Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Only equations, please!!!!!!!!!!! Only equations, please!!!!!!!!!!! Question 1 (40 marks) Refer to Figure 1. Write the Excel formula for each cell marked with ?? in

Only equations, please!!!!!!!!!!!

Only equations, please!!!!!!!!!!!

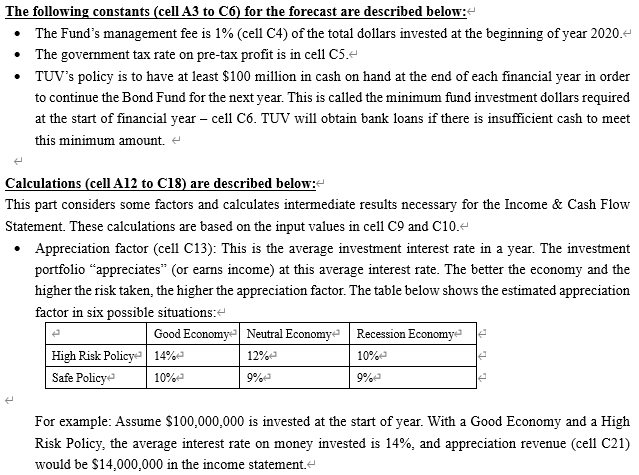

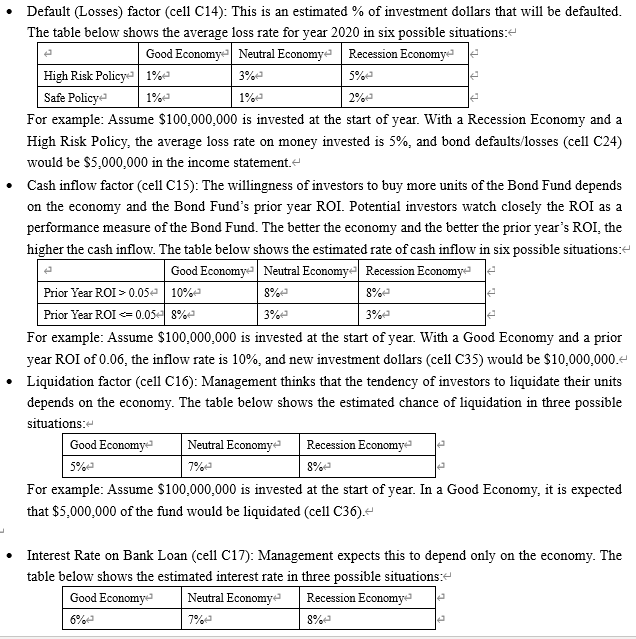

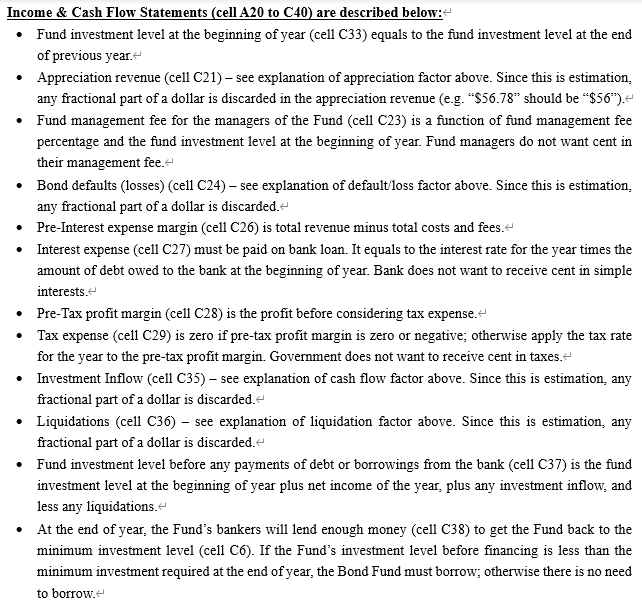

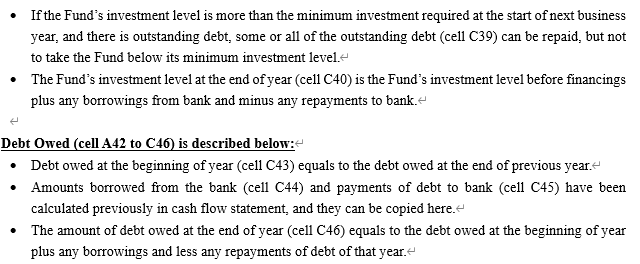

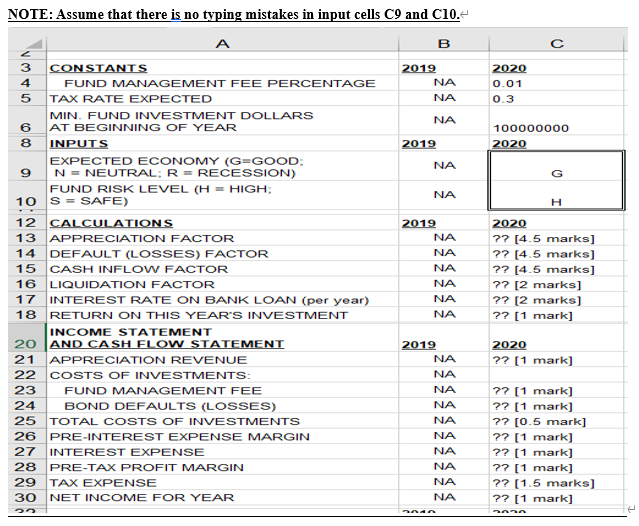

Question 1 (40 marks) Refer to Figure 1. Write the Excel formula for each cell marked with ?? in column C. and label each formula clearly with cell reference position. TUV Investment Company manages a family of mutual funds. TUV recently started a new fund called the Bond Fund at the end of year 2019. For year 2020, the Bond Fund's management wants to know if they should choose high or low risk investments, and how their choice might be affected by a changing economy. High risk and high reward (or interests) go hand-in-hand. Companies in high-risk industries must offer high interest rates on bonds they issue to attract investors, who know that the chance of default (or loss) is greater with high-risk companies. By contrast, companies in low-risk industries can offer lower interest rates. For example, U.S. Government bonds have very low risks because U.S. Government can't default or bankrupt. Bonds issued by some blue-chip companies may have high risks because these companies may default or bankrupt at any time. Another factor affecting interest rates is the general state of economy. In a good economy, companies compete for capital, so interest rates offered to investors go up. In a recession economy, interest rates go down. In a good economy, defaults are less likely. In a recession economy, companies have trouble making ends meet and the chance of defaults increase. You are required to make a what-if analysis in Microsoft Excel (see Net income from previous years reinvested in new bonds. Investors send in money for units of the Bond Fund; this is called "inflow factor. Bond Fund managers borrow money from the bank if total dollars in Bond Fund at the end of year fall below $100 million, which is the minimum fund investment dollars at the beginning of year 2020 (cell C6). The Bond Fund's total invested dollars could be reduced in two ways: Investors cash out their units, and fund managers must liquidate some Fund investments to pay these investors. This is called the "liquidation factor. A bond issuer defaults, announcing it is not going to repay its debt. This means that the now-worthless investment must be written off as an expense in the Fund income statement The following constants (cell A3 to C6) for the forecast are described below: The Fund's management fee is 1% (cell C4) of the total dollars invested at the beginning of year 2020.- The government tax rate on pre-tax profit is in cell C5.- TUV's policy is to have at least $100 million in cash on hand at the end of each financial year in order to continue the Bond Fund for the next year. This is called the minimum fund investment dollars required at the start of financial year -cell C6. TUV will obtain bank loans if there is insufficient cash to meet this minimum amount Calculations (cell A12 to C18) are described below: This part considers some factors and calculates intermediate results necessary for the Income & Cash Flow Statement. These calculations are based on the input values in cell C9 and C10. Appreciation factor (cell C13): This is the average investment interest rate in a year. The