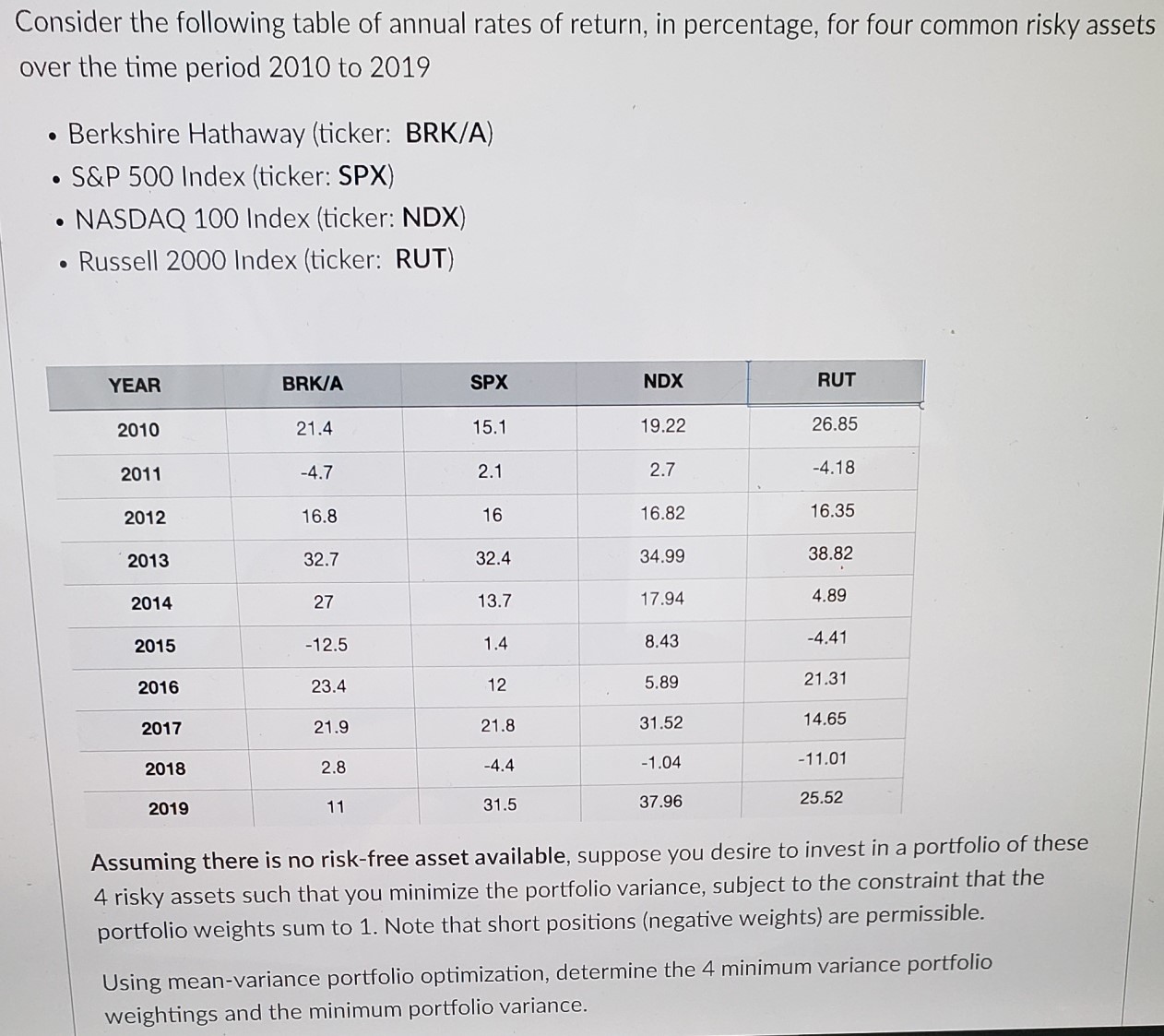

Question

Now assume there is a risk-free asset available and the annual risk-free rate is 2%. Using mean-variance portfolio theory, determine the 4 portfolio weightings and

Now assume there is a risk-free asset available and the annual risk-free rate is 2%. Using mean-variance portfolio theory, determine the 4 portfolio weightings and the portfolio variance for the unique fund F defined by the tangent portfolio and the one-fund theorem.

Note that the portfolio weights sum to 1 and short selling (negative weights) are permissible.

What is the portfolio weight for SPX in the unique fund F?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Estate Finance De Limmobilier

Authors: Thomas, Philippe, Romanet Perroux, Arnaud

1st Edition

2863255991, 9782863255995