Answered step by step

Verified Expert Solution

Question

1 Approved Answer

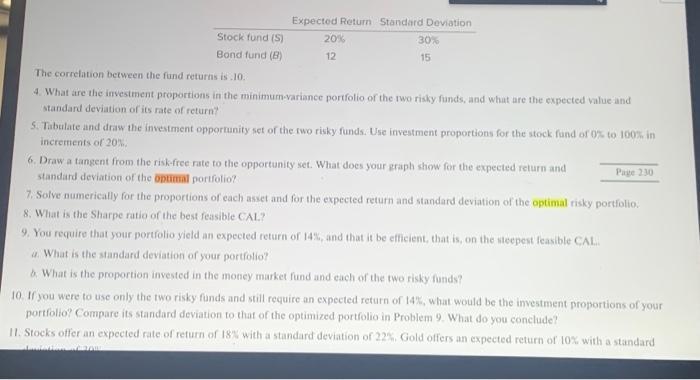

ONLY NEED ANSWER TO #6 & #7 Stock fund (S) Bond fund (B) Expected Return Standard Deviation 20% 12 30% 15 The correlation between the

ONLY NEED ANSWER TO #6 & #7

Stock fund (S) Bond fund (B) Expected Return Standard Deviation 20% 12 30% 15 The correlation between the fund returns is .10.

6. Draw a tangent from the risk-free rate to the opportunity set. What does your graph show for the expected return and standard deviation of the optimal portfolio? 7. Solve numerically for the proportions of each asset and for the expected return and standard deviation of the optimal risky portfolio.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How Much Can I Spend In Retirement A Guide To Investment Based Retirement Income Strategies

Authors: Wade D Pfau

1st Edition

1945640022, 978-1945640025