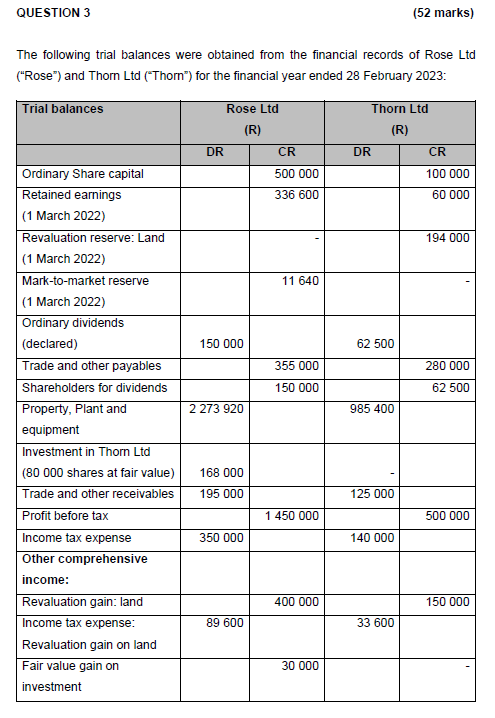

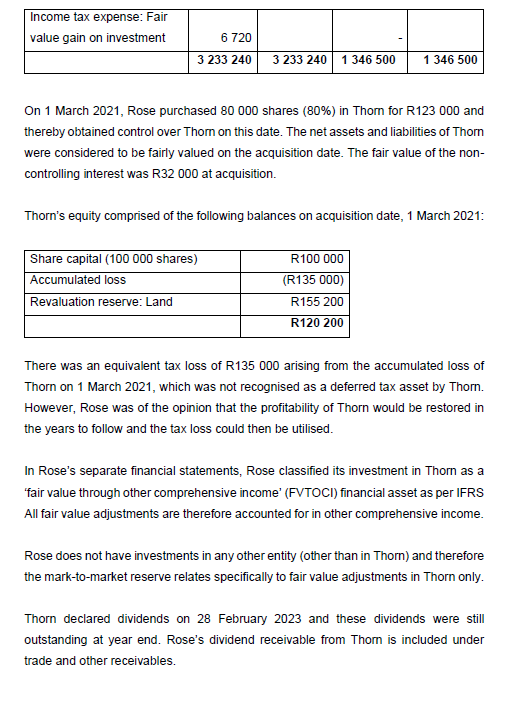

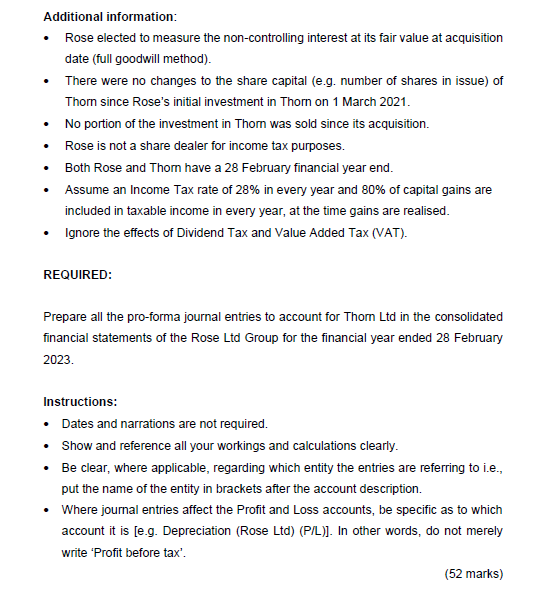

On 1 March 2021, Rose purchased 80000 shares (80\%) in Thorn for R123 000 and thereby obtained control over Thorn on this date. The net assets and liabilities of Thorn were considered to be fairly valued on the acquisition date. The fair value of the noncontrolling interest was R32 000 at acquisition. Thorn's equity comprised of the following balances on acquisition date, 1 March 2021: There was an equivalent tax loss of R135 000 arising from the accumulated loss of Thorn on 1 March 2021, which was not recognised as a deferred tax asset by Thorn. However, Rose was of the opinion that the profitability of Thorn would be restored in the years to follow and the tax loss could then be utilised. In Rose's separate financial statements, Rose classified its investment in Thorn as a 'fair value through other comprehensive income' (FVTOCl) financial asset as per IFRS All fair value adjustments are therefore accounted for in other comprehensive income. Rose does not have investments in any other entity (other than in Thorn) and therefore the mark-to-market reserve relates specifically to fair value adjustments in Thorn only. Thorn declared dividends on 28 February 2023 and these dividends were still outstanding at year end. Rose's dividend receivable from Thorn is included under trade and other receivables. Additional information: - Rose elected to measure the non-controlling interest at its fair value at acquisition date (full goodwill method). - There were no changes to the share capital (e.g. number of shares in issue) of Thorn since Rose's initial investment in Thorn on 1 March 2021. - No portion of the investment in Thorn was sold since its acquisition. - Rose is not a share dealer for income tax purposes. - Both Rose and Thorn have a 28 February financial year end. - Assume an Income Tax rate of 28% in every year and 80% of capital gains are included in taxable income in every year, at the time gains are realised. - Ignore the effects of Dividend Tax and Value Added Tax (VAT). REQUIRED: Prepare all the pro-forma journal entries to account for Thorn Ltd in the consolidated financial statements of the Rose Ltd Group for the financial year ended 28 February 2023. Instructions: - Dates and narrations are not required. - Show and reference all your workings and calculations clearly. - Be clear, where applicable, regarding which entity the entries are referring to i.e., put the name of the entity in brackets after the account description. - Where journal entries affect the Profit and Loss accounts, be specific as to which account it is [e.g. Depreciation (Rose Ltd) (P/L)]. In other words, do not merely write 'Profit before tax'. (52 marks) The following trial