Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Old MathJax webview make project report on all question is full need project report on all os Handbook on Strategic Cost Management & Performance Evaluation

Old MathJax webview

make project report on all

question is full need project report on all

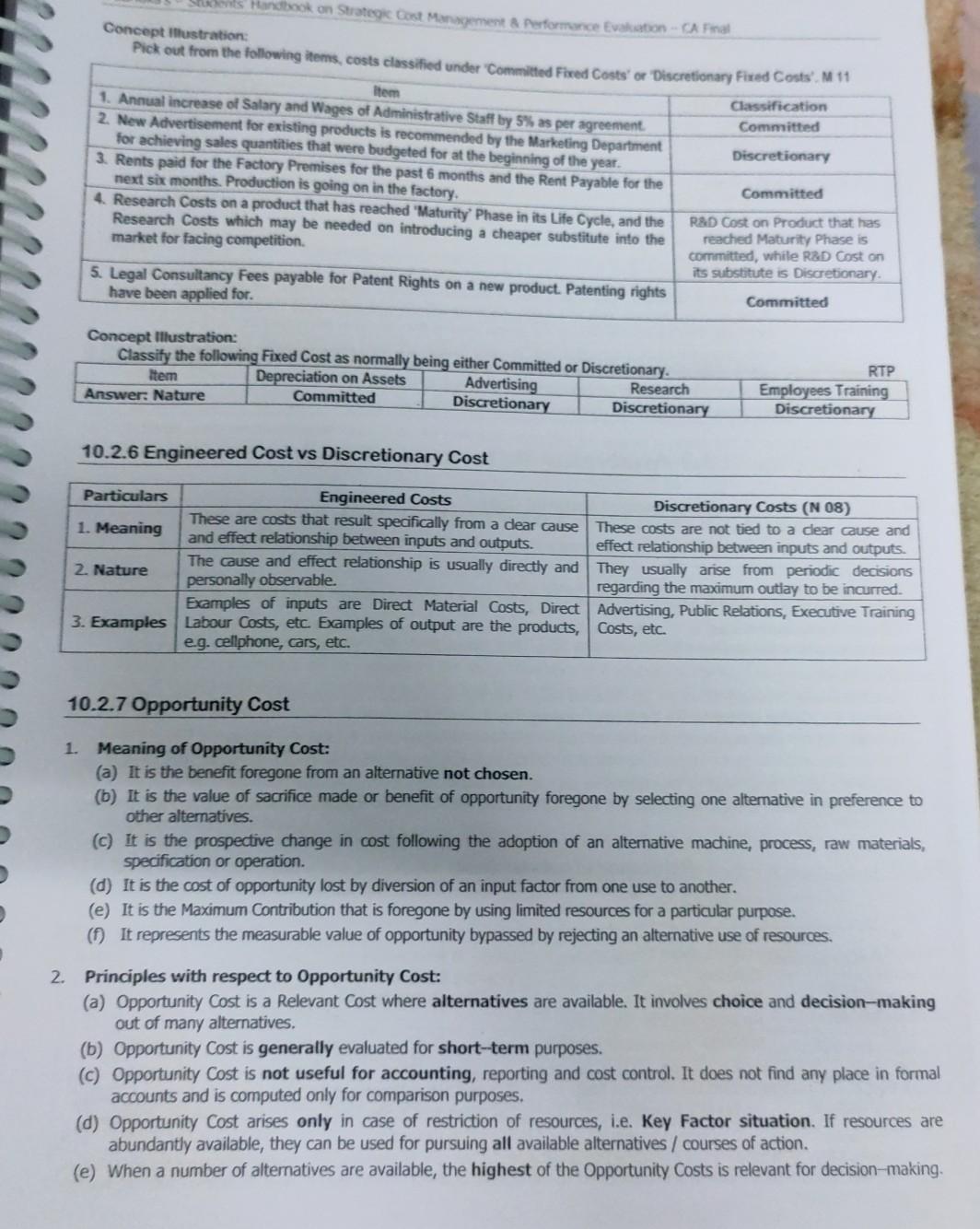

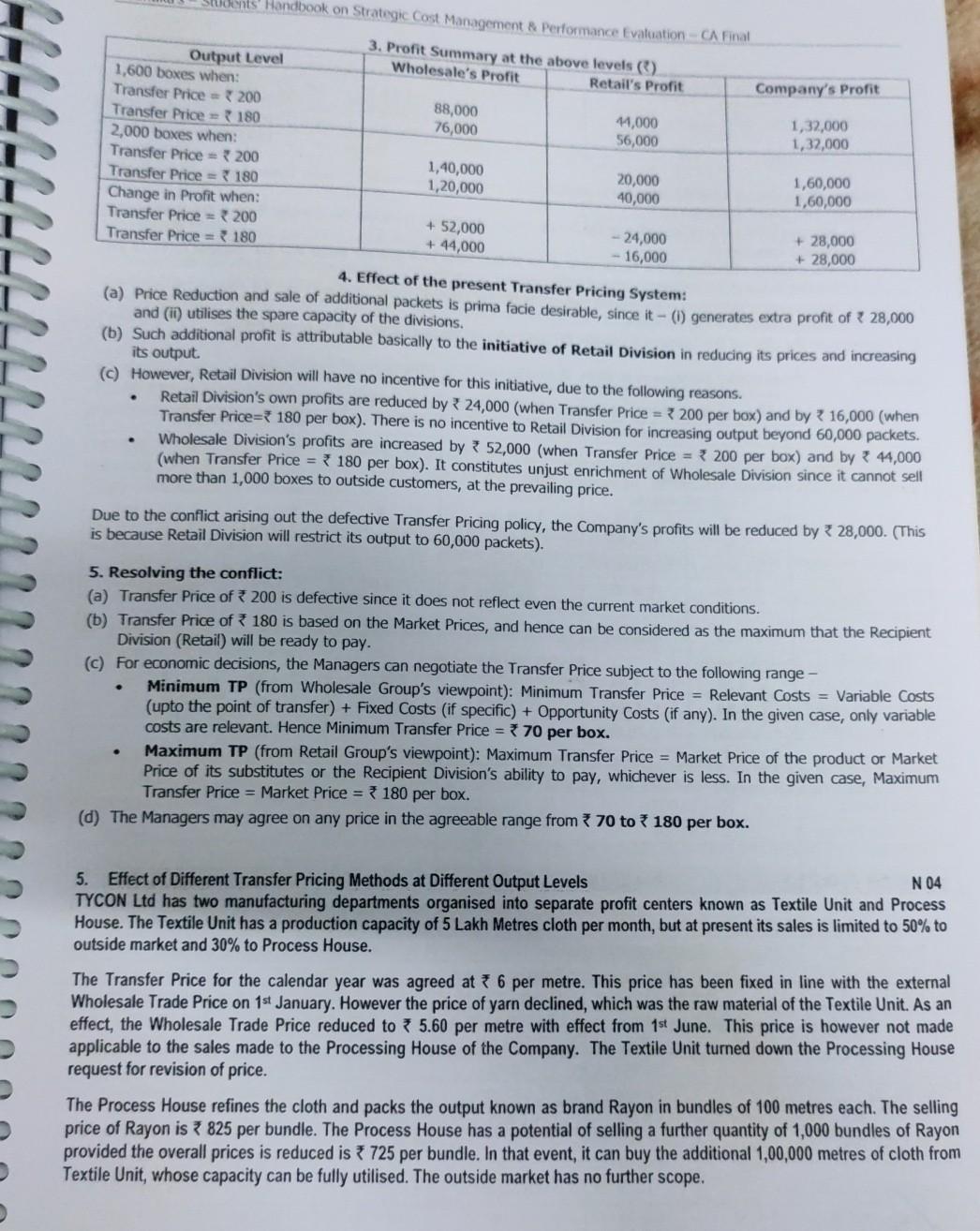

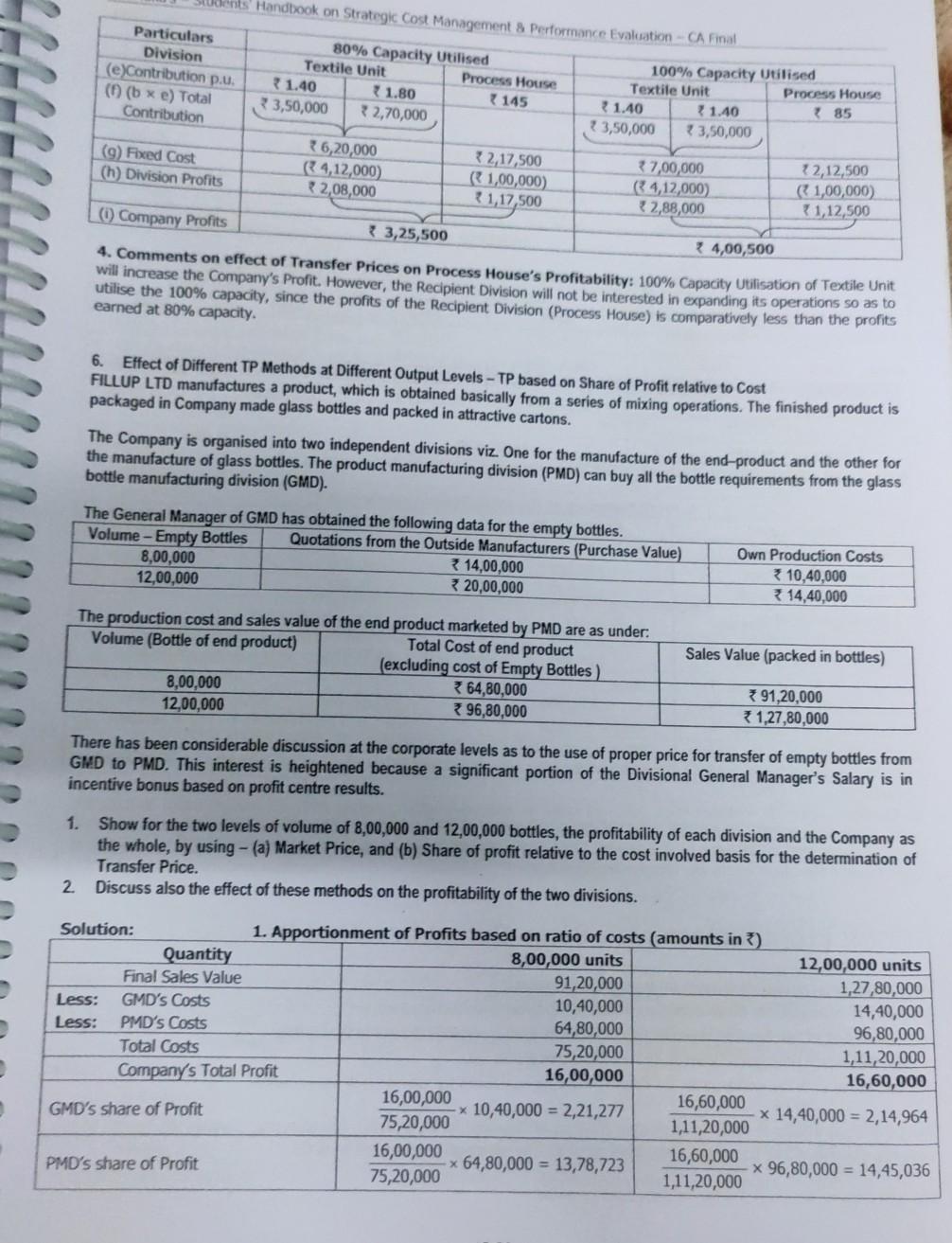

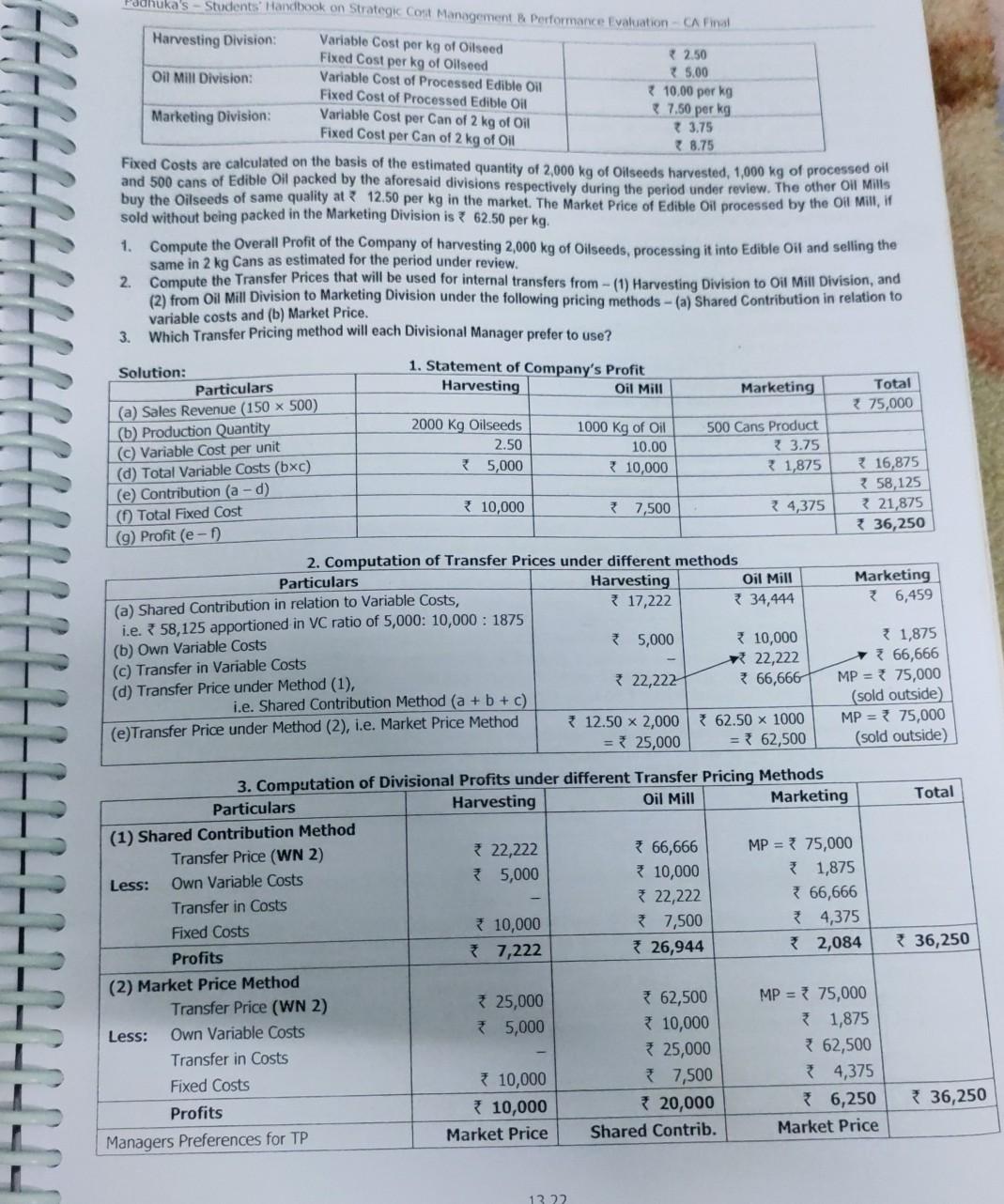

os Handbook on Strategic Cost Management & Performance Evaluation - CA Final Concept Mustration: Pick out from the following items, costs classified under Committed Fixed Costs' or Discretionary Fixed Conts'. M 11 Item Classification 1. Annual increase of Salary and Wages of Administrative Staff by 5% as per agreement Committed 2. New Advertisement for existing products is recommended by the Marketing Department for achieving sales quantities that were budgeted for at the beginning of the year. Discretionary 3. Rents paid for the Factory Premises for the past 6 months and the Rent Payable for the next six months. Production is going on in the factory Committed 4. Research Costs on a product that has reached "Maturity Phase in its Life Cycle, and the RSD Cost on Product that has Research Costs which may be needed on introducing a cheaper substitute into the reached Maturity Phase is market for facing competition committed, while R&D Cost on its substitute is Discretionary. 