Answered step by step

Verified Expert Solution

Question

1 Approved Answer

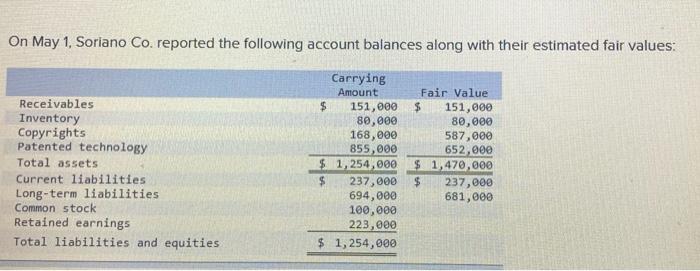

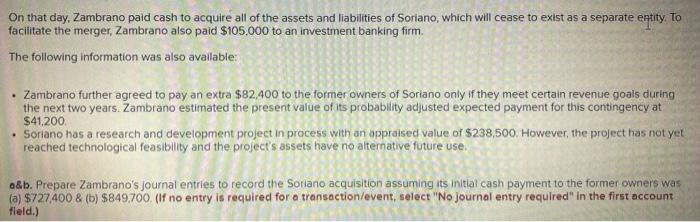

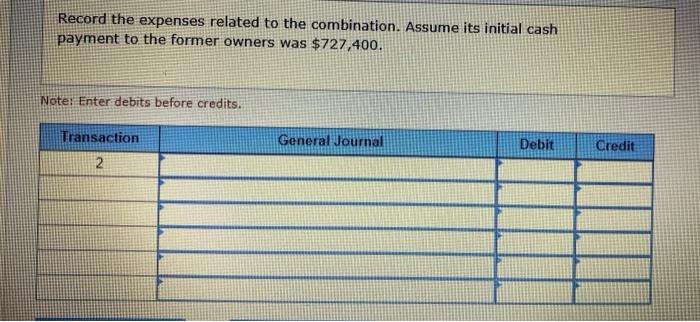

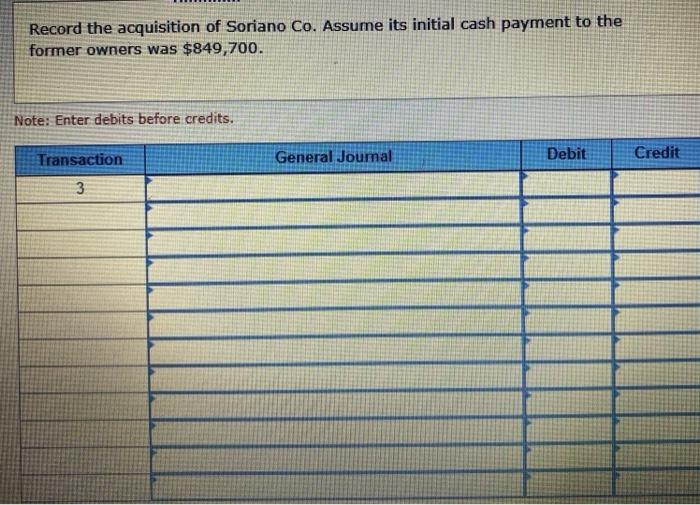

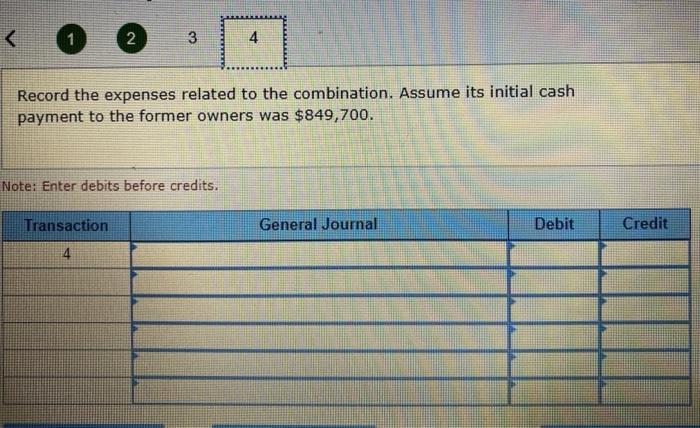

On May 1, Soriano Co. reported the following account balances along with their estimated fair values: Receivables Inventory Copyrights Patented technology Total assets Current liabilities

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managements Reluctance In Implementing Audit Recommendations

Authors: Tariro Chinamasa

1st Edition

6139980240, 978-6139980246