Answered step by step

Verified Expert Solution

Question

1 Approved Answer

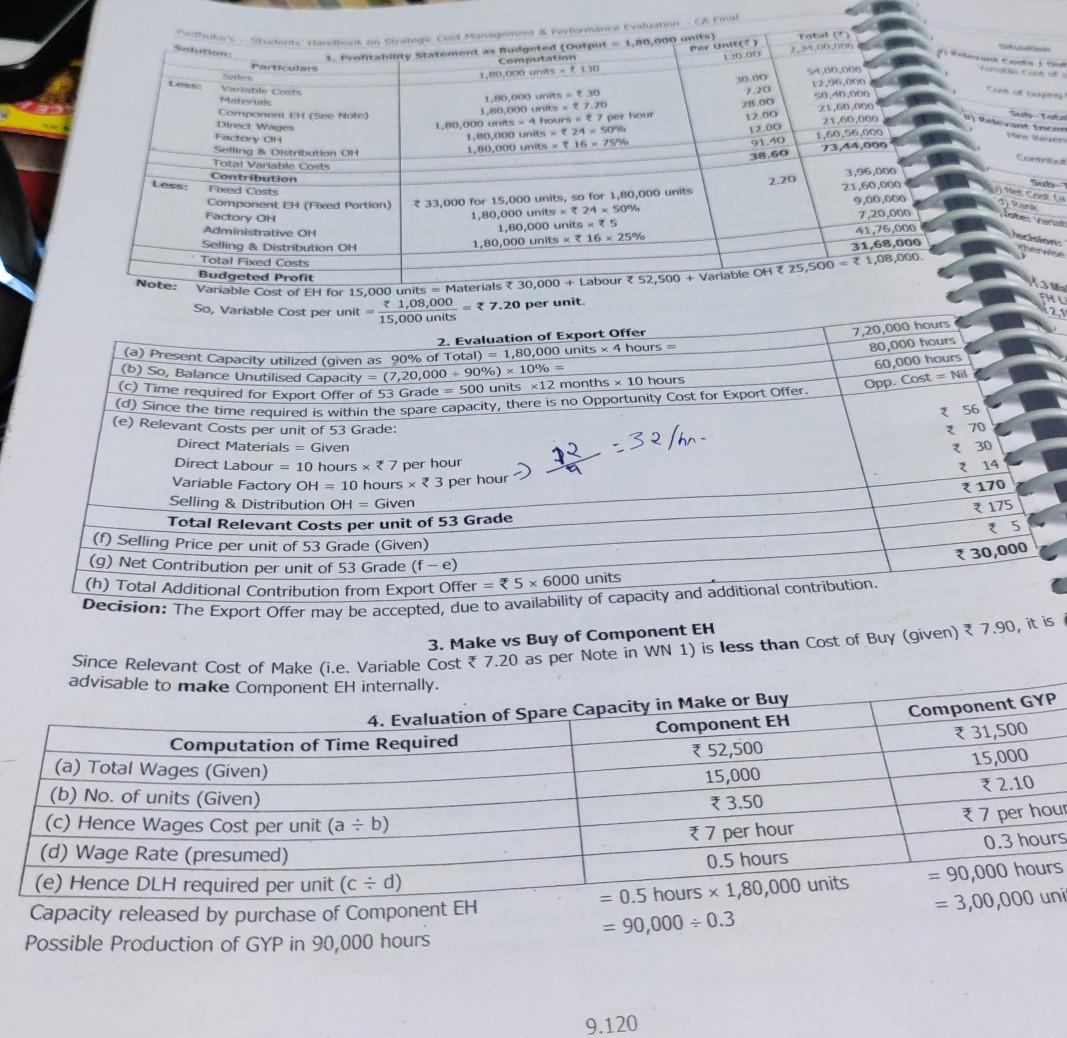

Old MathJax webview need project report on all question is complete at 3. per unit) ED Parts Proty Statements Budget (output 1,000 Computation 1,600,000 0.00

