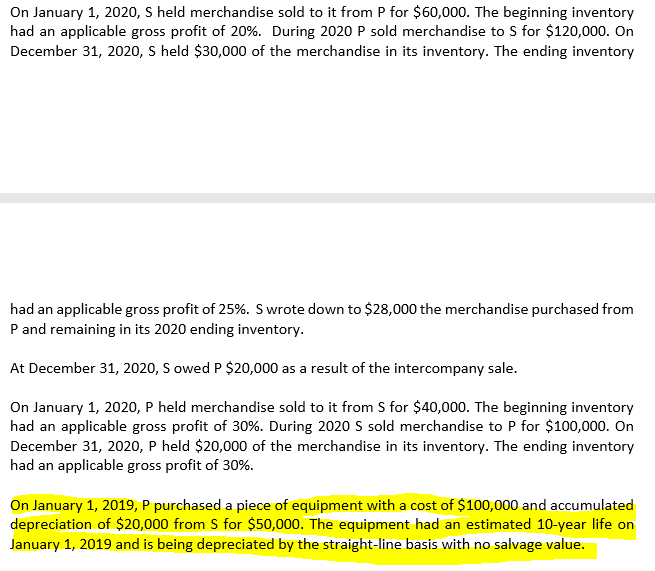

On January 1, 2019, P purchased a piece of equipment with a cost of $100,000 and accumulated depreciation of $20,000 from S for $50,000. The equipment had an estimated 10-year life on January 1, 2019 and is being depreciated by the straight-line basis with no salvage value.

