Question

Objectives To develop an ability to identify and assume an assigned role. To be able to identify and rank the importance of explicit issues. To

Objectives

- To develop an ability to identify and assume an assigned role.

- To be able to identify and rank the importance of explicit issues.

- To illustrate the importance of hidden (undirected) issues that arise from a detailed analysis.

- To identify accounting issues (GAAP/IFRS compliance issues), assess their implications, generate alternatives, and provide recommendations within the bounds of GAAP/IFRS to meet the clients needs.

- To examine how accounting standards impact financial measures (ratios, covenants, etc.).

- To prepare a coherent report and integrated analysis that meets specific user needs.

Instructions In order to complete your case analysis successfully

- identify the role you are playing

- assess the financial reporting landscape considering the user needs, constraints, and business environment,

- identify the issues,

- analyze the issues (qualitatively and quantitatively), and

- provide a recommendation and conclusi

An average grade will result from answering all questions with basic coverage and accuracy, showing all your work. Additional points come from including greater detail, astute, informed commentary where appropriate and connections to readings and other content.

Respond in a single Word doc (or comparable text editor).

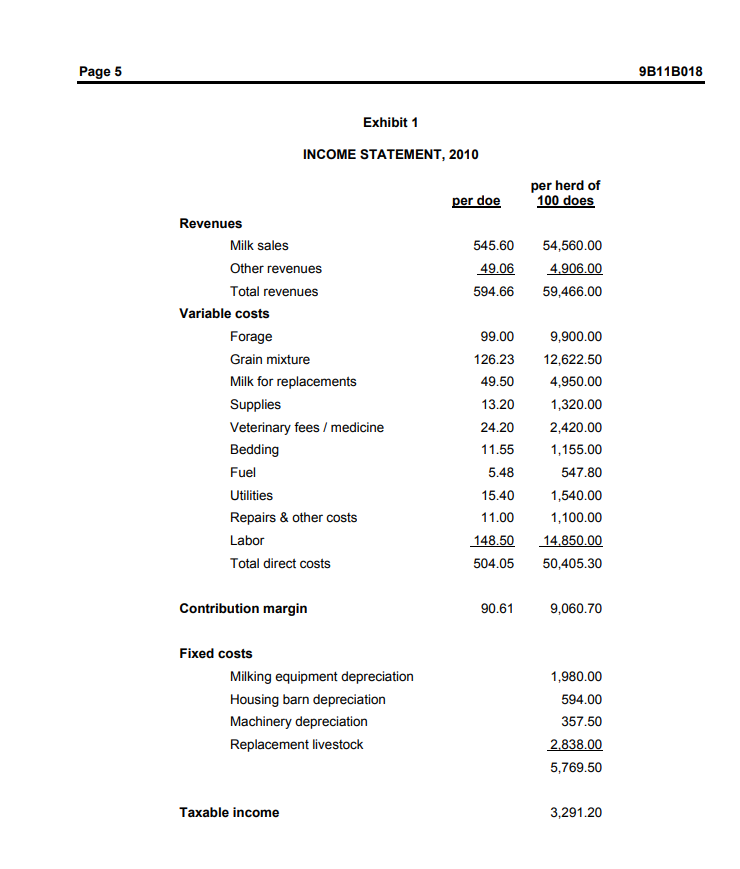

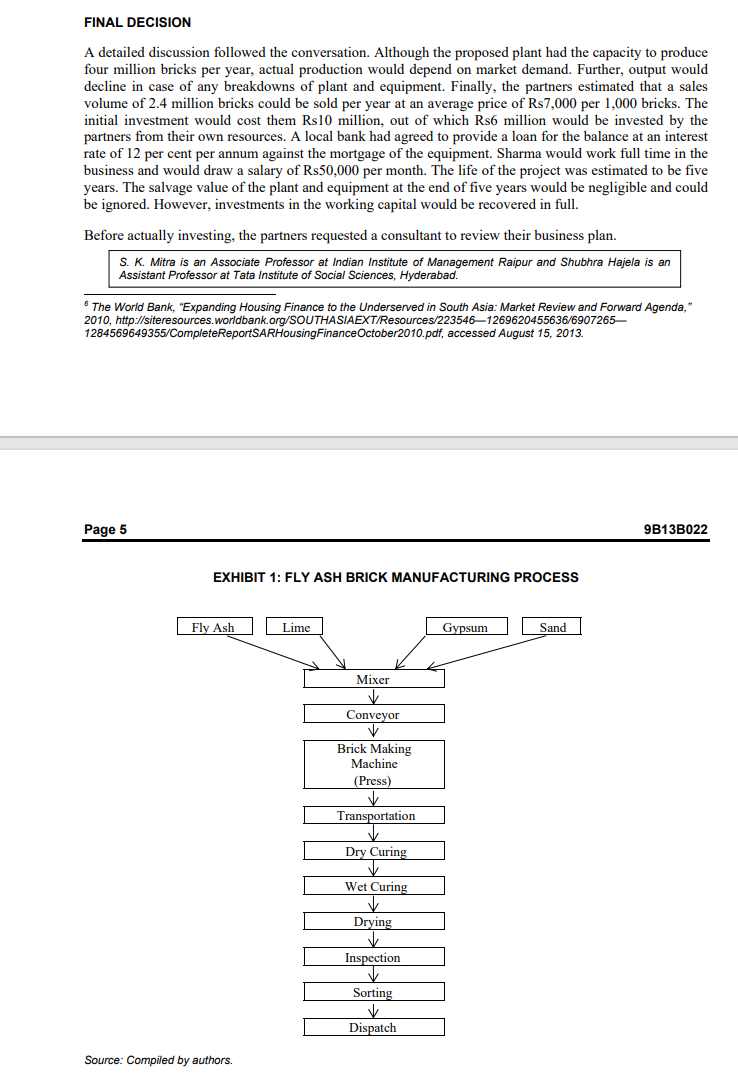

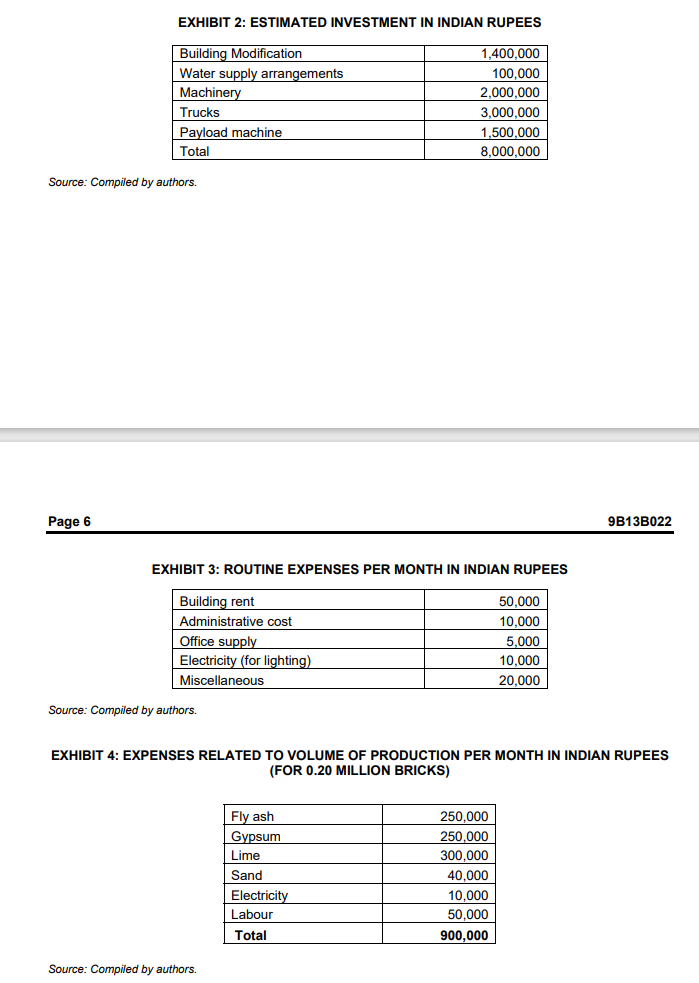

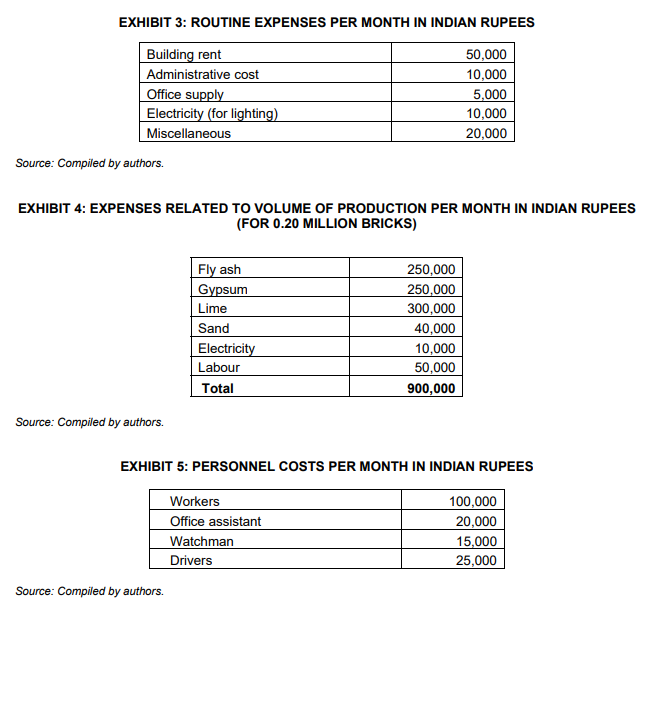

Page 5 9B11B018 Exhibit 1 INCOME STATEMENT, 2010 per doe per herd of 100 does 545.60 49.06 594.66 54,560.00 4.906.00 59,466.00 Revenues Milk sales Other revenues Total revenues Variable costs Forage Grain mixture Milk for replacements Supplies Veterinary fees / medicine Bedding Fuel Utilities Repairs & other costs Labor Total direct costs 99.00 126.23 49.50 13.20 24.20 11.55 5.48 15.40 11.00 148.50 504.05 9,900.00 12,622.50 4,950.00 1,320.00 2,420.00 1,155.00 547.80 1,540.00 1,100.00 14.850.00 50,405.30 Contribution margin 90.61 9,060.70 Fixed costs Milking equipment depreciation Housing barn depreciation Machinery depreciation Replacement livestock 1,980.00 594.00 357.50 2.838.00 5,769.50 Taxable income 3,291.20 FINAL DECISION A detailed discussion