Answered step by step

Verified Expert Solution

Question

1 Approved Answer

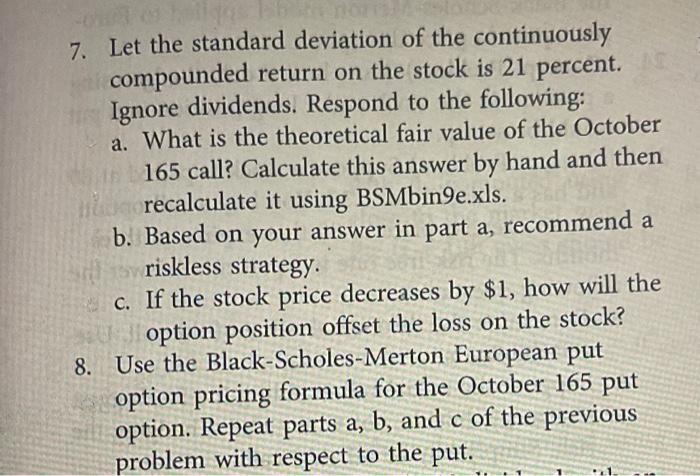

Number 8 and please explain 7. Let the standard deviation of the continuously compounded return on the stock is 21 percent Ignore dividends. Respond to

Number 8 and please explain

7. Let the standard deviation of the continuously compounded return on the stock is 21 percent Ignore dividends. Respond to the following: a. What is the theoretical fair value of the October 165 call? Calculate this answer by hand and then recalculate it using BSMbin9e.xls. b. Based on your answer in part a, recommend a riskless strategy c. If the stock price decreases by $1, how will the option position offset the loss on the stock? 8. Use the Black-Scholes-Merton European put option pricing formula for the October 165 put option. Repeat parts a, b, and c of the previous problem with respect to the put. Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Automated Stock Trading Systems

Authors: Laurens Bensdorp

1st Edition

1544506031, 978-1544506036