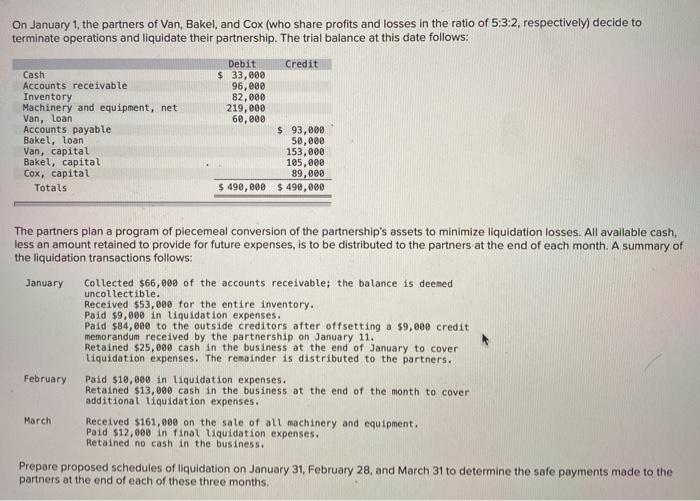

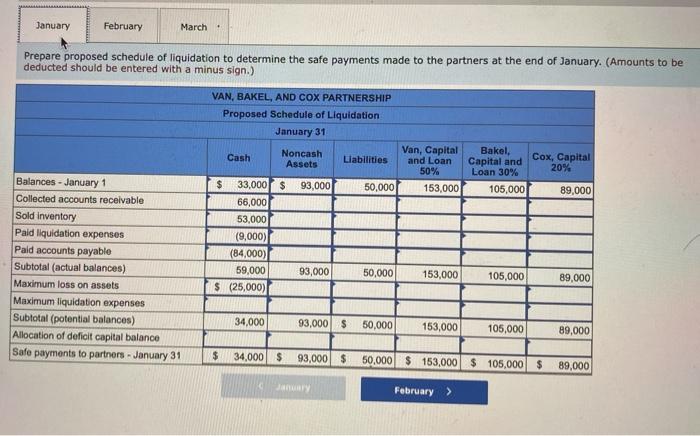

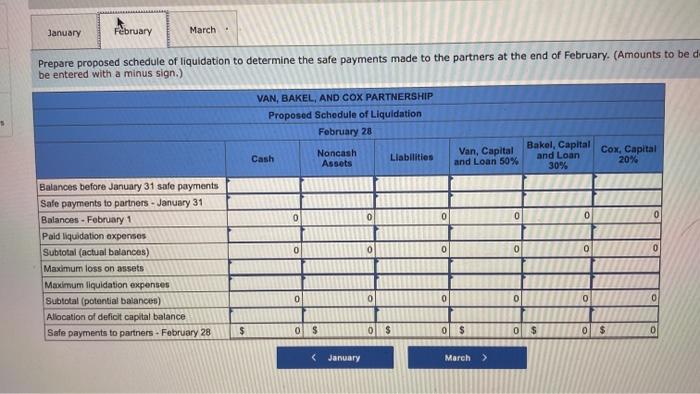

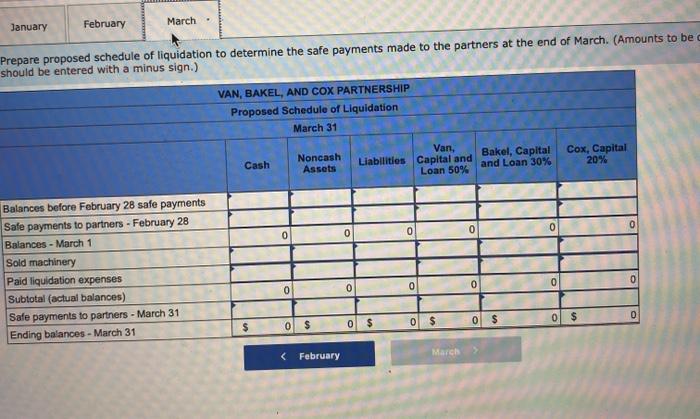

On January 1, the partners of Van, Bakel, and Cox (who share profits and losses in the ratio of 5:3:2, respectively) decide to terminate operations and liquidate their partnership. The trial balance at this date follows: Cash Accounts receivable Inventory Machinery and equipment, net Van, loan Accounts payable Bakel, loan Van, capital Bakel, capital Cox, capital Totals Debit Credit $ 33,000 96,000 82,000 219,000 60,000 $ 93,000 50,000 153,000 105,000 89,000 $ 490,000 $ 490,000 The partners plan a program of plecemeal conversio the partnership's assets to minimize liquidation losses. All available cash, less an amount retained to provide for future expenses, is to be distributed to the partners at the end of each month. A summary of the liquidation transactions follows: January Collected $66,000 of the accounts receivable; the balance is deemed uncollectible. Received $53,000 for the entire inventory. Paid $9,000 in Liquidation expenses. Paid $84,000 to the outside creditors after offsetting a $9,000 credit memorandum received by the partnership on January 11. Retained $25,000 cash in the business at the end of January to cover liquidation expenses. The remainder is distributed to the partners. February Paid $10,000 in liquidation expenses. Retained $13,000 cash in the business at the end of the month to cover additional liquidation expenses. March Received $161,000 on the sale of all machinery and equipment. Paid $12,000 in final liquidation expenses. Retained no cash in the business. Prepare proposed schedules of liquidation on January 31, February 28, and March 31 to determine the safe payments made to the partners at the end of each of these three months. January February March Prepare proposed schedule of liquidation to determine the safe payments made to the partners at the end of January. (Amounts to be deducted should be entered with a minus sign.) VAN, BAKEL, AND COX