5. Legal Consultancy Fees payable for Patent Rights on a new product. Patenting rights Committed have been applied for. Concept Illustration: Classify the following Fixed Cost as normally being either Committed or Discretionary. Item Depreciation on Assets Advertising Research Answer: Nature Committed Discretionary Discretionary RTP Employees Training Discretionary 10.2.6 Engineered Cost vs Discretionary Cost Particulars Engineered Costs Discretionary Costs (N 08) These are costs that result specifically from a dear cause 1. Meaning These costs are not tied to a clear cause and and effect relationship between inputs and outputs. effect relationship between inputs and outputs. The cause and effect relationship is usually directly and They usually arise from periodic decisions 2. Nature personally observable. regarding the maximum outiay to be incurred. Examples of inputs are Direct Material Costs, Direct Advertising, Public Relations, Executive Training 3. Examples Labour costs, etc. Examples of output are the products, Costs, etc. e.g. cellphone, cars, etc. 10.2.7 Opportunity Cost 1. Meaning of Opportunity Cost: (a) It is the benefit foregone from an alternative not chosen. (b) It is the value of sacrifice made or benefit of opportunity foregone by selecting one alternative in preference to other alternatives. (C) It is the prospective change in cost following the adoption of an alternative machine, process, raw materials, specification or operation. (d) It is the cost of opportunity lost by diversion of an input factor from one use to another. (e) It is the Maximum Contribution that is foregone by using limited resources for a particular purpose. It represents the measurable value of opportunity bypassed by rejecting an alternative use of resources. 2. Principles with respect to Opportunity Cost: (a) Opportunity cost is a Relevant Cost where alternatives are available. It involves choice and decision-making out of many alternatives. (b) Opportunity cost is generally evaluated for short-term purposes. (C) Opportunity Cost is not useful for accounting, reporting and cost control. It does not find any place in formal accounts and is computed only for comparison purposes. (d) Opportunity Cost arises only in case of restriction of resources, i.e. Key Factor situation. If resources are abundantly available, they can be used for pursuing all available alternatives / courses of action. (e) When a number of alternatives are available, the highest of the Opportunity Costs is relevant for decision-making. Company's Profit Sudents' Handbook on Strategic Cost Management Performance Evaluation CA Final 3. Profit Summary at the above levels ). Output Level Wholesale's Profit Retail's Profit 1,600 boxes when: Transfer Price = 200 88,000 44,000 Transfer Price 180 76,000 56,000 2,000 boxes when: Transfer Price = 200 1,40,000 Transfer Price => 180 1,20,000 40,000 Change