investment portfolio "appreciates" (or earns income) at this average interest rate. The better the economy and the higher the risk taken, the higher the appreciation factor. The table below shows the estimated appreciation factor in six possible situations: Good Economy Neutral Economye Recession Economye le High Risk Policy | 14% 12% Safe Policy 10% 9% 10% 9% For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a High Risk Policy, the average interest rate on money invested is 14%, and appreciation revenue (cell C21) would be $14,000,000 in the income statement. 1% Default (Losses) factor (cell C14): This is an estimated % of investment dollars that will be defaulted. The table below shows the average loss rate for year 2020 in six possible situations: Good Economy Neutral Economye Recession Economy High Risk Policy | 1% 3% 5% Safe Policy 1%- 2% For example: Assume $100,000,000 is invested at the start of year. With a Recession Economy and a High Risk Policy, the average loss rate on money invested is 5%, and bond defaults/losses (cell C24) would be $5,000,000 in the income statement Cash inflow factor (cell C15): The willingness of investors to buy more units of the Bond Fund depends on the economy and the Bond Fund's prior year ROI. Potential investors watch closely the ROI as a performance measure of the Bond Fund. The better the economy and the better the prior year's ROI, the higher the cash inflow. The table below shows the estimated rate of cash inflow in six possible situations: Good Economy Neutral Economy Recession Economy Prior Year ROI >0.05- 10% 8% Prior Year ROI = 0.054 8% 3% 3% For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a prior year ROI of 0.06, the inflow rate is 10%, and new investment dollars (cell C35) would be $10,000,000.- Liquidation factor (cell C16): Management thinks that the tendency of investors to liquidate their units depends on the economy. The table below shows the estimated chance of liquidation in three possible situations: Good Economy Neutral Economy Recession Economy 8% For example: Assume $100,000,000 is invested at the start of year. In a Good Economy, it is expected that $5,000,000 of the fund would be liquidated (cell C36). 8% 5% 7% Interest Rate on Bank Loan (cell C17): Management expects this to depend only on the economy. The table below shows the estimated interest rate in three possible situations: Good Economy Neutral Economy Recession Economy 6% 8% 7% Income & Cash Flow Statements (cell A20 to C40) are described below: Fund investment level at the beginning of year (cell C33) equals to the fund investment level at the end of previous year. Appreciation revenue (cell C21) - see explanation of appreciation factor above. Since this is estimation, any fractional part of a dollar is discarded in the appreciation revenue (e.g. "$56.78" should be "$56"). Fund management fee for the managers of the Fund (cell C23) is a function of fund management fee percentage and the fund investment level at the beginning of year. Fund managers do not want cent in their management fee. Bond defaults (losses) (cell C24) see explanation of default loss factor above. Since this is estimation, any fractional part of a dollar is discarded. Pre-Interest expense margin (cell C26) is total revenue minus total costs and fees.' Interest expense (cell C27) must be paid on bank loan. It equals to the interest rate for the year times the amount of debt owed to the bank at the beginning of year. Bank does not want to receive cent in simple interests. Pre-Tax profit margin (cell C28) is the profit before considering