PARTNERSHIP Proposed Schedule of Liquidation January 31 Cash Noncash Assets Llabilities Van, Capital and Loan 50% 153,000 Bakel, Capital and Loan 30% 105,000 Cox, Capital 20% 93,000 50,000 89,000 Balances - January 1 Collected accounts receivable Sold inventory Paid liquidation expenses Pald accounts payable Subtotal (actual balances) Maximum loss on assets Maximum liquidation expenses Subtotal (potential balances) Allocation of deficit capital balance Safe payments to partners - January 31 $ 33,000 $ 66,000 53,000 (9,000) (84,000) 59,000 $ (25,000) 93,000 50,000 153,000 105,000 89,000 34,000 93,000 $ 50,000 153,000 105,000 89,000 $ 34,000 $ 93,000 $ 50,000 $ 153,000 $ 105,000 $ 89,000 February > January February March Prepare proposed schedule of liquidation to determine the safe payments made to the partners at the end of February. (Amounts to be de be entered with a minus sign.) VAN, BAKEL, AND COX PARTNERSHIP Proposed Schedule of Liquidation February 28 Cash Noncash Assets Liabilities Van, Capital and Loan 50% Bakel, Capital and Loan 30% Cox, Capital 20% 0 0 0 0 0 0 0 0 0 0 0 Balances before January 31 safe payments Safe payments to partners - January 31 Balances - February 1 Pald liquidation expenses Subtotal (actual balances) Maximum loss on assets Maximum liquidation expenses Subtotal (potential balances) Allocation of deficit capital balance Safe payments to partners - February 28 0 0 0 $ 0 S 0 $ 0 $ 0 $ 0 $ 0 January February March Prepare proposed schedule of liquidation to determine the safe payments made to the partners at the end of March. (Amounts to be should be entered with a minus sign.) VAN, BAKEL, AND COX PARTNERSHIP Proposed Schedule of Liquidation March 31 Noncash Assets Van, Liabilities Capital and Loan 50% Bakel, Capital and Loan 30% Cash Cox, Capital 20% 0 0 0 Balances before February 28 safe payments Safe payments to partners - February 28 Balances - March 1 Sold machinery Paid liquidation expenses Subtotal (actual balances) Safe payments to partners - March 31 Ending balances - March 31 0 0 0 0 0 0 0 0 $ 0 $ 0 $ $ 0 $ 0 $