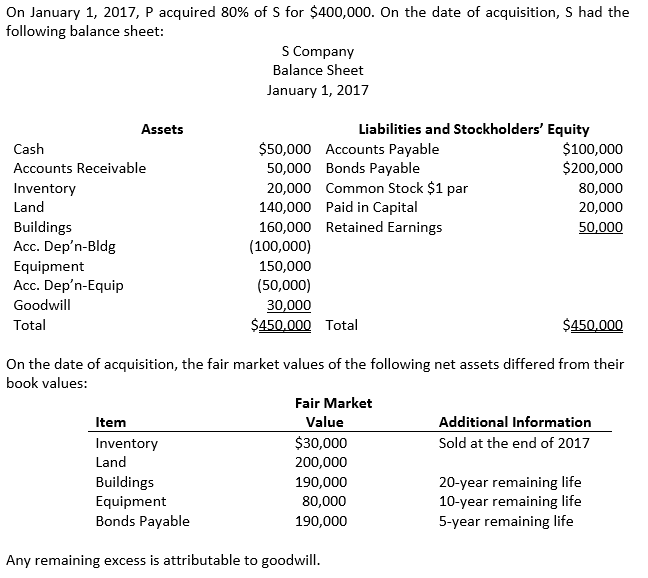

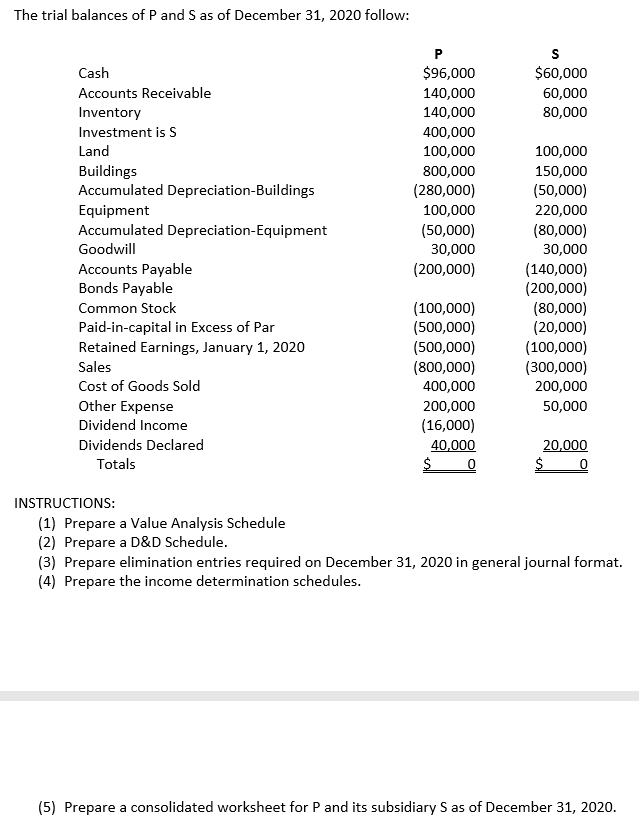

On January 1, 2017, P acquired 80% f S for $400,000. On the date of acquisition, S had the following balance sheet: S Company Balance Sheet January 1, 2017 Assets Cash Accounts Receivable Inventory Land Buildings Acc. Dep'n-Bldg Equipment Acc. Dep'n-Equip Goodwill Total Liabilities and Stockholders' Equity $50,000 Accounts Payable $100,000 50,000 Bonds Payable $200,000 20,000 Common Stock $1 par 80,000 140,000 Paid in Capital 20,000 160,000 Retained Earnings 50,000 (100,000) 150,000 (50,000) 30,000 $450.000 Total $450,000 On the date of acquisition, the fair market values of the following net assets differed from their book values: Fair Market Item Value Additional Information Inventory $30,000 Sold at the end of 2017 Land 200,000 Buildings 190,000 20-year remaining life Equipment 80,000 10-year remaining life Bonds Payable 190,000 5-year remaining life Any remaining excess is attributable to goodwill. On January 1, 2020, S held merchandise sold to it from P for $60,000. The beginning inventory had an applicable gross profit of 20%. During 2020 P sold merchandise to S for $120,000. On December 31, 2020, S held $30,000 of the merchandise in its inventory. The ending inventory had an applicable gross profit of 25%. S wrote down to $28,000 the merchandise purchased from P and remaining in its 2020 ending inventory. At December 31, 2020, Sowed P $20,000 as a result of the intercompany sale. On January 1, 2020, P held merchandise sold to it from S for $40,000. The beginning inventory had an applicable gross profit of 30%. During 2020 S sold merchandise to P for $100,000. On December 31, 2020, P held $20,000 of the merchandise in its inventory. The ending inventory had an applicable gross profit of 30%. On January 1, 2019, P purchased a piece of equipment with a cost of $100,000 and accumulated depreciation of $20,000 from S for $50,000. The equipment had an estimated 10-year life on January 1, 2019 and is being depreciated by the straight-line basis with no salvage value. The trial balances of P and S as of December 31, 2020 follow: S $60,000 60,000 80,000 Cash Accounts Receivable Inventory Investment is s Land Buildings Accumulated Depreciation-Buildings Equipment Accumulated Depreciation Equipment Goodwill Accounts Payable Bonds Payable Common Stock Paid-in-capital in Excess of Par Retained Earnings, January 1, 2020 Sales Cost of Goods Sold Other Expense Dividend Income Dividends Declared Totals P $96,000 140,000 140,000 400,000 100,000 800,000 (280,000) 100,000 (50,000) 30,000 (200,000) 100,000 150,000 (50,000) 220,000 (80,000) 30,000 (140,000) (200,000) (80,000) (20,000) (100,000) (300,000) 200,000 50,000 (100,000) (500,000) (500,000) (800,000) 400,000 200,000 (16,000) 40,000 0 20.000 $ 0 $ INSTRUCTIONS: (1) Prepare a Value Analysis Schedule (2) Prepare a D&D Schedule. (3) Prepare elimination entries required on December 31, 2020 in general journal format. (4) Prepare the income determination schedules. (5) Prepare a consolidated worksheet for P and its subsidiary S as of December 31, 2020. On January 1, 2017, P acquired 80% f S for $400,000. On the date of acquisition, S had the following balance sheet: S Company Balance Sheet January 1, 2017 Assets Cash Accounts Receivable Inventory Land Buildings Acc. Dep'n-Bldg Equipment Acc. Dep'n-Equip Goodwill Total Liabilities and Stockholders' Equity $50,000 Accounts Payable $100,000 50,000 Bonds Payable $200,000 20,000 Common Stock $1 par 80,000 140,000 Paid in Capital 20,000 160,000 Retained Earnings 50,000 (100,000) 150,000 (50,000) 30,000 $450.000 Total $450,000 On the date of acquisition, the fair market values of the following net assets differed from their book values: Fair Market Item Value Additional Information Inventory $30,000 Sold at the end of 2017 Land 200,000 Buildings 190,000 20-year remaining life Equipment 80,000 10-year remaining life Bonds Payable 190,000 5-year remaining life Any remaining excess is attributable to goodwill. On January 1, 2020, S held merchandise sold to it from P for $60,000. The beginning inventory had an applicable gross profit of 20%. During 2020 P sold merchandise to S for $120,000. On December 31, 2020, S held $30,000 of the merchandise in its inventory. The ending inventory had an applicable gross profit of 25%. S wrote down to $28,000 the merchandise purchased from P and remaining in its 2020 ending inventory. At December 31, 2020, Sowed P $20,000 as a result of the intercompany sale. On January 1, 2020, P held merchandise sold to it from S for $40,000. The beginning inventory had an applicable gross profit of 30%. During 2020 S sold merchandise to P for $100,000. On December 31, 2020, P held $20,000 of the merchandise in its inventory. The ending inventory had an applicable gross profit of 30%. On January 1, 2019, P purchased a piece of equipment with a cost of $100,000 and accumulated depreciation of $20,000 from S for $50,000. The equipment had an estimated 10-year life on January 1, 2019 and is being depreciated by the straight-line basis with no salvage value. The trial balances of P and S as of December 31, 2020 follow: S $60,000 60,000 80,000 Cash Accounts Receivable Inventory Investment is s Land Buildings Accumulated Depreciation-Buildings Equipment Accumulated Depreciation Equipment Goodwill Accounts Payable Bonds Payable Common Stock Paid-in-capital in Excess of Par Retained Earnings, January 1, 2020 Sales Cost of Goods Sold Other Expense Dividend Income Dividends Declared Totals P $96,000 140,000 140,000 400,000 100,000 800,000 (280,000) 100,000 (50,000) 30,000 (200,000) 100,000 150,000 (50,000) 220,000 (80,000) 30,000 (140,000) (200,000) (80,000) (20,000) (100,000) (300,000) 200,000 50,000 (100,000) (500,000) (500,000) (800,000) 400,000 200,000 (16,000) 40,000 0 20.000 $ 0 $ INSTRUCTIONS: (1) Prepare a Value Analysis Schedule (2) Prepare a D&D Schedule. (3) Prepare elimination entries required on December 31, 2020 in general journal format. (4) Prepare the income determination schedules. (5) Prepare a consolidated worksheet for P and its subsidiary S as of December 31, 2020