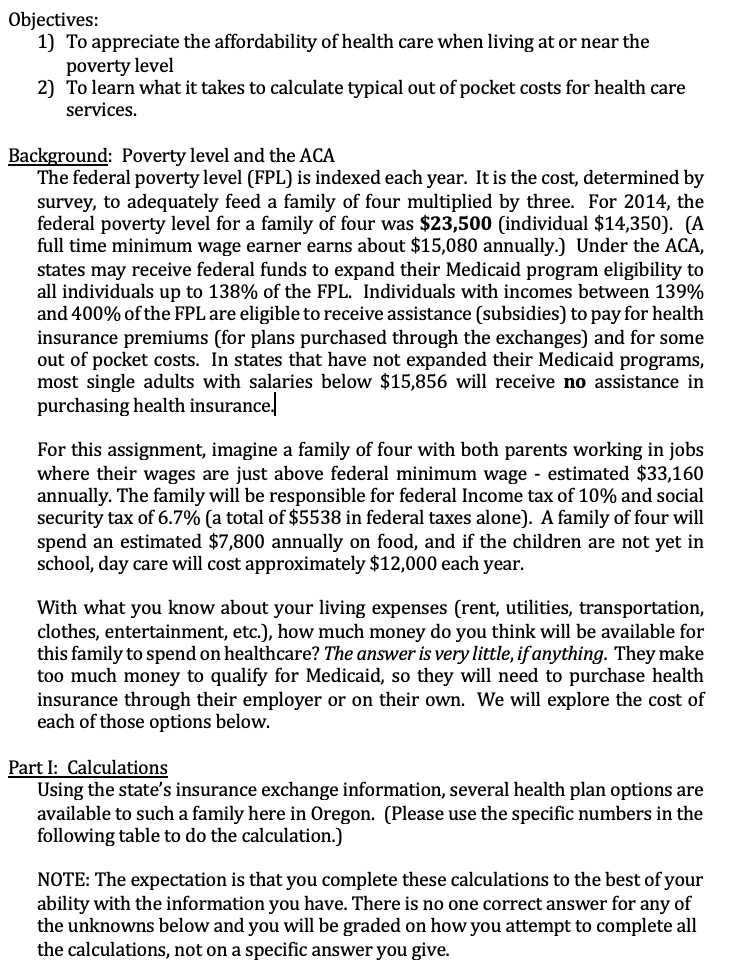

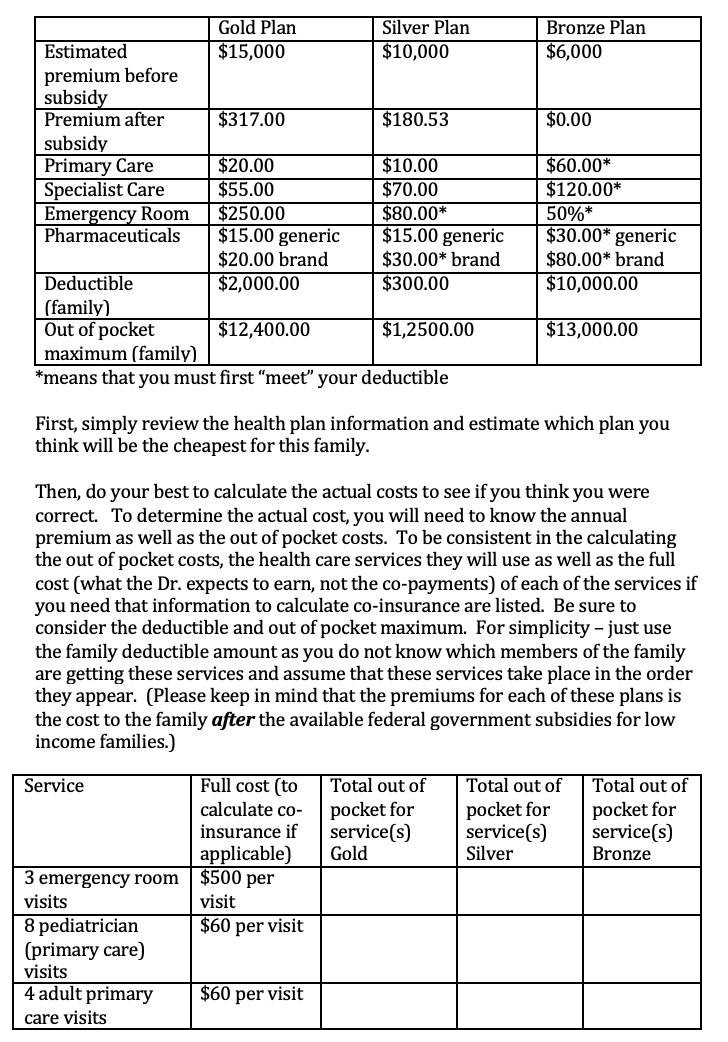

Objectives: 1) To appreciate the affordability of health care when living at or near the poverty level 2) To learn what it takes to calculate typical out of pocket costs for health care services. Background: Poverty level and the ACA The federal poverty level (FPL) is indexed each year. It is the cost, determined by survey, to adequately feed a family of four multiplied by three. For 2014, the federal poverty level for a family of four was $23,500 (individual $14,350). (A full time minimum wage earner earns about $15,080 annually.) Under the ACA, states may receive federal funds to expand their Medicaid program eligibility to all individuals up to 138% of the FPL. Individuals with incomes between 139% and 400% of the FPL are eligible to receive assistance (subsidies) to pay for health insurance premiums (for plans purchased through the exchanges) and for some out of pocket costs. In states that have not expanded their Medicaid programs, most single adults with salaries below $15,856 will receive no assistance in purchasing health insurance. For this assignment, imagine a family of four with both parents working in jobs where their wages are just above federal minimum wage - estimated $33,160 annually. The family will be responsible for federal Income tax of 10% and social security tax of 6.7% (a total of $5538 in federal taxes alone). A family of four will spend an estimated $7,800 annually on food, and if the children are not yet in school, day care will cost approximately $12,000 each year. With what you know about your living expenses (rent, utilities, transportation, clothes, entertainment, etc.), how much money do you think will be available for this family to spend on healthcare? The answer is very little, if anything. They make too much money to qualify for Medicaid, so they will need to purchase health insurance through their employer or on their own. We will explore the cost of each of those options below. Part I: Calculations Using the state's insurance exchange information, several health plan options are available to such a family here in Oregon. (Please use the specific numbers in the following table to do the calculation.) NOTE: The expectation is that you complete these calculations to the best of your ability with the information you have. There is no one correct answer for any of the unknowns below and you will be graded on how you attempt to complete all the calculations, not on a specific answer you give. Bronze Plan $6,000 $0.00 Gold Plan Silver Plan Estimated $15,000 $10,000 premium before subsidy Premium after $317.00 $180.53 subsidy Primary Care $20.00 $10.00 Specialist Care $55.00 $70.00 Emergency Room $250.00 $80.00* Pharmaceuticals $15.00 generic $15.00 generic $20.00 brand $30.00* brand Deductible $2,000.00 $300.00 (family) Out of pocket $12,400.00 $1,2500.00 maximum (family) *means that you must first meet your deductible $60.00* $120.00* 50%* $30.00* generic $80.00* brand $10,000.00 $13,000.00 First, simply review the health plan information and estimate which plan you think will be the cheapest for this family. Then, do your best to calculate the actual costs to see if you think you were correct. To determine the actual cost, you will need to know the annual premium as well as the out of pocket costs. To be consistent in the calculating the out of pocket costs, the health care services they will use as well as the full cost (what the Dr. expects to earn, not the co-payments) of each of the services if you need that information to calculate co-insurance are listed. Be sure to consider the deductible and out of pocket maximum. For simplicity - just use the family deductible amount as you do not know which members of the family are getting these services and assume that these services take place in the order they appear. (Please keep in mind that the premiums for each of these plans is the cost to the family after the available federal government subsidies for low income families.) Service Full cost to calculate co- insurance if applicable) Total out of pocket for service(s) Gold Total out of pocket for service(s) Silver Total out of pocket for service(s) Bronze $500 per visit $60 per visit 3 emergency room visits 8 pediatrician (primary care) visits 4 adult primary care visits $60 per visit $120 per visit $15.00 per Rx per 4 specialists physician visits 2 generic medications each month Total out of pocket costs Annual Premium month TOTAL COSTS (premium and out of pocket costs) Monthly premium x 12 Premium + out of pocket costs II. Family with employer based coverage. Now, compare what you found above with a family receiving insurance through their employer (still earning the same salary). Using national average premiums and co-insurance, the typical costs for an employer provided plan are listed below. Service Health plan co- insurance $100 per visit Total out of pocket for services $1500 (deductible) $23 per visit $23 per visit $184 (23 *8) $142 (23*4) 3 emergency room visits (two different kids 8 pediatrician visits 4 primary care visits for the parents 4 specialists visits 2 generic medications each month Total out of pocket costs $35 per visit $10.00 per Rx per month XXXXXX $140 (35*4) $240 (10*2*12) $2,206 Annual Premium XXXXXX $4,565 XXXXXX $6,771 TOTAL COSTS (premium and out of pocket costs)