Old MathJax webview

need project report on all

question is complete

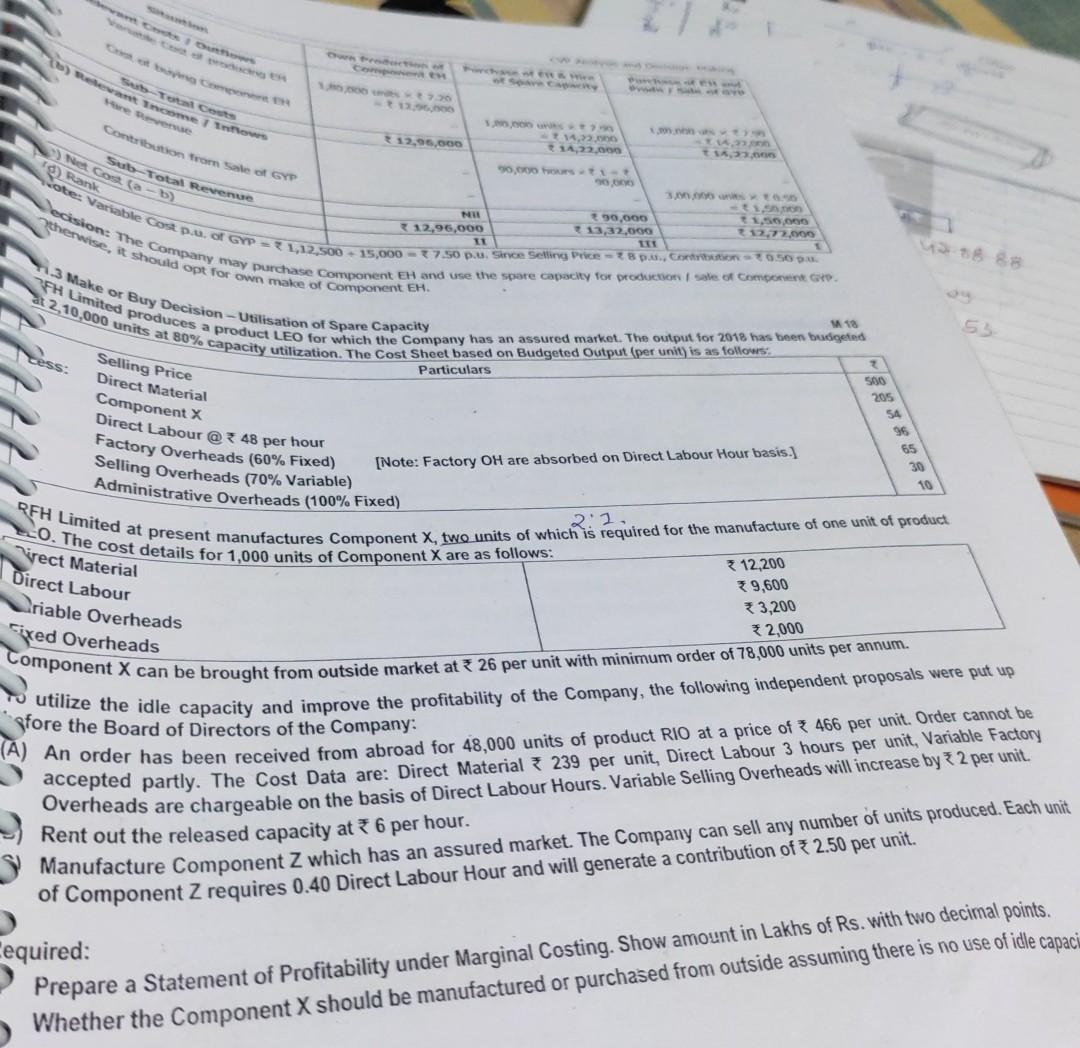

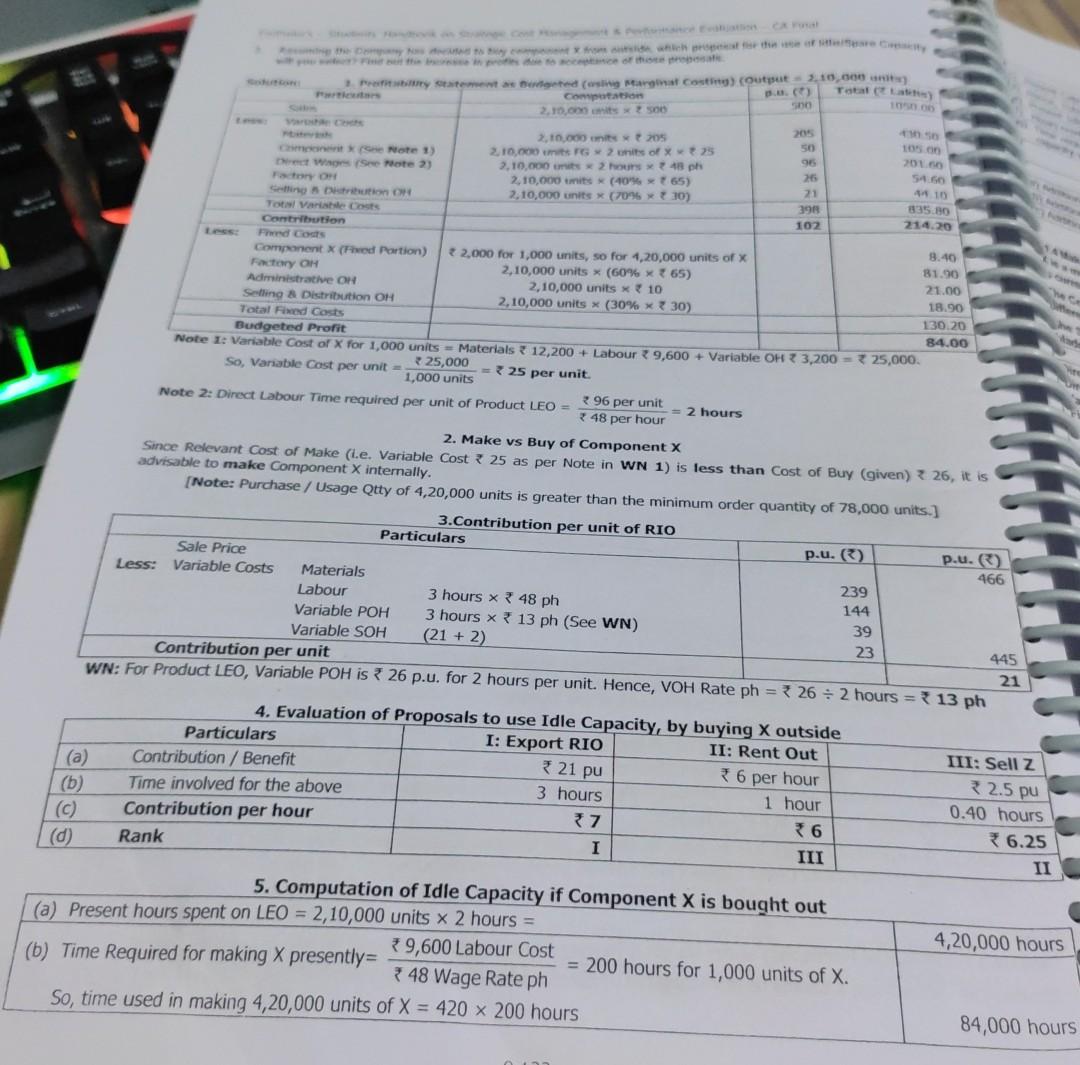

at 3. per unit) ED Parts Proty Statements Budget (output 1,000 Computation 1,600,000 0.00 7.20 28.00 12.00 1,500,000 1,80,000.7.20 1,800,000 hours per hour 1.80,000 24 50 1,80,000 unit 16 75% . 12.96.0 40.C 21.60. 21.50.000 1,60,56.000 73,44,000 12.00 140 38.60 2.20 Componente Mote) red was Factory OH Setting Distribution on Total Variable costs Contribution Fored Costs Componenten (Fixed portion) Factory OH Administrative OH Selling & Distribution OH Total Fixed Costs Budgeted Profit Variable Cost of EH for 15,000 units - Materials 30,000 + Labour 3 52,500 + Variable OH 25.SOO 21.08,000 So, Variable Cost per unit 33,000 for 15,000 units, so for 1,80,000 units 1,80,000 units x 24 x 50% 1,80,000 units 5 1,80,000 units X 16 25% 3.96.000 21,60,000 9,00,000 7,20,000 41,76,000 31,68,000 ed Where Note: 37.20 per unit. * 1,08,000 15,000 units PH 2. 7,20,000 hours 80,000 hours 60,000 hours Opp. Cost = Nil Present Capacity utilized (given as 90% of total) -21,80,000 units + 4 hours = So, Balance Unutilised Capacity - 7,20,000 - 90%) 10% = for Export Offer. (C) Time required for Export Offer of 53 Grade = 500 units x12 months x 10 hours (e) Relevant Costs per unit of 53 Grade: Direct Materials = Given Direct Labour = 10 hours x7 per hour -32 356 70 30 14 170 175 5 30,000 Selling & Distribution OH = Given Total Relevant Costs per unit of 53 Grade (1) Selling Price per unit of 53 Grade (Given) (9) Net Contribution per unit of 53 Grade (f-e) (h) Total Additional Contribution from Export Offer = * 5 * 6000 units Decision: The Export Offer may be accepted, due to availability of capacity and additional contribution. 