On the income statement attached, which lines are considered operating vs non operating, and why?

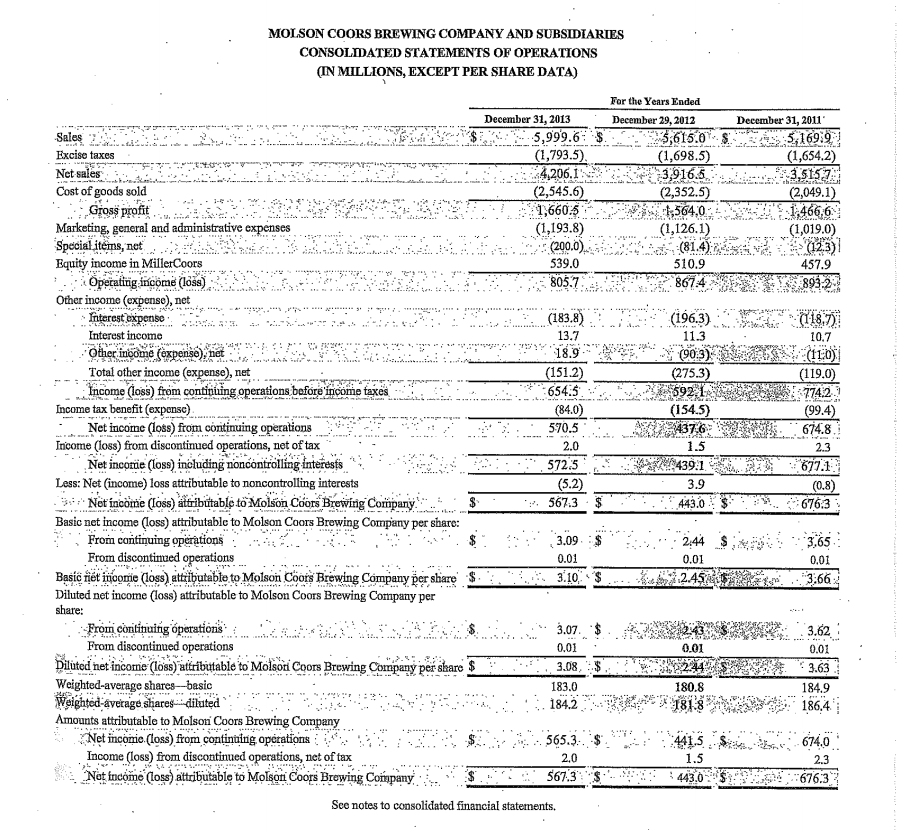

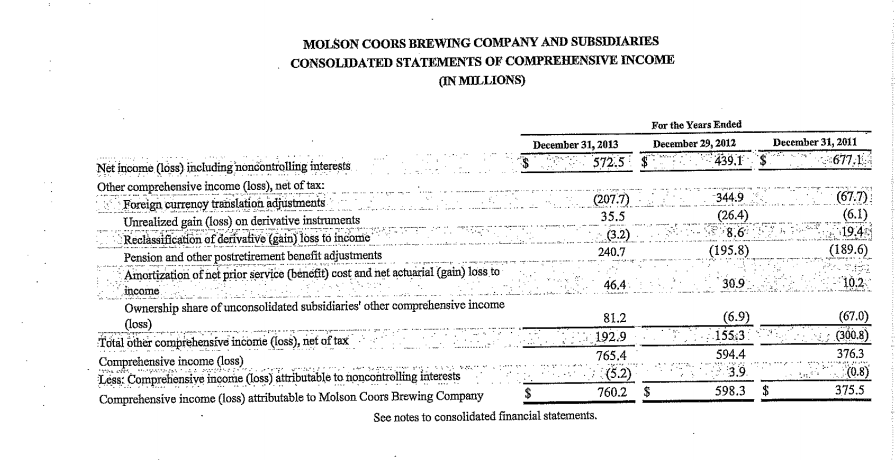

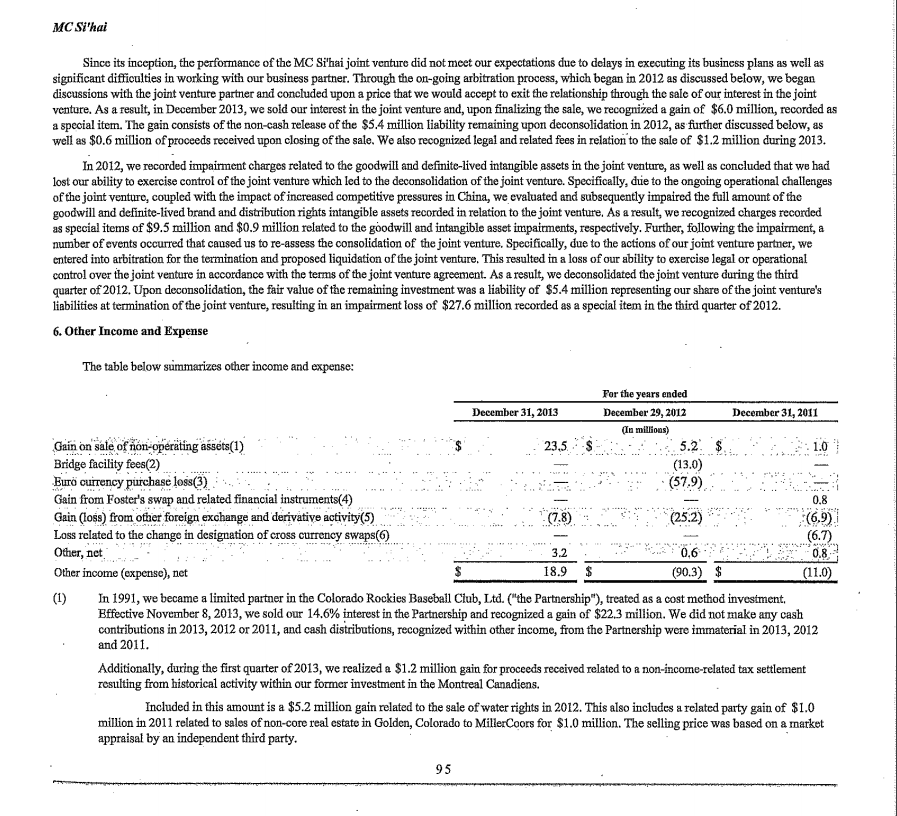

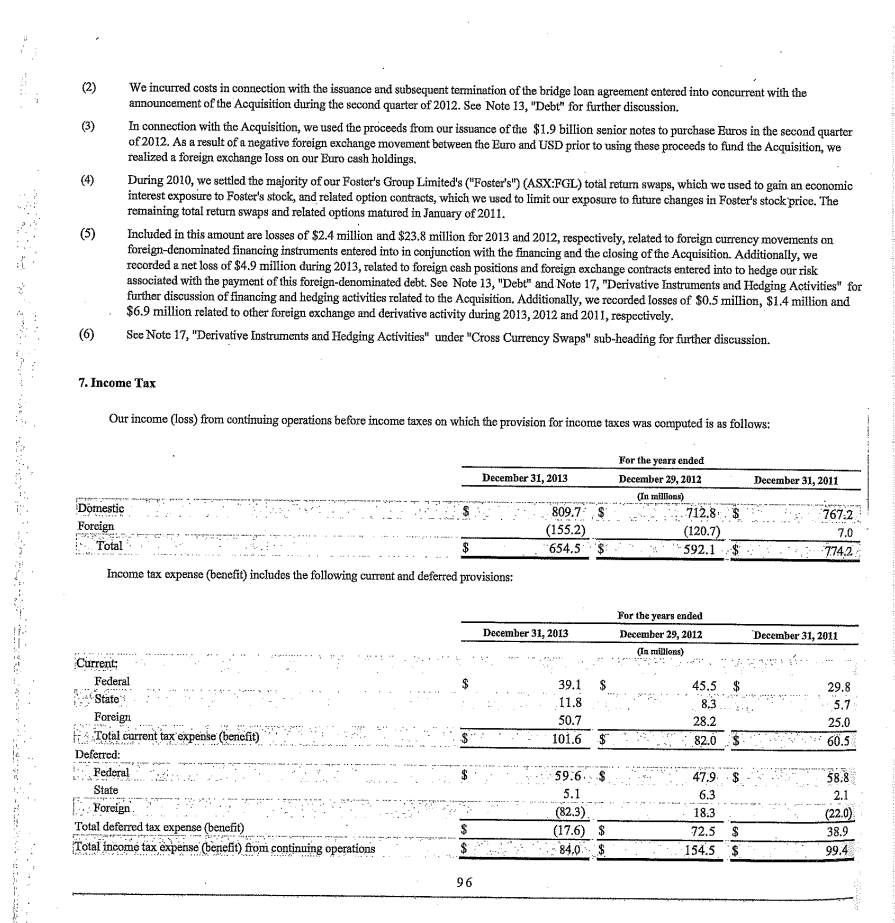

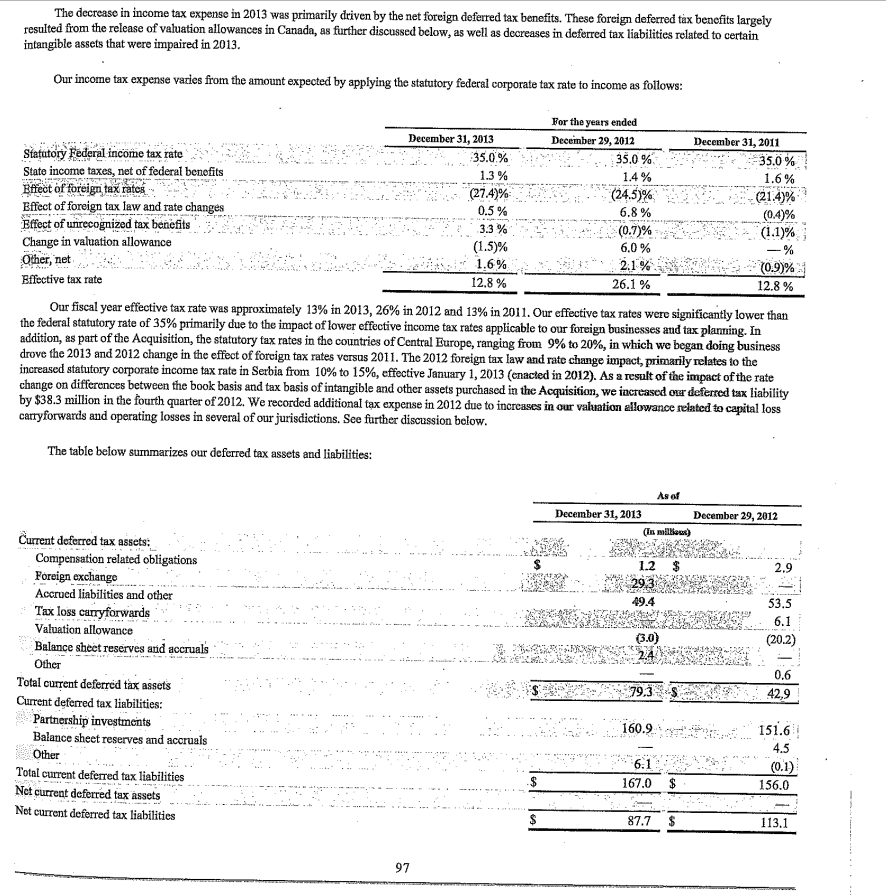

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF OPERATIONS (IN MILLIONS, EXCEPT PER SHARE DATA) For the Years Ended December 31,2013 December 29,2012 December 31,2011 (1,698.5) (2,352.5) (1,126.1) 510.9 Excise taxes (1,793.5) (1,654,2) Cost of goods sold (2,545.6 Gross profit. general and a Equity income in MillerCoors 539.0 457.9 Opecating income (loss)".. 8057803 " :.. #x ,.r : Other income(expense),net."? Interest income 10.7 Total other income (expense), net 151.2 (275.3 774:2.1 9.4 Income tax benefit (expense) (154.5) Net income (loss) from continuing operations *. '.. 570.5 Income (loss) from discontinued operations, net of tax 2.3 Net income (ioss) including noncontrolling iteres* 439:67 572.5 Less: Net (income) loss attributable to noncontrolling interests .;r'. N t in tie@ s) it ibit blet Mole . CionB i ingCoin a yin......-. S Basic net income (loss) attributable to Molson Coors Brewing Company per share: (0.8 : 6763 ' 443.0 $ . From ds 0.01 Basig riet inoomie loss attibutable to Molson Coors Browing Company per share Diluted net income (loss) attributable to Molson Coors Brewing Company per From continuing operations From discontinued operations haa 3.07 . .$ .Aeea 0.01 mgr.. 3.62 : ... u . .. 0.01 ple nt ncome (tble to Moloai Cooms Browi Weighted-average shares-basic re S 3.63 180.8 184.9 Amounts attributable to Molson Coors Brewing Company Net incoie (loss) fromm coptinuing, operations .. Income (loss) from discontinmed operations, net of tax Nat incoime Coss) attibutable to Molsgn Coors Browing Conpany. r. ..i.'K 565 2.3 See notes to consolidated financial statements. MOLSON COORS BREWING COMPANY AND SUBSIDIARIES CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (IN MILLIONS) For the Years Ended December 31, 2013 December 29, 2012 December 31, 2011 572.5 $ 439.1 $677,1 Net income (loss) including noncontrolling interests Other comprehensive income (loss),netoftax: 01764) 344.9 -..-- (67.7 Foreigcurrenoy translation adjustments Unrealized gain (loss) on derivative instruments 35.5 28.6194 loss to and other postretirement benefit adjustments 240.7 -- (189.6). Amortization of net prior service (benefit) cost and net actuarial (gain) loss to " 46.4 10.2 Ownership share of (loss) (67.0) (300.8) 376.3 (0.8 375.5 155:3 " Total other comprehensive income (loss), net of tax -. 192.9 765.4 760.2 $ 598.3 $ Comprehensive income (loss) attributable to Molson Coors Brewing Company See notes to consolidated financial statements. CONSOLIDATED FINANCIAL STATEMENTS (EXCERPTS) 1. Basis of Presentation and Summary of Significant Accounting Policies Revenue Recognition Our net sales represent the sale of beer and other malt beverages (including adjacencies, such as cider) net of excise taxes, the vast majority of which are brands that we own and brew ourselves. We import or brew and sell certain non-owned partner brands under licensing and related arrangements. In addition, we contract manufacture for other brewers in some of our markets. Revenue is recognized when the significant risks and rewards of ownership, including the risk of loss, are transferred to the customer or distributor depending upon the method of distribution and shipping terms. The cost of various programs, such as price promotions, rebates and coupon programs are treated as a reduction of sales. In certain of our markets, slotting or listing fees are paid to customers and are also treated