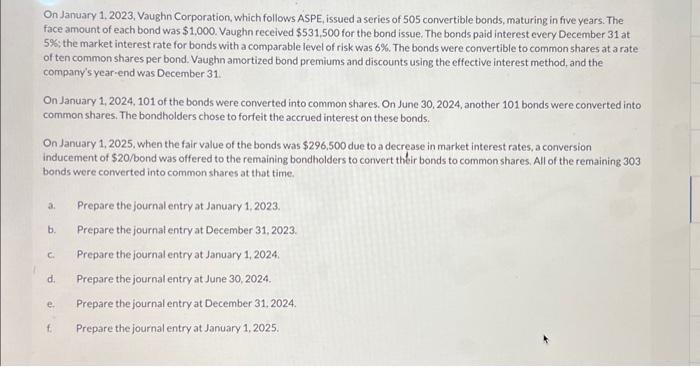

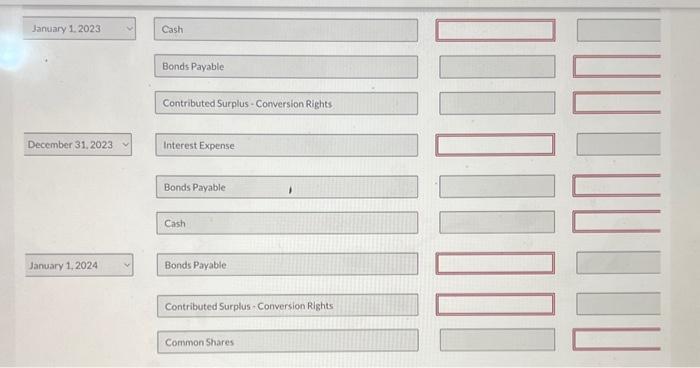

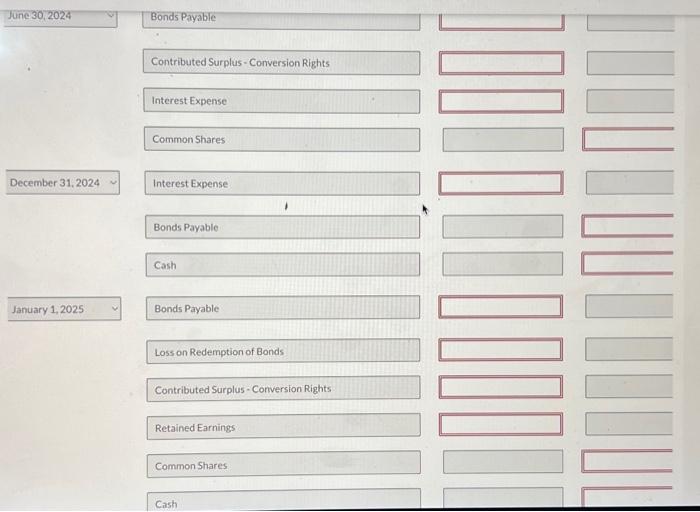

On January 1, 2023, Vaughn Corporation, which follows ASPE, issued a series of 505 convertible bonds, maturing in five years. The face amount of each bond was $1,000. Vaughn received $531,500 for the bond issue. The bonds paid interest every December 31 at. 5%; the market interest rate for bonds with a comparable level of risk was 6%. The bonds were convertible to common shares at a rate of ten common shares per bond. Vaughn amortized bond premiums and discounts using the effective interest method, and the company's year-end was December 31 . On January 1, 2024, 101 of the bonds were converted into common shares. On June 30, 2024, another 101 bonds were converted into common shares. The bondholders chose to forfeit the accrued interest on these bonds. On January 1, 2025, when the fair value of the bonds was $296,500 due to a decrease in market interest rates, a conversion inducement of $20 /bond was offered to the remaining bondholders to convert their bonds to common shares. All of the remaining 303 bonds were converted into common shares at that time. a. Prepare the journal entry at January 1, 2023. b. Prepare the journal entry at December 31,2023. c. Prepare the journal entry at January 1, 2024. d. Prepare the journal entry at June 30, 2024 . e. Prepare the journal entry at December 31,2024. f. Prepare the journal entry at January 1, 2025. January 1.2023 Cash Bonds Payable Contributed Surplus - Conversion Rights December 31, 2023 Interest Expense Bonds Payable Cash \begin{tabular}{|l|l|l} \hline January 1, 2024 & Bonds Payable \end{tabular} Contributed Surplus - Conversion Rights Common Shares Contributed Surplus - Conversion Rights Interest Expense Common Shares Interest Expense Bonds Payable Cash January 1, 2025 Loss on Redemption of Bonds Contributed Surplus - Conversion Rights Retained Earnings Common Shares Cash On January 1, 2023, Vaughn Corporation, which follows ASPE, issued a series of 505 convertible bonds, maturing in five years. The face amount of each bond was $1,000. Vaughn received $531,500 for the bond issue. The bonds paid interest every December 31 at. 5%; the market interest rate for bonds with a comparable level of risk was 6%. The bonds were convertible to common shares at a rate of ten common shares per bond. Vaughn amortized bond premiums and discounts using the effective interest method, and the company's year-end was December 31 . On January 1, 2024, 101 of the bonds were converted into common shares. On June 30, 2024, another 101 bonds were converted into common shares. The bondholders chose to forfeit the accrued interest on these bonds. On January 1, 2025, when the fair value of the bonds was $296,500 due to a decrease in market interest rates, a conversion inducement of $20 /bond was offered to the remaining bondholders to convert their bonds to common shares. All of the remaining 303 bonds were converted into common shares at that time. a. Prepare the journal entry at January 1, 2023. b. Prepare the journal entry at December 31,2023. c. Prepare the journal entry at January 1, 2024. d. Prepare the journal entry at June 30, 2024 . e. Prepare the journal entry at December 31,2024. f. Prepare the journal entry at January 1, 2025. January 1.2023 Cash Bonds Payable Contributed Surplus - Conversion Rights December 31, 2023 Interest Expense Bonds Payable Cash \begin{tabular}{|l|l|l} \hline January 1, 2024 & Bonds Payable \end{tabular} Contributed Surplus - Conversion Rights Common Shares Contributed Surplus - Conversion Rights Interest Expense Common Shares Interest Expense Bonds Payable Cash January 1, 2025 Loss on Redemption of Bonds Contributed Surplus - Conversion Rights Retained Earnings Common Shares Cash