3. Make vs Buy of Component EH advisable to make Component EH internally. Since Relevant Cost of Make (i.e. Variable Cost * 7.20 as per Note in WN 1) is less than Cost of Buy given)* 7.90, it is 4. Evaluation of Spare Capacity in Make or Buy Computation of Time Required Component EH Component GYP 52,500 331,500 15,000 15,000 3.50 2.10 7 per hour 7 per hour 0.5 hours 0.3 hours Capacity released by purchase of Component EH = 0.5 hours x 1,80,000 units = 90,000 hours Possible Production of GYP in 90,000 hours = 90,000 = 0.3 = 3,00,000 uni (a) Total Wages (Given) (b) No. of units (Given) (C) Hence Wages Cost per unit (a : b) (d) Wage Rate (presumed) (e) Hence DLH required per unit (C = d) 9.120 1 O Com Vincent Set To Go he Contribution tror sale of GY 12,96,000 14,22.00 1,300 1,30 Het Cost (a - b) 9) Rank Sub-Total Revenue 90.00 50 -11 90,000 1,50.000 votes Variable Costu, o GYP12500 - 15.000 27.50 .. Srce Soling Price Contos MU 13,32,000 212.72.000 12,96,000 therwise, it should opt for own make of Component EH. ecision: The Company may purchase Component EH and use the spare capacity for production Sale of Com 7.3 Make or Buy Decision - Utilisation of Spare Capacity 118 FH Limited produces a product LEO for which the Company has an assured market. The output for 2018 has been budged 2,10,000 units at 80% capacity utilization. The Cost Sheet based on Budgeted Output (per unit) is as followers Particulars 53 tess: Selling Price Direct Material Component X 500 205 54 Direct Labour @ 48 per hour Factory Overheads (60% Fixed) Selling Overheads (70% Variable) Administrative Overheads (100% Fixed) 36 65 lote: Factory OH are absorbed on Direct Labour Hour basis.) 