as a reduction of sales. Sales of products are for cash or otherwise agreed upon credit terms. Sales are stated net of incentives, discounts and retuns. We do not have standard terms that permit return of product; however, in certain markets where returns occur we estimate the amount of returns based on historical return experience and adjust our revenue accordingly. Products that do not meet our high quality standards are returned by the customer or recalled and destroyed and are recorded as a reduction of revenue. The reversal of revenue is recorded upon determination that the product will be recalled and destroyed. We estimate the costs required to facilitate product retums and record them in cost of goods sold as required. In addition to supplying our own brands, the U.K. business (within our Europe segment) sells other beverage companies' products to on-premise customers to provide them with a full range of products for their retail outlets. We refer to this as the "factored brand business." Sales from this business are included in our net sales and cost of goods sold when ultimately sold, but the related volume is not included in our reported sales volumes. In the factored brand business, we normally purchase inventory, which includes excise taxes charged by the vendor, take orders from customers for such brands, and invoice customers for the product and related costs of delivery. In accordance with guidance pertaining to reporting revenue gross as a principal versus net as an agent, sales under the factored brands are reported on a gross income basis. Payments made to customers are conditional on the achievement of volume targets, marketing commitments, or both. If paid in advance, we record such payments as prepayments and amortize them in the consolidated statements of operations over the relevant period to which the customer commitment is made (up to five years). Where there is no sufficiently separate identifiable benefit, and the payment is linked to volumes, or fair value cannot be established, the amortization of the prepayment or the cost as incurred is included in sales discounts as a reduction to sales and where there are specific marketing activities/commitments the cost is included as marketing, gencral and administrative expenses. The amounts capitalized are reassessed regularly for recoverability over the contract period and are impaired where there is objective evidence that the benefits will not be realized or the asset is otherwise not recoverable. In the U.K., loans are extended to a portion of the retail outlets that sell our brands. We reclassify a portion of beer revenue to interest income to reflect a market rate of interest on these loans. In fiscal years 2013, 2012 and 2011, these amounts were $4.9 million, S5.7 million, and $6.3 million, respectively, included in the Europe segment. Excise Taxes Excise taxes collected from customers and remitted to tax authorities are government-imposed excise taxes on beer shipments. Excise taxes on beer shipments aro shown in a separate line item in the consolidated statements of opcrations as a reduction of sales. Sales taxes collected from customers are recognized as a liability, with the liability subsequently reduced when the taxes are remitted to the tax authority Cost of Goods Sold Our cost of goods sold includes costs we incur to make and ship beer. These costs include brewing materials, such as barley, hops and various grains. Packaging materials, including glass bottiles, aluminum and steel cans, cardboard and paperboard are also included in our cost of goods sold. Additionally our cost of goods sold include both direct and indirect labor, shipping and handling including freight