Answered step by step

Verified Expert Solution

Question

1 Approved Answer

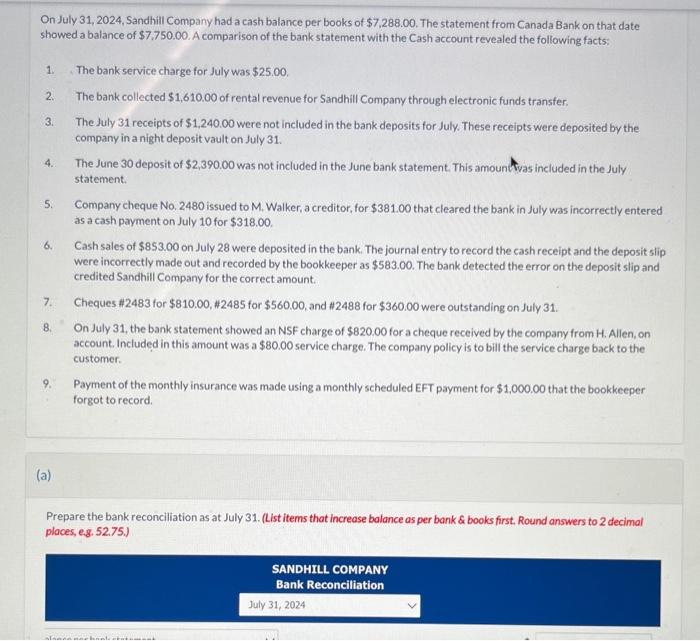

On July 31, 2024, Sandhill Company had a cash balance per books of $7,288.00. The statement from Canada Bank on that date showed a balance

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial And Managerial Accounting

Authors: Robert Meigs Jan Williams, Sue Haka, Mark S Bettner

16th Edition

0077557344, 978-0077557348