in Profit when: Transfer Price 200 + 52,000 - 24,000 Transfer Price => 180 + 44,000 16,000 1,32,000 1,32,000 20,000 1,60,000 1,60,000 + 28,000 + 28,000 4. Effect of the present Transfer Pricing System: (a) Price Reduction and sale of additional packets is prima facie desirable, since it - (1) generates extra profit of 28,000 and (11) utilises the spare capacity of the divisions. (b) Such additional profit is attributable basically to the initiative of Retail Division in reducing its prices and increasing its output (c) However, Retail Division will have no incentive for this initiative, due to the following reasons. Retail Division's own profits are reduced by 24,000 (when Transfer Price = 200 per box) and by ? 16,000 (when Transfer Price={ 180 per box). There is no incentive to Retail Division for increasing output beyond 60,000 packets. Wholesale Division's profits are increased by 52,000 (when Transfer Price = * 200 per box) and by 44,000 (when Transfer Price = 180 per box). It constitutes unjust enrichment of Wholesale Division since it cannot sell more than 1,000 boxes to outside customers, at the prevailing price. Due to the conflict arising out the defective Transfer Pricing policy, the Company's profits will be reduced by 328,000. (This is because Retail Division will restrict its output to 60,000 packets). 5. Resolving the conflict: (a) Transfer Price of 200 is defective since it does not reflect even the current market conditions. (b) Transfer Price of 180 is based on the Market Prices, and hence can be considered as the maximum that the recipient Division (Retail) will be ready to pay. (c) For economic decisions, the Managers can negotiate the Transfer Price subject to the following range - Minimum TP (from Wholesale Group's viewpoint): Minimum Transfer Price = Relevant Costs = Variable Costs (upto the point of transfer) + Fixed Costs (if specific) + Opportunity Costs (if any). In the given case, only variable costs are relevant. Hence Minimum Transfer Price = 70 per box. Maximum TP (from Retail Group's viewpoint): Maximum Transfer Price = Market Price of the product or Market Price of its substitutes or the Recipient Division's ability to pay, whichever is less. In the given case, Maximum Transfer Price = Market Price = 180 per box. (d) The Managers may agree on any price in the agreeable range from 70 to 180 per box. 5. Effect of Different Transfer Pricing Methods at Different Output Levels N 04 TYCON Ltd has two manufacturing departments organised into separate profit centers known as Textile Unit and Process House. The Textile Unit has a production capacity of 5 Lakh Metres cloth per month, but at present its sales is limited to 50% to outside market and 30% to Process House. The Transfer Price for the calendar year was agreed at 6 per metre. This price has been fixed in line with the external Wholesale Trade Price on 1st January. However the