Answered step by step

Verified Expert Solution

Question

1 Approved Answer

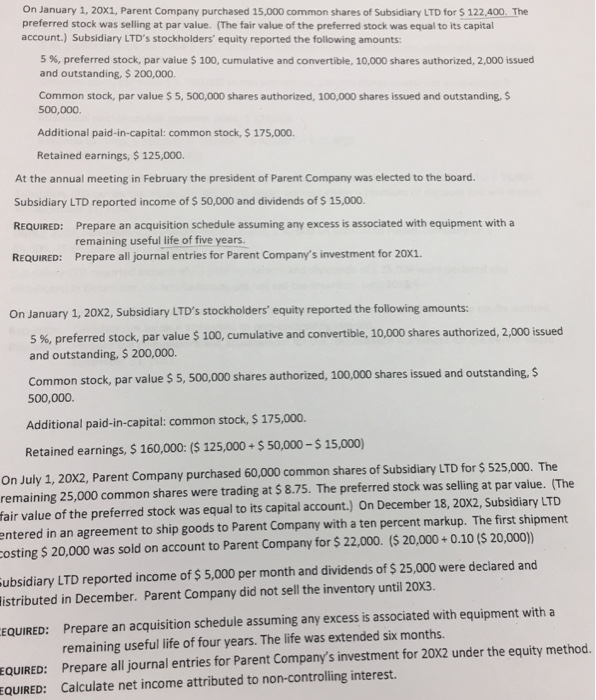

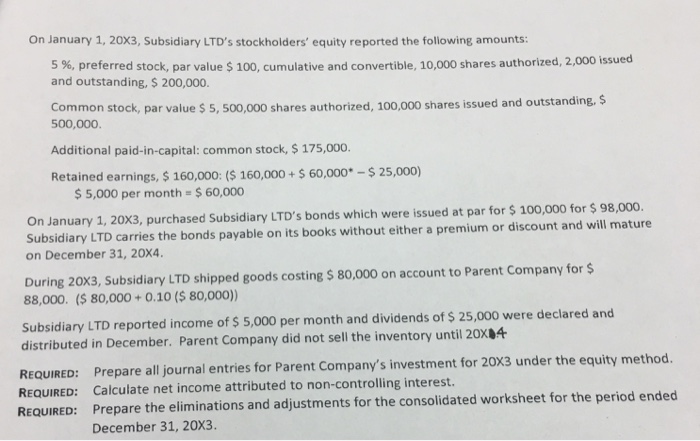

On January 1, 20x1, Parent Company purchased 15.000 common shares of subsidiary LT preferred stock was selling at par value. The fair value of the

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

A Blueprint For Lean Audit Lead Your Company To Higher Performance Levels

Authors: Maurice Washpun

1st Edition

B09R3DSLFF, 979-8408643707