tax expense. Tax expense (cell C29) is zero if pre-tax profit margin is zero or negative; otherwise apply the tax rate for the year to the pre-tax profit margin. Government does not want to receive cent in taxes. Investment Inflow (cell C35) see explanation of cash flow factor above. Since this is estimation, any fractional part of a dollar is discarded. Liquidations (cell C36) - see explanation of liquidation factor above. Since this is estimation, any fractional part of a dollar is discarded. Fund investment level before any payments of debt or borrowings from the bank (cell C37) is the fund investment level at the beginning of year plus net income of the year, plus any investment inflow, and less any liquidations. At the end of year, the Fund's bankers will lend enough money (cell C38) to get the Fund back to the minimum investment level (cell C6). If the Fund's investment level before financing is less than the minimum investment required at the end of year, the Bond Fund must borrow; otherwise there is no need to borrow. If the Fund's investment level is more than the minimum investment required at the start of next business year, and there is outstanding debt, some or all of the outstanding debt (cell C39) can be repaid, but not to take the Fund below its minimum investment level. The Fund's investment level at the end of year (cell C40) is the Fund's investment level before financings plus any borrowings from bank and minus any repayments to bank. Debt Owed (cell A42 to C46) is described below: Debt owed at the beginning of year (cell C43) equals to the debt owed at the end of previous year. Amounts borrowed from the bank (cell C44) and payments of debt to bank (cell C45) have been calculated previously in cash flow statement, and they can be copied here. The amount of debt owed at the end of year (cell C46) equals to the debt owed at the beginning of year plus any borrowings and less any repayments of debt of that year. NOTE: Assume that there is no typing mistakes in input cells C9 and C10.- B uman 2019 NA NA 2020 0.01 0.3 NA 100000000 2020 2019 NA 9 G NA H 3 CONSTANTS 4 FUND MANAGEMENT FEE PERCENTAGE 5 TAX RATE EXPECTED MIN. FUND INVESTMENT DOLLARS 6 AT BEGINNING OF YEAR 8 INPUTS EXPECTED ECONOMY (G=GOOD N = NEUTRAL; R = RECESSION) FUND RISK LEVEL (H = HIGH: 10 S = SAFE) 12 CALCULATIONS 13 APPRECIATION FACTOR 14 DEFAULT (LOSSES) FACTOR 15 CASH INFLOW FACTOR 16 LIQUIDATION FACTOR 17 INTEREST RATE ON BANK LOAN (per year) 18 RETURN ON THIS YEAR'S INVESTMENT INCOME STATEMENT 20 AND CASH FLOW STATEMENT 21 APPRECIATION REVENUE 22 COSTS OF INVESTMENTS: 23 FUND MANAGEMENT FEE 24 BOND DEFAULTS (LOSSES) 25 TOTAL COSTS OF INVESTMENTS 26 PRE-INTEREST EXPENSE MARGIN 27 INTEREST EXPENSE 28 PRE-TAX PROFIT MARGIN 29 TAX EXPENSE 30 NET INCOME FOR YEAR 2019 NA NA NA NA NA NA 2020 7? [4.5 marks] ?? [4.5 marks) ?? [4.5 marks] 7? [2 marks] ?? [2 marks] ?? [1 mark] 2020 ?? [1 mark] 2019 NA NA NA NA NA NA NA NA NA NA 77 [1 mark) ?? [1 mark] ?? [0.5 mark] ?? [1 mark] ?? [1 mark] 7? [1 mark] ?? (1.5 marks) ?? [1 mark] JO Ann B 2019 NA 2020 ?? [0.5 mark] ?? [0.5 mark] ?? [1 mark] ?? [1 mark] NA NA NA A 32 FUND INVESTMENT LEVEL 33 AT BEGINNING OF YEAR 34 ADD: FUND NET INCOME FOR YEAR 35 ADD: INVESTMENT INFLOW 36 LESS: LIQUIDATIONS FUND INVESTMENT LEVEL 37 BEFORE FINANCINGS 38 ADD: BORROWINGS FROM BANK 39 LESS: REPAYMENTS TO BANK 40 FUND INVESTMENT LEVEL AT YEAR END 42 DEBT OWED 43 OWED TO BANK AT BEGINNING OF YEAR 44 ADD: BORROWINGS IN YEAR 45 LESS: DEBT REPAYMENTS/YR 46 EQUALS: OWED TO BANK AT END OF YEAR ?? [1 marks] NA ?? (1.5 marks] NA ?? [4 marks] 