followed the conversation. Although the proposed plant had the capacity to produce four million bricks per year, actual production would depend on market demand. Further, output would decline in case of any breakdowns of plant and equipment. Finally, the partners estimated that a sales volume of 2.4 million bricks could be sold per year at an average price of Rs7,000 per 1,000 bricks. The initial investment would cost them Rs 10 million, out of which Rs6 million would be invested by the partners from their own resources. local bank had agreed to provide a loan for the balance at an interest rate of 12 per cent per annum against the mortgage of the equipment. Sharma would work full time in the business and would draw a salary of Rs50,000 per month. The life of the project was estimated to be five years. The salvage value of the plant and equipment at the end of five years would be negligible and could be ignored. However, investments in the working capital would be recovered in full. Before actually investing, the partners requested a consultant to review their business plan. S. K. Mitra is an Associate Professor at Indian Institute of Management Raipur and Shubhra Hajela is an Assistant Professor at Tata Institute of Social Sciences, Hyderabad. The World Bank, "Expanding Housing Finance to the Underserved in South Asia: Market Review and Forward Agenda," 2010, http://siteresources.worldbank.org/SOUTHASIAEXT/Resources/2235461269620455636/6907265 1284569649355/CompleteReportSARHousing Finance October 2010.pdf, accessed August 15, 2013. Page 5 9B13B022 EXHIBIT 1: FLY ASH BRICK MANUFACTURING PROCESS Fly Ash Lime Gypsum Sand Mixer Conveyor Brick Making Machine (Press) Transportation Dry Curing Wet Curing Drying Inspection V Sorting Dispatch Source: Compiled by authors. EXHIBIT 2: ESTIMATED INVESTMENT IN INDIAN RUPEES Building Modification Water supply arrangements Machinery Trucks Payload machine Total 1,400,000 100,000 2,000,000 3,000,000 1,500,000 8,000,000 Source: Compiled by authors. Page 6 9B13B022 EXHIBIT 3: ROUTINE EXPENSES PER MONTH IN INDIAN RUPEES Building rent Administrative cost Office supply Electricity (for lighting) Miscellaneous 50,000 10,000 5,000 10,000 20,000 Source: Compiled by authors. EXHIBIT 4: EXPENSES RELATED TO VOLUME OF PRODUCTION PER MONTH IN INDIAN RUPEES (FOR 0.20 MILLION BRICKS) Fly ash Gypsum Lime Sand Electricity Labour Total 250,000 250,000 300,000 40,000 10,000 50.000 900,000 Source: Compiled by authors. EXHIBIT 3: ROUTINE EXPENSES PER MONTH IN INDIAN RUPEES Building rent Administrative cost Office supply Electricity (for lighting) Miscellaneous Source: Compiled by authors. 