balances were obtained from the financial records of Rose Ltd On 1 March 2021, Rose purchased 80000 shares (80\%) in Thorn for R123 000 and thereby obtained control over Thorn on this date. The net assets and liabilities of Thorn were considered to be fairly valued on the acquisition date. The fair value of the noncontrolling interest was R32 000 at acquisition. Thorn's equity comprised of the following balances on acquisition date, 1 March 2021: There was an equivalent tax loss of R135 000 arising from the accumulated loss of Thorn on 1 March 2021, which was not recognised as a deferred tax asset by Thorn. However, Rose was of the opinion that the profitability of Thorn would be restored in the years to follow and the tax loss could then be utilised. In Rose's separate financial statements, Rose classified its investment in Thorn as a 'fair value through other comprehensive income' (FVTOCl) financial asset as per IFRS All fair value adjustments are therefore accounted for in other comprehensive income. Rose does not have investments in any other entity (other than in Thorn) and therefore the mark-to-market reserve relates specifically to fair value adjustments in Thorn only. Thorn declared dividends on 28 February 2023 and these dividends were still outstanding at year end. Rose's dividend receivable from Thorn is included under trade and other receivables. Additional information: - Rose elected to measure the non-controlling interest at its fair value at acquisition date (full goodwill method). - There were no changes to the share capital (e.g. number of shares in issue) of Thorn since Rose's initial investment in Thorn on 1 March 2021. - No portion of the investment in Thorn was sold since its acquisition. - Rose is not a share dealer for income tax purposes. - Both Rose and Thorn have a 28 February financial year end. - Assume an Income Tax rate of 28% in every year and 80% of capital gains are included in taxable income in every year, at the time gains are realised. - Ignore the effects of Dividend Tax and Value Added Tax (VAT). REQUIRED: Prepare all the pro-forma journal entries to account for Thorn Ltd in the consolidated financial statements of the Rose Ltd Group for the financial year ended 28 February 2023. Instructions: - Dates and narrations are not required. - Show and reference all your workings and calculations clearly. - Be clear, where applicable, regarding which entity the entries are referring to i.e., put the name of the entity in brackets after the account description. - Where journal entries affect the Profit and Loss accounts, be specific as to which account it is [e.g. Depreciation (Rose Ltd) (P/L)]. In other words, do not merely write 'Profit before tax'. (52 marks) The following trial balances were obtained from the financial records of Rose Ltd