106000000 ?? [1 mark] 2019 2020 NA ?? [0.5 mark] NA 7? (0.5 mark] NA ?? [0.5 mark] 10000000 ?? (0.5 mark] Figure 1: (NA stands for Not Applicable) Question 1 (40 marks) Refer to Figure 1. Write the Excel formula for each cell marked with ?? in column C. and label each formula clearly with cell reference position. TUV Investment Company manages a family of mutual funds. TUV recently started a new fund called the Bond Fund at the end of year 2019. For year 2020, the Bond Fund's management wants to know if they should choose high or low risk investments, and how their choice might be affected by a changing economy. High risk and high reward (or interests) go hand-in-hand. Companies in high-risk industries must offer high interest rates on bonds they issue to attract investors, who know that the chance of default (or loss) is greater with high-risk companies. By contrast, companies in low-risk industries can offer lower interest rates. For example, U.S. Government bonds have very low risks because U.S. Government can't default or bankrupt. Bonds issued by some blue-chip companies may have high risks because these companies may default or bankrupt at any time. Another factor affecting interest rates is the general state of economy. In a good economy, companies compete for capital, so interest rates offered to investors go up. In a recession economy, interest rates go down. In a good economy, defaults are less likely. In a recession economy, companies have trouble making ends meet and the chance of defaults increase. You are required to make a what-if analysis in Microsoft Excel (see Net income from previous years reinvested in new bonds. Investors send in money for units of the Bond Fund; this is called "inflow factor. Bond Fund managers borrow money from the bank if total dollars in Bond Fund at the end of year fall below $100 million, which is the minimum fund investment dollars at the beginning of year 2020 (cell C6). The Bond Fund's total invested dollars could be reduced in two ways: Investors cash out their units, and fund managers must liquidate some Fund investments to pay these investors. This is called the "liquidation factor. A bond issuer defaults, announcing it is not going to repay its debt. This means that the now-worthless investment must be written off as an expense in the Fund income statement The following constants (cell A3 to C6) for the forecast are described below: The Fund's management fee is 1% (cell C4) of the total dollars invested at the beginning of year 2020.- The government tax rate on pre-tax profit is in cell C5.- TUV's policy is to have at least $100 million in cash on hand at the end of each financial year in order to continue the Bond Fund for the next year. This is called the minimum fund investment dollars required at the start of financial year -cell C6. TUV will obtain bank loans if there is insufficient cash to meet this minimum amount Calculations (cell A12 to C18) are described below: This part considers some factors and calculates intermediate results necessary for the Income & Cash Flow Statement. These calculations are based on the input values in cell C9 and C10. Appreciation factor (cell C13): This is the average investment interest rate in a year. The investment portfolio "appreciates" (or earns income) at this average interest rate. The better the economy and the higher the risk taken, the higher the appreciation factor. The table below shows the estimated appreciation factor in six possible situations: Good Economy Neutral Economye Recession Economye le High Risk Policy | 14% 12% Safe Policy 10% 9% 10% 9% For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a High Risk Policy, the average interest rate on money invested is 14%, and appreciation revenue (cell C21) would be $14,000,000 in the income statement. 