costs, utilities, maintenance costs, depreciation, promotional packaging, other manufacturing overheads and costs to purchase factored brands from suppliers, as well as the estimated cost to facilitate product returns. Marketing, General and Administrative Expenses Our marketing, general and administrative expenses include media advertising (television, radio, print), tactical advertising (signs, banners, point-of sale materials) and promotion costs on both local and national levels within our operating segments. The creative portion of our advertising activitics is expensed as incurred. Production costs of advertising and promotional materials are expensed when the advertising is first run. Advertising expense was $458.5 million, $423.5 million and $398.8 million for fiscal years 2013, 2012 and 2011, respectively. Prepaid advertising costs of $13.8 million and $23.9 million, were included in current assets in the consolidated balance sheets at December 31, 2013, and December 29, 2012, respectively This classification includes general and administrative costs for fiunctions such as finance, legal, human resources and information technology, which I costs are expensed when incutred. These costs also include our marketing and sales organizations, including labor and other consist primarily of labor and outside services, as well as bad debt expense related to our allowance for doubtful accounts. Unless capitalization is allowed or overheads. This line item additionally includes amortization costs associated with intangible assets, as well as certain deprociation costs related to non- production equipment and share-based d over the vesting period of the awards. Certain share-based contain provisions that accelerate vesting of awards upon change in control, retirement, disability or death of eligible employees and directors, Our share-b awards are considered vested when the employee's retention of the award is no longer contingent on providing service, which for certain awards can for awards granted to retirement-eligible individuals or accelerated recognition for awards granted to individuals that will become retirement eligible within the stated vesting period. Also, if less than the stated vesting period, we recognize these costs over the period from the grant date to the date retirement eligibility reducing net operating cash flows and increasing net financing cash flows. is achieved. We report the bencfits of tax deductions in excess of recognized compensation cost as a financing cash flow, thereby Special Items Our special items represent charges incurred or benefits realized that we do not believe to be indicative of our core operations; specifically, such items are considered to be one of the following: infrequent or unusual items, impairment or asset abandonment-related losses, .restructuring charges and other atypical employeo-related costs, or fees on termination of significant operating agreements and gains (losses) on disposal of investments. Although we believe these itens are not indicative of our core operations, the items classified as special items are not necessarily non-recurring. Equity Income in MillerCoors MillerCoors accounted for Our equity income in MillerCoors represents our proportionate share for the period of the net income of our i under the equity method. Such amount typically reflects adjustments to eliminate intercompany gains and losses, and to difference between cost and underlying equity in net assets upon the formation of MillerCoors. Interest Expense, net interest costs are associated with borrowings to finance our operations. In addition to interest eamed on our cash and cash equivalents across our interest income in the Europe segment