Answered step by step

Verified Expert Solution

Question

1 Approved Answer

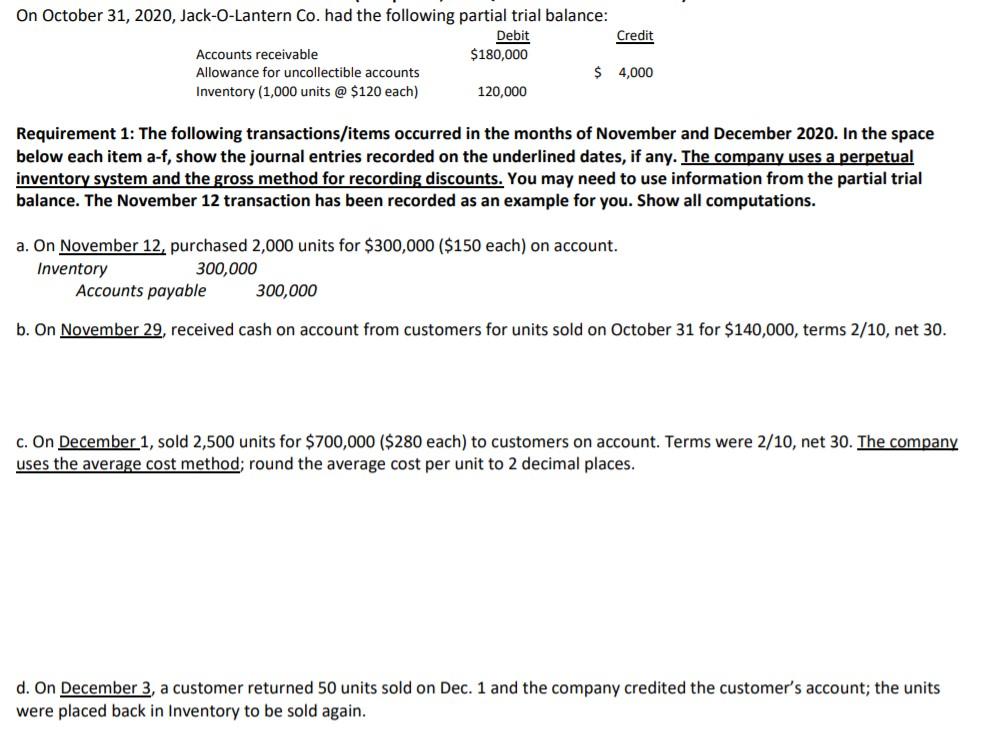

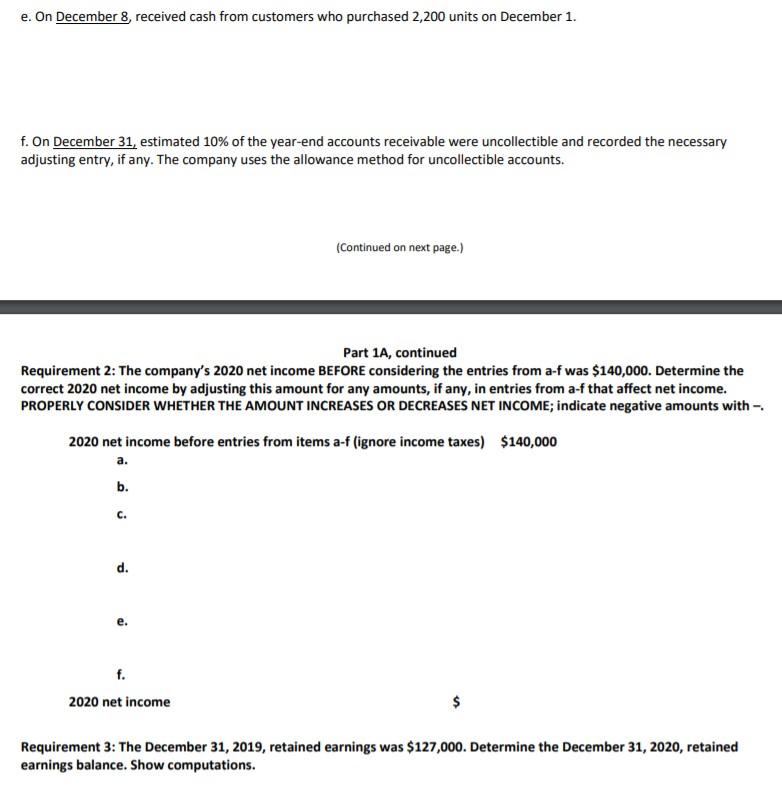

On October 31, 2020, Jack-O-Lantern Co. had the following partial trial balance: Debit Credit Accounts receivable $180,000 Allowance for uncollectible accounts $ 4,000 Inventory (1,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modern Auditing Study Guide

Authors: Walter G. Kell

4th Edition

0471619434, 978-0471619437