1% Default (Losses) factor (cell C14): This is an estimated % of investment dollars that will be defaulted. The table below shows the average loss rate for year 2020 in six possible situations: Good Economy Neutral Economye Recession Economy High Risk Policy | 1% 3% 5% Safe Policy 1%- 2% For example: Assume $100,000,000 is invested at the start of year. With a Recession Economy and a High Risk Policy, the average loss rate on money invested is 5%, and bond defaults/losses (cell C24) would be $5,000,000 in the income statement Cash inflow factor (cell C15): The willingness of investors to buy more units of the Bond Fund depends on the economy and the Bond Fund's prior year ROI. Potential investors watch closely the ROI as a performance measure of the Bond Fund. The better the economy and the better the prior year's ROI, the higher the cash inflow. The table below shows the estimated rate of cash inflow in six possible situations: Good Economy Neutral Economy Recession Economy Prior Year ROI >0.05- 10% 8% Prior Year ROI = 0.054 8% 3% 3% For example: Assume $100,000,000 is invested at the start of year. With a Good Economy and a prior year ROI of 0.06, the inflow rate is 10%, and new investment dollars (cell C35) would be $10,000,000.- Liquidation factor (cell C16): Management thinks that the tendency of investors to liquidate their units depends on the economy. The table below shows the estimated chance of liquidation in three possible situations: Good Economy Neutral Economy Recession Economy 8% For example: Assume $100,000,000 is invested at the start of year. In a Good Economy, it is expected that $5,000,000 of the fund would be liquidated (cell C36). 8% 5% 7% Interest Rate on Bank Loan (cell C17): Management expects this to depend only on the economy. The table below shows the estimated interest rate in three possible situations: Good Economy Neutral Economy Recession Economy 6% 8% 7% Income & Cash Flow Statements (cell A20 to C40) are described below: Fund investment level at the beginning of year (cell C33) equals to the fund investment level at the end of previous year. Appreciation revenue (cell C21) - see explanation of appreciation factor above. Since this is estimation, any fractional part of a dollar is discarded in the appreciation revenue (e.g. "$56.78" should be "$56"). Fund management fee for the managers of the Fund (cell C23) is a function of fund management fee percentage and the fund investment level at the beginning of year. Fund managers do not want cent in their management fee. Bond defaults (losses) (cell C24) see explanation of default loss factor above. Since this is estimation, any fractional part of a dollar is discarded. Pre-Interest expense margin (cell C26) is total revenue minus total costs and fees.' Interest expense (cell C27) must be paid on bank loan. It equals to the interest rate for the year times the amount of debt owed to the bank at the beginning of year. Bank does not want to receive cent in simple interests. Pre-Tax profit margin (cell C28) is the profit before considering tax expense. Tax expense (cell C29) is zero if pre-tax profit margin is zero or negative; otherwise apply the tax rate for the year to the pre-tax profit margin. Government does not want to receive cent in taxes. Investment Inflow (cell C35) see explanation of cash flow factor above. Since this is estimation, any fractional