is associated with trade loans receivable from customers, primarily in the U.K. As noted above, this includes a portion of beer revenue which is reclassified to interest income to reflect a market rate of interest on these loans. We capitalize interest cost as a part of the certain fixed assots if the cost of the capital expenditure and the expected time to complete the project are considered significant. Other Income (Expense) Our other income (expense) classification primari ly includes gains and losses associated with activities not directly related to brewing and selling beer. For instance, certain gains or losses on foreign exchange and on sales of non-operating assets are classificd in this line item. Income Taxes Deferred income taxes are provided for the temporary differences betwcen the financial reporting basis and the tax basis of our assets, liabilities, and and losses recorded in accumulated other comprehensive income (loss). We provide for taxes that may be payable if undistributed earnings of overseas s gs of overseas subsidiaries were to be remitted to the U.S, except for those earnings that we consider to be permanently reinvested. Interest, penalties offsetting positions related to unrecognized tax benefits are recognized as a component of income tax expense. primarily the rosult of uncertainties regarding the future realization of recorded tax benefits o tax loss carryforwards from our consolidated balance sheet Our deferred tax valuation allowances are includes our investment in Tradeteam of $17.7 million. During the fiscal years ended 2013, 2012 and 2011, we recognized equity carnings from our Tradeteam investment of $4.6 million, S6.0 million and $6.4 million, respectively, which are recorded within cost of goods sold MC SY'hai Since its inception, the performance of the MC Si hajoint venture did not meet our expectations due to delays in executing its business plans as well as significant difficulties in working with our business partner. Through the on-going arbitration process, which began in 2012 as discussed below, we began discussions with the joint venture partner and concluded upon a price that we would accept to exit the relationship through the sale of our interest in the joint venture. As a result, in December 2013, we sold our interest in the joint venture and, upon finalizing the sale, we recognized a gain of $6.0 million, recorded as a special item. The gain consists of the non-cash release of the S5.4 million liability remaining upon deconsolidation in 2012, as further discussed below, as well as $0.6 million of proceeds received upon closing of the sale. We also recognized legal and related fees in relation to the sale of $1.2 million during 2013 In 2012, we recorded impairment charges related to the goodwill and defnite-lived intangible assets in the joint venture, as well as concluded that we had lost our ability to exercise control of the joint venture which led to the deconsolidation of the joint venture. Specifically, due to the ongoing operational challenges of the joint venture, coupled with the impact of increased competitive pressures in China, we evaluated and subsequently impaired the full amount of the goodwill and definite-lived brand and distribution rights intangible assets recorded in relation to the joint venture. As a result, we recognized charges recorded as special items of $9.5 million and $0.9 million related to the goodwill and intangible asset impairments, respectively. Further, following the impairment, a number of events occurred that caused us to re-assess the consolidation of the joint venture. Specifically, due to the actions of our joint venture partner, we entered into arbitration for the