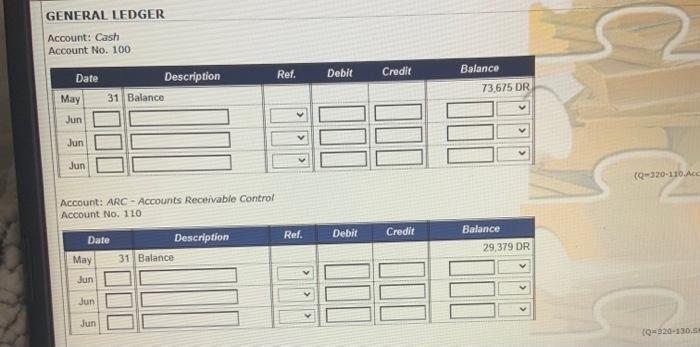

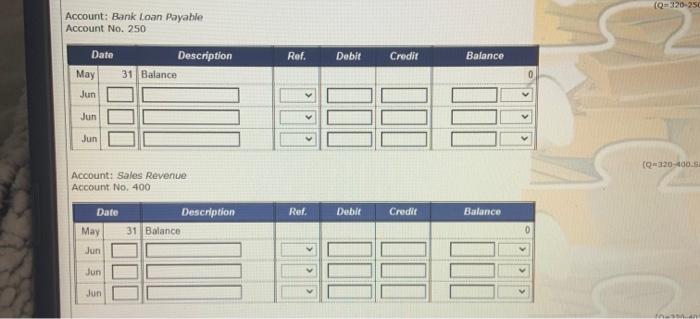

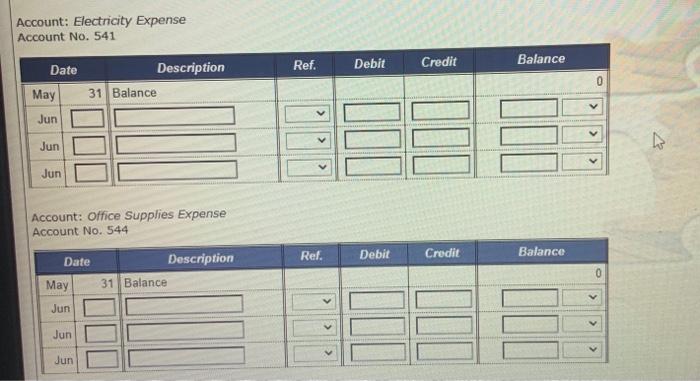

Now that you have reviewed information about Cover 2 Cover, you are ready to begin the first step in the accounting cycle, recording transactions. On this page of the practice set, you are asked to record transactions that occurred during the first week of June into the company's journals and post the appropriate entries to the ledger accounts. The following transactions occurred throughout the first week of June: Week 1 Date Transaction description 1 Issued Check No. 319 for $9,700 to pay ZNG Property Group for two month's worth of rent in advance. Issued Check No. 320 to Office Supplies Warehouse for the purchase of $451 worth of office supplies. Obtained a loan of $58,000 from BitiBank at a simple interest rate of 6% per year. The first interest payment is due at the end of August 2023 and the principal of the loan is to be repaid on June 1, 2028. 3 Paid the full amount owing to Peachson, Check No. 321. 3 Cough-up bookstore paid the full amount owing on their account. 4 Paid sales staff wages of $3,847 for the week up to and including yesterday, Check No. 322. Note that $2,191 of this payment relates to the wages expense incurred during the last week of May. 6 Made payment of $790 to Integer Energy for 3 months of electricity up to and including May 31, Check No. 323. After completing this practice set page, you should know how to record basic transactions in the journals provided below and understand the posting process in the manual accounting system. Note that you will record the remaining June transactions in the following sections of this practice set. Remember, one purpose of using special journals is to make the posting process more efficient by posting the total of most columns in the special joumals after all of the transactions for the period have been recorded. However, some parts of a journal entry are still required to be posted on a daily basis. View the company's accounting policies and procedures er for details of what is to be posted daily or monthly. Instructions for week 1 1) Record all week 1 transactions in the relevant journals. Note that special journais must be used where applicable. Any transaction that cannot be recorded in a special journal should be recorded in the general journal. 2) Post entries recorded in the journals to the appropriate ledger accounts according to the company's accounting policies and proceduresw. Account: Cash Account No. 100 Account: ARC - Accounts Receivable Control Account No, 110 Account: Bank Loan Payable Account No. 250 Account: Sales Revenue Account No. 400 Account: Electricity Expense Account No. 541 Account: Office Supplies Expense Account No. 544 Account: Sales Discounts Account No. 402 Account: Cost of Goods Sold Account No. 500 Account: Wages Expense Account No. 516