Answered step by step

Verified Expert Solution

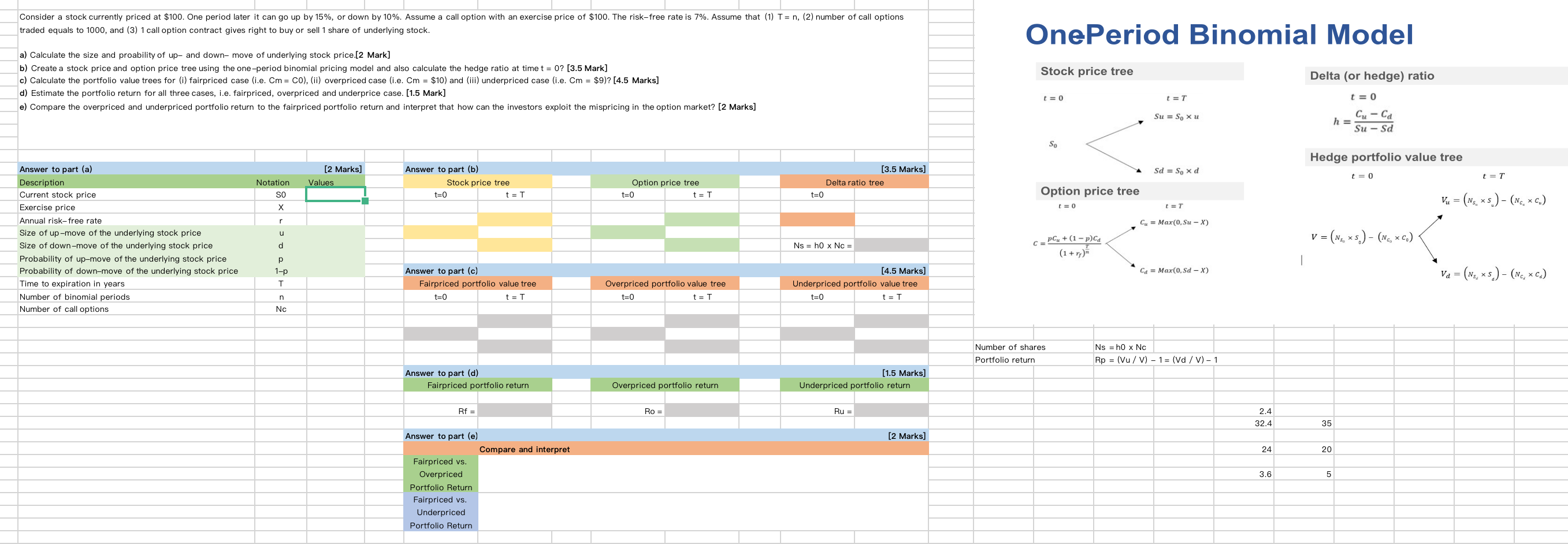

Question

1 Approved Answer

OnePeriod Binomial Model Stock price tree [ begin{array}{c} text { Delta (or hedge) ratio } qquad begin{array}{c} t=0 h=frac{C_{u}-c_{d}}{S u-S d} end{array} end{array}

OnePeriod Binomial Model Stock price tree \\[ \\begin{array}{c} \\text { Delta (or hedge) ratio } \\\\ \\qquad \\begin{array}{c} t=0 \\\\ h=\\frac{C_{u}-c_{d}}{S u-S d} \\end{array} \\end{array} \\] Hedge portfolio value tree

OnePeriod Binomial Model Stock price tree \\[ \\begin{array}{c} \\text { Delta (or hedge) ratio } \\\\ \\qquad \\begin{array}{c} t=0 \\\\ h=\\frac{C_{u}-c_{d}}{S u-S d} \\end{array} \\end{array} \\] Hedge portfolio value tree Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investing

Authors: Scott B. Smart, Lawrence J. Gitman, Michael D. Joehnk

12th edition

978-0133075403, 133075354, 9780133423938, 133075400, 013342393X, 978-0133075359