termination and proposed liquidation of the joint venture. This resulted in a loss of our ability to exercise legal or operational control over the joint venture in accordance with the terms of the joint venture agreement. As a result, we deconsolidated thejoint venture during the third quarter of 2012. Upon deconsolidation, the fair value of the remaining investment was a liability of $5.4 million representing our share of the joint venture's liabilities at termination of the joint venture, resulting in an impairment loss of $27.6 million recorded as a special item in the third quarter of 2012 6. Other Income and Expense The table below summarizes other income and For the years ended December 29, 2012 (Tn millioas) December 31, 2013 December 31,2011 Gain on sale of non-operting assets(C) Bridge facility fees(2) Euro ourrency purchase loss(3) Gain from Foster's swap Gain (loss) from other foreign exchange and derivative activity(.) Loss related to the change in designation of cross currency swaps(o) Other, net Other income (expense), net 23,5 -S : (57.9) and related financial instruments(4) 7.8) 25.2).6.9). 0.60.8 18.9 $ (90.3) $ (I) In 1991, we became a limited partner in the Colorado Rockies Baseball Club, Ltd. ("the Partnership"), treated as a cost method investment. Effective November 8, 2013, we sold our 14.6% interest in the Partnership and recognized a gain of $22.3 million, we did not make any cash contributions in 2013, 2012 or 2011, and cash distributions, recognized within other income, from the Partnership were immaterial in 2013, 2012 and 2011. Additionally, during the first quarter of 2013, we realized a $1.2 million gain for proceeds received related to a non-income-related tax settlement resulting from historical activity within our former investment in the Montreal Canadiens. Included in this amount is a $5.2 million gain related to the sale of water rights in 2012. This also includes a related party gain of S1.0 million in 2011 related to sales of non-core real estate in Golden, Colorado to MillerCoors for $1.0 million. The selling price was based on a market appraisal by an independent third party. (2)We incurred costs in connection with the issuance and subsequent termination of the bridge loan agreement entered into concurrent with the (3 In connection with the Acquisition, we used the proceeds from our issuance of the $1.9 billion senior notes to purchase Buros in the second quarter (4)During 2010, we settled the majority of our Foster's Group Limited's ("Foster's"n (ASX:FGL) total return swaps, which wo used to gain an economic (5) Included in this amount are losses of $2.4 million and $23.8 million for 2013 and 2012, respectively, related to foreign curreney movements on announcement of the Acquisition during the second quarter of 2012. See Note 13, "Debt" for further discussion. of 2012. As a result of a negative foreign exchange movement between the Euro and USD prior to using these proceeds to fund the Acquisition, we realized a foreign exchange loss on our Euro cash holdings. interest exposure to Foster's stock, and related option contracts, which we used to limit our exposure to future changes in Foster's stock price. The remaining total return swaps and related options matured in January of 2011 foreign-denominated financing instruments entered into in conjunction with the financing and the closing of the Acquisition. Additionally, we recorded a net loss of $4.9 million during 2013, related to foreign cash positions and foreign exchange contracts entered into to hedge our risk associated with the payment of this foreign-denominated debt. See Note 13, "Debt" and Note 17, "Derivative Instruments and Hedging Activities" for further discussion of financing and hedging activitics rclated to the Acquisition, Additionally, we recorded losses of $0.5 million, $1.4 million and $6.9 million related to other foreign exchange and derivative activity during 2013, 2012 and 2011, respectively (6) SeeNote 17, "Derivative Instruments and Hedging Activitics" under "Cross Currency Swaps" sub-heading for further discussion. 