50,000 10,000 5,000 10,000 20,000 EXHIBIT 4: EXPENSES RELATED TO VOLUME OF PRODUCTION PER MONTH IN INDIAN RUPEES (FOR 0.20 MILLION BRICKS) Fly ash Gypsum Lime Sand Electricity Labour Total 250,000 250,000 300,000 40,000 10,000 50,000 900,000 Source: Compiled by authors. EXHIBIT 5: PERSONNEL COSTS PER MONTH IN INDIAN RUPEES Workers Office assistant Watchman Drivers 100,000 20,000 15,000 25,000 Source: Compiled by authors. Page 5 9B11B018 Exhibit 1 INCOME STATEMENT, 2010 per doe per herd of 100 does 545.60 49.06 594.66 54,560.00 4.906.00 59,466.00 Revenues Milk sales Other revenues Total revenues Variable costs Forage Grain mixture Milk for replacements Supplies Veterinary fees / medicine Bedding Fuel Utilities Repairs & other costs Labor Total direct costs 99.00 126.23 49.50 13.20 24.20 11.55 5.48 15.40 11.00 148.50 504.05 9,900.00 12,622.50 4,950.00 1,320.00 2,420.00 1,155.00 547.80 1,540.00 1,100.00 14.850.00 50,405.30 Contribution margin 90.61 9,060.70 Fixed costs Milking equipment depreciation Housing barn depreciation Machinery depreciation Replacement livestock 1,980.00 594.00 357.50 2.838.00 5,769.50 Taxable income 3,291.20 FINAL DECISION A detailed discussion followed the conversation. Although the proposed plant had the capacity to produce four million bricks per year, actual production would depend on market demand. Further, output would decline in case of any breakdowns of plant and equipment. Finally, the partners estimated that a sales volume of 2.4 million bricks could be sold per year at an average price of Rs7,000 per 1,000 bricks. The initial investment would cost them Rs 10 million, out of which Rs6 million would be invested by the partners from their own resources. local bank had agreed to provide a loan for the balance at an interest rate of 12 per cent per annum against the mortgage of the equipment. Sharma would work full time in the business and would draw a salary of Rs50,000 per month. The life of the project was estimated to be five years. The salvage value of the plant and equipment at the end of five years would be negligible and could