Answered step by step

Verified Expert Solution

Question

1 Approved Answer

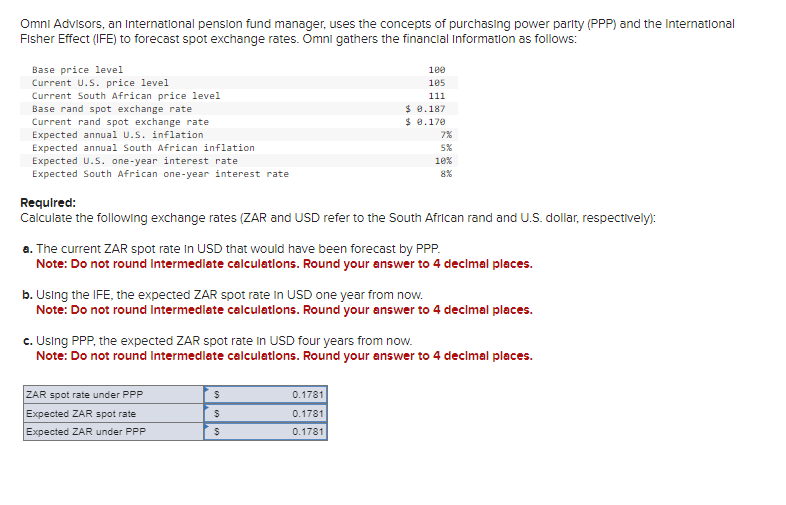

Omni Advisors, an International pension fund manager, uses the concepts of purchasing power parity (PPP) and the International Fisher Effect (IFE) to forecast spot

Omni Advisors, an International pension fund manager, uses the concepts of purchasing power parity (PPP) and the International Fisher Effect (IFE) to forecast spot exchange rates. Omni gathers the financial Information as follows: Base price level Current U.S. price level Current South African price level Base rand spot exchange rate Current rand spot exchange rate Expected annual U.S. inflation Expected annual South African inflation 100 105 111 $ 0.187 $ 0.170 7% 5% 10% 8% Expected U.S. one-year interest rate Expected South African one-year interest rate Required: Calculate the following exchange rates (ZAR and USD refer to the South African rand and U.S. dollar, respectively): a. The current ZAR spot rate in USD that would have been forecast by PPP. Note: Do not round intermediate calculations. Round your answer to 4 decimal places. b. Using the IFE, the expected ZAR spot rate in USD one year from now. Note: Do not round intermediate calculations. Round your answer to 4 decimal places. c. Using PPP, the expected ZAR spot rate in USD four years from now. Note: Do not round intermediate calculations. Round your answer to 4 decimal places. ZAR spot rate under PPP $ 0.1781 Expected ZAR spot rate $ 0.1781 Expected ZAR under PPP $ 0.1781

Step by Step Solution

★★★★★

3.48 Rating (145 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the exchange rates using the concepts of purchasing power parity PPP and ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657