7. Income Tax Our income (loss) from continuing operations before income taxes on which the provision for income taxes was computed is as follows: For the years ended December 29, 2012 December 31,2013 Deeember 31, 2011 767.2 Foreign Total 654.5 $ 592.1 Income tax expense (benefit) includes the following current and deferred provisions: For the years ended December 29, 2012 Ia milions) December 31,2013 December 31,2011 Federal 5 h. Total current ta expense (benefit). .................. 101.6 $ Pederal - 479 * 9 58 Foreign.' Total deferred tax expense Total income tax expense (benefit) froi continuing operations 154.5 6 The decrease in income tax expense in 2013 was primarily driven by the net foreign deferred tax benefits. These forcign deferred tx benefits largely resulted from the release of valuation allowances in Canada, as further discussed below, as well as deareases in deferred tax liabilitics related to certain intangible assets that were impaired in 2013. Our income tax expense varies from the amount expected by applying the statutory federal corporate tax rate to income as follows For the years ended Deceimber 29,2012 December 31, 2013 December 31,2011 Siatutory federal income tax rate State income taxes, net of federal benofits Bfteot of foreign tax ratck Bffect of foreign tax law and rate changes 35.0% 1.4% 6.8 % 6.0 % 0.5 % 3.3 % Change in valuation allowance Other, net"^. Effective tax rate 1.6% 12.8 % 26.1 % 12.8 % Our fiscal year effective tax rate was approximately 13% in 2013, 26% n 2012 and 13% in 2011 Our effective tax rates were significantly lower than the federal statutory rate of 35% primarily due to the impact of lower e ective m ome tax rates applicable to our foreign businesses andt lammn in addition, as part of the Acquisition, the statutory tax rates in the countries of Central drove the 2013 and 2012 change in the effect of foreign tax rates versus 2011. The 2012 foreign tax law and rate change impact, increased statutory corporate income tax rate tn Serbia om 10% to 15% e ective January 1 2013 enacted in 2012 As a result of the impact of the rate change on differences between the book basis and tax basis of intangible and other assets p by $38.3 million in the fourth quarter of 2012. We recorded additional tax expense in 2012 due to increases in our carryforwards and operating losses in several of our jurisdictions. See further discussion below rope, ranging f om 9% to 20% in which we began doing business urchased in the Acquisition, we iacreased otr deferred tax liability The table below summarizes our deferred tax assets and liabilities: As af December 31, 2013 December 29, 2012 Current deferred tax assets: Compensation related obligations Foreign exchange Accrued liabilities and other Tax loss carryforwards Vauation allowance Balance sheet reserves and accruals 49.4 53.5 .0 (20.2) Total current deferred tax assets Current deferred tax liabilities: Partnership investments Balance sheet reserves and accruals Other 60.9151.6 Total current deferred tax liabilities Net current deferred tax assets Net current deferred tax liabilities 167.0 $ 156.0 87.7 $ 8. Special Items We have incurred charges or recognized gains that we do not believe to be indicative of our core operations. As such, we have separately classified these charges (benefits) as special items. The