part of a dollar is discarded. Liquidations (cell C36) - see explanation of liquidation factor above. Since this is estimation, any fractional part of a dollar is discarded. Fund investment level before any payments of debt or borrowings from the bank (cell C37) is the fund investment level at the beginning of year plus net income of the year, plus any investment inflow, and less any liquidations. At the end of year, the Fund's bankers will lend enough money (cell C38) to get the Fund back to the minimum investment level (cell C6). If the Fund's investment level before financing is less than the minimum investment required at the end of year, the Bond Fund must borrow; otherwise there is no need to borrow. If the Fund's investment level is more than the minimum investment required at the start of next business year, and there is outstanding debt, some or all of the outstanding debt (cell C39) can be repaid, but not to take the Fund below its minimum investment level. The Fund's investment level at the end of year (cell C40) is the Fund's investment level before financings plus any borrowings from bank and minus any repayments to bank. Debt Owed (cell A42 to C46) is described below: Debt owed at the beginning of year (cell C43) equals to the debt owed at the end of previous year. Amounts borrowed from the bank (cell C44) and payments of debt to bank (cell C45) have been calculated previously in cash flow statement, and they can be copied here. The amount of debt owed at the end of year (cell C46) equals to the debt owed at the beginning of year plus any borrowings and less any repayments of debt of that year. NOTE: Assume that there is no typing mistakes in input cells C9 and C10.- B uman 2019 NA NA 2020 0.01 0.3 NA 100000000 2020 2019 NA 9 G NA H 3 CONSTANTS 4 FUND MANAGEMENT FEE PERCENTAGE 5 TAX RATE EXPECTED MIN. FUND INVESTMENT DOLLARS 6 AT BEGINNING OF YEAR 8 INPUTS EXPECTED ECONOMY (G=GOOD N = NEUTRAL; R = RECESSION) FUND RISK LEVEL (H = HIGH: 10 S = SAFE) 12 CALCULATIONS 13 APPRECIATION FACTOR 14 DEFAULT (LOSSES) FACTOR 15 CASH INFLOW FACTOR 16 LIQUIDATION FACTOR 17 INTEREST RATE ON BANK LOAN (per year) 18 RETURN ON THIS YEAR'S INVESTMENT INCOME STATEMENT 20 AND CASH FLOW STATEMENT 21 APPRECIATION REVENUE 22 COSTS OF INVESTMENTS: 23 FUND MANAGEMENT FEE 24 BOND DEFAULTS (LOSSES) 25 TOTAL COSTS OF INVESTMENTS 26 PRE-INTEREST EXPENSE MARGIN 27 INTEREST EXPENSE 28 PRE-TAX PROFIT MARGIN 29 TAX EXPENSE 30 NET INCOME FOR YEAR 2019 NA NA NA NA NA NA 2020 7? [4.5 marks] ?? [4.5 marks) ?? [4.5 marks] 7? [2 marks] ?? [2 marks] ?? [1 mark] 2020 ?? [1 mark] 2019 NA NA NA NA NA NA NA NA NA NA 77 [1 mark) ?? [1 mark] ?? [0.5 mark] ?? [1 mark] ?? [1 mark] 7? [1 mark] ?? (1.5 marks) ?? [1 mark] JO Ann B 2019 NA 2020 ?? [0.5 mark] ?? [0.5 mark] ?? [1 mark] ?? [1 mark] NA NA NA A 32 FUND INVESTMENT LEVEL 33 AT BEGINNING OF YEAR 34 ADD: FUND NET INCOME FOR YEAR 35 ADD: INVESTMENT INFLOW 36 LESS: LIQUIDATIONS FUND INVESTMENT LEVEL 37 BEFORE FINANCINGS 38 ADD: BORROWINGS FROM BANK 39 LESS: REPAYMENTS TO BANK 40 FUND INVESTMENT LEVEL AT YEAR END 42 DEBT OWED 43 OWED TO BANK AT BEGINNING OF YEAR 44 ADD: BORROWINGS IN YEAR 45 LESS: DEBT REPAYMENTS/YR 46 EQUALS: OWED TO BANK AT END OF YEAR ?? [1 marks] NA ?? (1.5 marks] NA ?? [4 marks] 106000000 ?? [1 mark] 2019 2020 NA ?? [0.5 mark] NA 7? (0.5 mark] NA ?? [0.5 mark] 10000000 ?? (0.5 mark] Figure 1: (NA stands for Not Applicable)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Investment Analysis And Portfolio Management

Authors: Frank K. Reilly, Keith C. Brown

6th Edition

003025809X, 978-3540014386