Answered step by step

Verified Expert Solution

Question

1 Approved Answer

On January 1, Pulse Recording Studio (PRS) had the following account balances. Accounts Payable $ 8,400 Accounts Receivable 6,600 Accumulated DepreciationEquipment 6,600 Cash 3,640 Cash

On January 1, Pulse Recording Studio (PRS) had the following account balances.

| Accounts Payable | $ | 8,400 |

| Accounts Receivable | 6,600 | |

| Accumulated DepreciationEquipment | 6,600 | |

| Cash | 3,640 | |

| Cash Equivalents | 1,620 | |

| Common Stock | 10,400 | |

| Deferred Revenue | 3,900 | |

| Equipment | 30,900 | |

| Notes Payable (long-term) | 12,300 | |

| Prepaid Rent | 2,610 | |

| Retained Earnings | 4,250 | |

| Supplies | 480 | |

The following transactions occurred during January.

- Received $2,440 cash on 1/1 from customers on account for recording services completed in December.

- Wrote checks on 1/2 totaling $4,370 for amounts owed on account at the end of December.

- Purchased and received supplies on account on 1/3, at a total cost of $200.

- Completed $3,900 of recording sessions on 1/4 that customers had paid for in advance in December.

- Received $4,690 cash on 1/5 from customers for recording sessions started and completed in January.

- Wrote a check on 1/6 for $4,080 for an amount owed on account.

- Converted $1,020 of cash equivalents into cash on 1/7.

- On 1/15, completed EFTs for $1,380 for employees salaries and wages for the first half of January.

- Received $2,970 cash on 1/31 from customers for recording sessions to start in February.

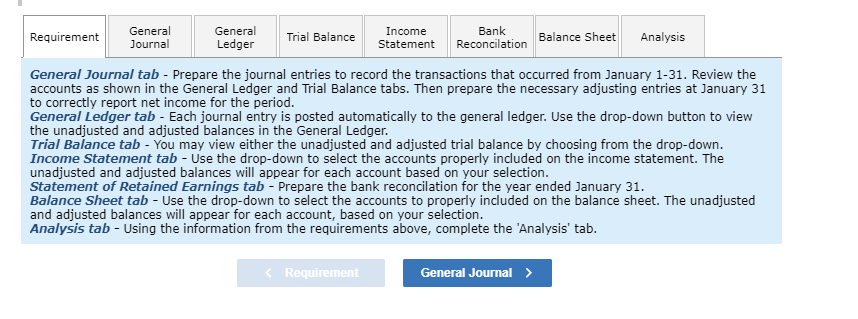

Required:

- Prepare journal entries for the January transactions. Review the 'General Ledger' and the unadjusted 'Trial Balance' Tabs to see the effect of the transactions on the account balances.

- Prepare journal entries for items (j)(n) from the bank reconciliation. j. The bank deducted $470 for an NSF check from a customer deposited on January 5. k. The check written January 6 has not cleared the bank, but the January 2 payment has cleared. l. The cash received and deposited on January 31 was not processed by the bank until February 1. m. The bank added $4 cash to the account for interest earned in January. n. The bank deducted $4 for service charges.

- Prepare adjusting journal entries on 1/31 in 'General Journal' Tab. (these are shown as items 15-21). o. Depreciation for the month is $240. p. Salaries and wages totaling $1,100 have not yet been recorded for January 1631. q. Prepaid Rent will be fully used up by March 31. r. Supplies on hand at January 31 were $200. s. Received $200 invoice for January electricity charged on account to be paid in February but is not yet recorded. t. Interest on the promissory note of $32 for January has not yet been recorded or paid. u. Income tax of $2,300 on January income has not yet been recorded or paid.

- Review the adjusted 'Trial Balance' as of January 31.

- Prepare an income statement for the period ended January 31 in the 'Income Statement' Tab.

- Prepare a bank reconciliation in the 'Bank Reconciliation' Tab.

- Prepare a classified balance sheet as of January 31 in the 'Balance Sheet' Tab.

- Using the information from the requirements above, complete the 'Analysis' tab.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fia Foundations Of Financial Accounting Ffa Interactive Text

Authors: BPP Learning Media

1st Edition

1509724176, 978-1509724178