table below summarizes special items recorded by segment: For the years ended December 29, 2012 (In millions) December 31,2013 December 31,2011 Restructuringl) 10.6 S 0,6 14.5 19.8 Special termination benefits 5.2 Canada(2) 17.9 Canada Intangible asset impairment(3) Burope - Asset abandonment(4) Europe - Intangible asset impairment(5) MCIChina impairinient anld related costs( 150.9 2 Canada Flood loss (imsurancsemnn Canada - BRI loan guarantee adjustment(8) 0.2. (2.0) ied asset adjustimiente) Europe - Release of non-income-related tax reserve(10) rFlood loss (insurance reimbursement)(11) Europe- Costs associated with strategic initiatives (4.2) (2.0) Cost associated wi otsourcing and other strategio initiatives 13.2 -. Europe- Tradetcan transactions(12) MCI-Sale of China joint venture(6) Total Special items, net (I) During 2013, 2012 and 2011, we recognized expenses associated with restructuring programs related to severance and other employee related charges. 200.0 S See further discussion of restructuring activitics below pension plans in Canada. See Note 16, "Employce Retirement Plans and Postretirement Benefits" for impact to our defined benefit pension plans. agreement with Miller in Canada. See Note 19, "Commitments and Contingencies" for further discussion. determined that our Home Draft package was not meeting expectations driven by a lack of demand in the U.K, markct and as a result, we recognized (2)During 2013, 2012 and 2011, we recognized charges for pension curtailment and special termination benefits related to certain defined benefit (3)During the fourth quarter of 2013, we recognized an impairment charge related to our definite-lived intangible asset associated with our licensing (4)During the second quarter of 2012, we recognized an asset abandonment charge relsted to the discontinuation of primary packaging in the U.K. We a loss related to the write-off of the Home Draft packaging line, tooling equipment and packaging materials inventory (5) g the third quarter of 2013, we recognized impairment charges related to indefinite-lived intangible assets in Burope. See Note 12, "Goodwill and Intangible Assets" for further discussion. (6)In December of 2013, we sold our interest in the MC Si'hai joint venture in China and recognized a gain of $6.0 million. The gain consists of the non-cash release of the $5.4 million liability representing the fair value of our remaining investment upon deconsolidation of the joint venture in 2012, as well as $0.6 million of proceeds received for our interest in the joint venture. We also recognized legal and related fees in relation to the sale of $1.2 million during 2013 In the second quarter of 2012, we recognized impairment charges of $10.4 million related to goodwill and definite-lived intangible assets in our MC Si'hai joint venture in China, and in the third quarter of 2012, we deconsolidated the joint venture and recognized an impairment loss of $27.6 million upon deconsolidation. See Note 5, "Investments" for fiurther discussion of the deconsolidation and subscquent sale of the joint venture. During 2012, we received insurance proceeds in excess of expenses incurred related to flood damages at our Toronto offices. During 2011 incurred expenses in excess of insurance proceeds related to these damages. we (8)During the second quarter of 2011, we recognized a $2.0 million gain resulting from a reduction of our guarantee of BRI debt obligations. (9) During the second quarter of 2011, we recognized a $7.6 million loss related to the correction of an immaterial crror in prior periods in the Canada segment, resulting frorn the performance of a fixed asset count that reduced properties by $13.9 million m 2011The adjustment