Question

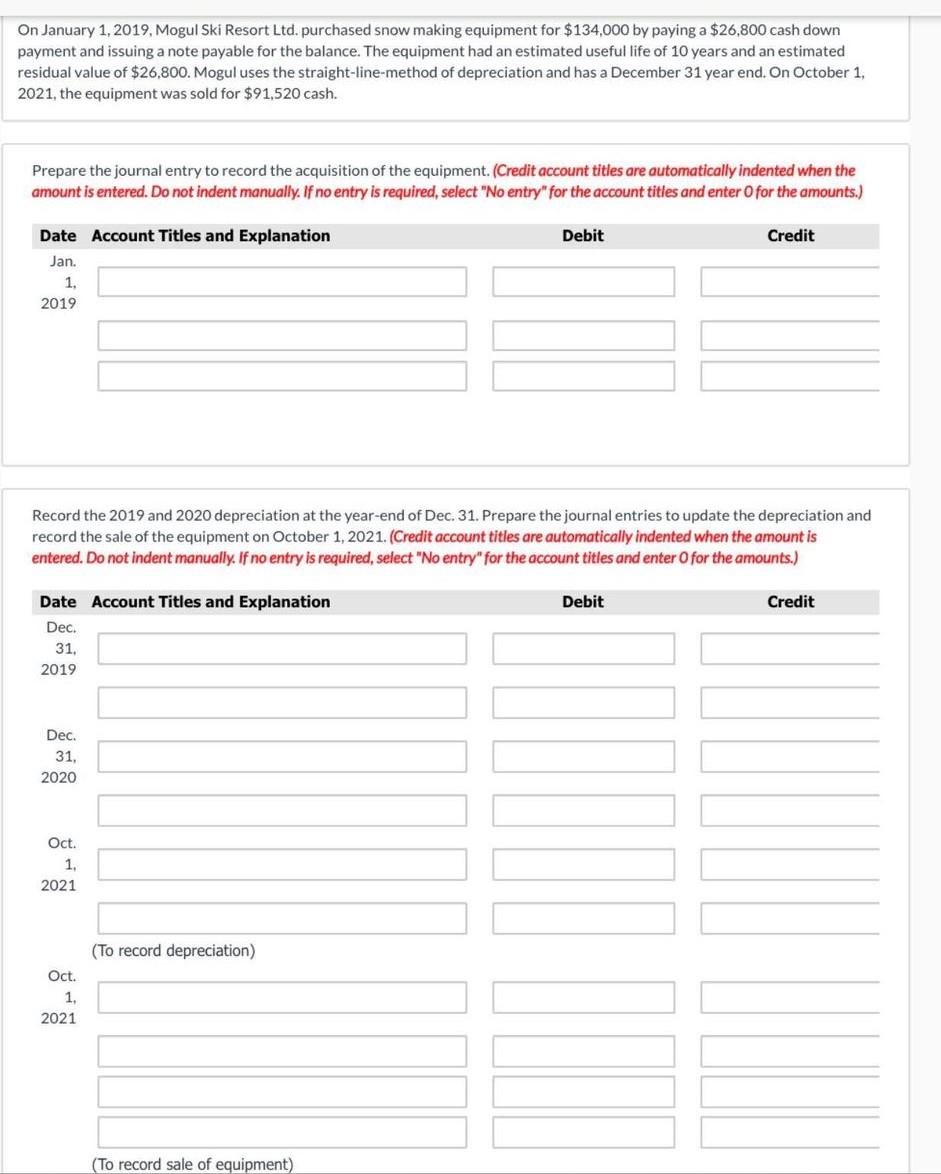

On january 1, 2019, Mogul ski resort Ltd. Purchased snow making equipment for $134,000 by paying a $26,800 cash down payment and issuing a note

On january 1, 2019, Mogul ski resort Ltd. Purchased snow making equipment for $134,000 by paying a $26,800 cash down payment and issuing a note payable for the balance. The equipment had an estimated useful life of 10 years and an estimated residual value of $26,800. Mogul uses the straight-line-method of depreciation and has a december 31 year end. On october 1, 2021, the equipment was sold for $91,520 cash.

Please explain entry for Oct 1st 2021 - record sale of equipment

Please explain entry for Oct 1st 2021 - record sale of equipment

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Loose Leaf Fundamental Financial Accounting Concepts

Authors: Thomas Edmonds, Frances McNair, Philip Olds

8th Edition

0077433807, 978-0077433802