Answered step by step

Verified Expert Solution

Question

1 Approved Answer

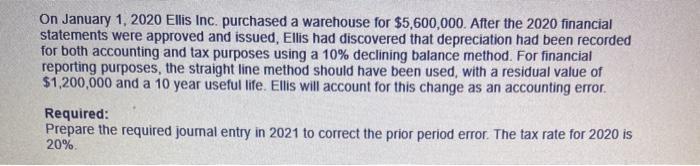

On January 1, 2020 Ellis Inc. purchased a warehouse for $5,600,000. After the 2020 financial statements were approved and issued, Ellis had discovered that depreciation

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Only Tax Audit Guide Youll Ever Need

Authors: Janet M. Sydlaske, Richard K. Millcroft

1st Edition

0471510769, 978-0471510765