also resulted in an increase to goodwill of $6.3 million for the assets identified as not present as of the Merger date. The impact of the error and the related correction in 2011 was not material to any prior annual or interim financial statements and was not material to the fiscal year results for 2011. (10) During 2009, we established a non-income-related tax reserve of $10.4 million that was recorded as a special item. Our estimates indicated a range of possible loss relative to this reserve of zero to S22.3 million, inclusive of potential penalties and interest. The amounts recorded in 2013, 2012 and 2011 represent the release of this reserve as a result of a change in estimate. As a result, the remaining amount of this non-income-related tax reserve was fully released in 2013 (11) During 2013, we recorded losses and rolated net costs of $5.4 million in our Europe business related to significant flooding in Czech Republic in the second quarter of 2013. These losses were offset by $7.4 million insurance proceeds received in 2013 Upon termination of our Tradeteam distribution agreements and subsequent termination ofthe oint venture and sale of our 49.9% interest m Tradeteam to DHL, we recognized a loss of $13.2 million in December 2013. See Note 5, "Investments" for further discussion. (12) In addition to the previously mentioned termination-related items recorded in special items, in the fourth quarter of 2013 we received termination notifications from Modelo and Heineken related to our MMI joint venture agreement and contract-brewing agreement, respectively. Upon temination of the MMI joint venture, which is expected to occur at the end of the day on February 28, 2014, we expect to recognize termination fce income of CAD 70.0 million, net of the remaining carrying value of the defnite-lived intangible asset, within special items. See Note 5, "Investments" for further discussion. Additionally, we have a contract brewing and kegging agreement with Heineken whereby we produce and package the Foster's and Kronenbourg brands in the U.K. In December 2013, we entered into an agreement with Heineken to early terminate this arrangement. As a result of the termination, Heineken has agreed to pay us an aggregate early termination payment of GBP 13.0million during and through the end of the transition period, concluding on April 30, 2015, which will boe recognized within special items. Restructuring Activities In 2012, we introduced several initiatives focused on increasing our efficiencies and reducing costs across all functions of the business in order to develop a more competitive supply chain and global cost structure. Included in these initiatives is a long-term focus on reducing labor and general overhead costs through restructuring activities. We view these restructuring activities as actions to allow us to meet our long-term growth targets by generating future cost savings within cost of goods sold and general and administrative expenses and include organizational changes that strengthen our business and accelerate efficiencies within our operational structure. As a result of these restructuring activities, we have reduced headcount by approximately 910 employees, of which 310 and 600 relate to 2013 and 2012 activities, respectively. Consequently, we recognized severance and other employee related charges during 2013 and 2012, which we have recorded as special items within our consolidated statements of operations. As we continually evaluate our cost structure and seek opportunities for further efficiencics and cost savings, we may incur additional restructuring related charges in the future, however, are unable to estimate the amount of charges at this time