30 10 REH Limited at present manufactures Component X, two units of which is required for the manufacture of one unit of product LO. The cost details for 1,000 units of Component X are as follows: 2:2 12,200 9,600 3,200 2,000 Component X can be brought from outside market at 26 per unit with minimum order of 78,000 units per annum. rect Material Direct Labour riable Overheads Cred Overheads utilize the idle capacity and improve the profitability of the Company , the following independent proposals were put up (A) An order has been received for commabroad for 48.000 units of product Rio at a price of 7 466 per unit. Order cannot be accepted partly. The Cost Data are: Direct Material * 239 per unit, Direct Labour 3 hours per unit, Variable Factory Overheads are chargeable on the basis of Direct Labour Hours. Variable Selling Overheads will increase by + 2 per unit Rent out the released capacity at 6 per hour. Manufacture Component Z which has an assured market. The Company can sell any number of units produced. Each unit of Component Z requires 0.40 Direct Labour Hour and will generate a contribution of 2.50 per unit. Cequired: Prepare a Statement of Profitability under Marginal Costing. Show amount in Lakhs of Rs. with two decimal points. Whether the Component X should be manufactured or purchased from outside assuming there is no use of idle capaci. the side whether tre Total Setements Bed (sy Margas Costa (output 2,10,000 Computation 2.10.000 500 835.10 205 2.000 i 205 50 105. Notes 2,10,000 units of 33 2016 Det W/Sete 2) 2.10,000 min 45 ph 26 54.60 Factory OH 2,10,000 units (165) 21 441 Son om 2,10,000 units X (709510) 398 Tot varte costs Contribution 102 214.20 Fred Gods 8.40 Component X (Fed Portion) 2,000 for 1,000 units, so for 4,20,000 units of Factory OH 81.00 2,10,000 unitsStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ressourceneffizientes Wirtschaften

Authors: Heinz Karl Prammer

2nd Edition

3658046082, 9783658046088