price of yarn declined, which was the raw material of the Textile Unit. As an effect, the Wholesale Trade Price reduced to 5.60 per metre with effect from 1st June. This price is however not made applicable to the sales made to the Processing House of the Company. The Textile Unit turned down the Processing House request for revision of price. The Process House refines the cloth and packs the output known as brand Rayon in bundles of 100 metres each. The selling price of Rayon is 825 per bundle. The Process House has a potential of selling a further quantity of 1,000 bundles of Rayon provided the overall prices is reduced is * 725 per bundle. In that event, it can buy the additional 1,00,000 metres of cloth from Textile Unit, whose capacity can be fully utilised. The outside market has no further scope. ents Handbook on Strategic Cost Management & Performance Evaluation - CA Final Particulars 80% Capacity Utilised 100% Capacity Utilised Division Textile Unit Process House Textile Unit Process House (e)Contribution p.u. 1.40 1.80 145 * 1.40 1.40 ( (bx e) Total 33,50,000 32,70,000 23,50,000 83,50,000 Contribution 76,20,000 32,17,500 37,00,000 (9) Fixed Cost 4,12,000) (1,00,000) (4,12,000) (h) Division Profits 2,08,000 31,17,500 2,88,000 385 22,12,500 (P 1,00,000) 1,12,500 Company ProfitsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cost Accounting

Authors: Edward B. Deakin, Michael Maher

3rd Edition

0256069190, 978-0256069198