be ignored. However, investments in the working capital would be recovered in full. Before actually investing, the partners requested a consultant to review their business plan. S. K. Mitra is an Associate Professor at Indian Institute of Management Raipur and Shubhra Hajela is an Assistant Professor at Tata Institute of Social Sciences, Hyderabad. The World Bank, "Expanding Housing Finance to the Underserved in South Asia: Market Review and Forward Agenda," 2010, http://siteresources.worldbank.org/SOUTHASIAEXT/Resources/2235461269620455636/6907265 1284569649355/CompleteReportSARHousing Finance October 2010.pdf, accessed August 15, 2013. Page 5 9B13B022 EXHIBIT 1: FLY ASH BRICK MANUFACTURING PROCESS Fly Ash Lime Gypsum Sand Mixer Conveyor Brick Making Machine (Press) Transportation Dry Curing Wet Curing Drying Inspection V Sorting Dispatch Source: Compiled by authors. EXHIBIT 2: ESTIMATED INVESTMENT IN INDIAN RUPEES Building Modification Water supply arrangements Machinery Trucks Payload machine Total 1,400,000 100,000 2,000,000 3,000,000 1,500,000 8,000,000 Source: Compiled by authors. Page 6 9B13B022 EXHIBIT 3: ROUTINE EXPENSES PER MONTH IN INDIAN RUPEES Building rent Administrative cost Office supply Electricity (for lighting) Miscellaneous 50,000 10,000 5,000 10,000 20,000 Source: Compiled by authors. EXHIBIT 4: EXPENSES RELATED TO VOLUME OF PRODUCTION PER MONTH IN INDIAN RUPEES (FOR 0.20 MILLION BRICKS) Fly ash Gypsum Lime Sand Electricity Labour Total 250,000 250,000 300,000 40,000 10,000 50.000 900,000 Source: Compiled by authors. EXHIBIT 3: ROUTINE EXPENSES PER MONTH IN INDIAN RUPEES Building rent Administrative cost Office supply Electricity (for lighting) Miscellaneous Source: Compiled by authors. 50,000 10,000 5,000 10,000 20,000 EXHIBIT 4: EXPENSES RELATED TO VOLUME OF PRODUCTION PER MONTH IN INDIAN RUPEES (FOR 0.20 MILLION BRICKS) Fly ash Gypsum Lime Sand Electricity Labour Total 250,000 250,000 300,000 40,000 10,000 50,000 900,000 Source: Compiled by authors. EXHIBIT 5: PERSONNEL COSTS PER MONTH IN INDIAN RUPEES Workers Office assistant Watchman Drivers 100,000 20,000 15,000 25,000 Source: Compiled by authors

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Supply Chain Management Accounting Managing Profitability Working Capital And Asset Utilization

Authors: Simon Templar

1st Edition

0749472995, 978-0749472993