Answered step by step

Verified Expert Solution

Question

1 Approved Answer

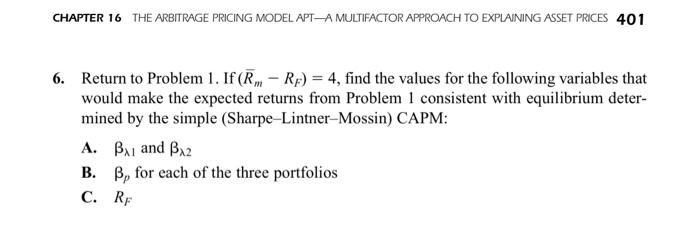

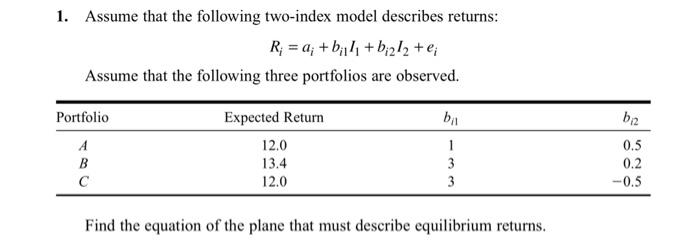

only question 6 needed thank you! CHAPTER 16 THE ARBITRAGE PRICING MODEL APT-A MULTIFACTOR APPROACH TO EXPLAINING ASSET PRICES 401 6. Return to Problem 1.

only question 6 needed thank you!

CHAPTER 16 THE ARBITRAGE PRICING MODEL APT-A MULTIFACTOR APPROACH TO EXPLAINING ASSET PRICES 401 6. Return to Problem 1. If(RM - Rp) = 4, find the values for the following variables that would make the expected returns from Problem I consistent with equilibrium deter- mined by the simple (Sharpe-Lintner-Mossin) CAPM: A. B and B2 B. B, for each of the three portfolios C. RF 1. Assume that the following two-index model describes returns: R; = a; +42 +b;272 +e; Assume that the following three portfolios are observed. Portfolio bi b2 Expected Return 12.0 13.4 12.0 B 1 3 3 0.5 0.2 -0.5 Find the equation of the plane that must describe equilibrium returns. CHAPTER 16 THE ARBITRAGE PRICING MODEL APT-A MULTIFACTOR APPROACH TO EXPLAINING ASSET PRICES 401 6. Return to Problem 1. If(RM - Rp) = 4, find the values for the following variables that would make the expected returns from Problem I consistent with equilibrium deter- mined by the simple (Sharpe-Lintner-Mossin) CAPM: A. B and B2 B. B, for each of the three portfolios C. RF 1. Assume that the following two-index model describes returns: R; = a; +42 +b;272 +e; Assume that the following three portfolios are observed. Portfolio bi b2 Expected Return 12.0 13.4 12.0 B 1 3 3 0.5 0.2 -0.5 Find the equation of the plane that must describe equilibrium returns Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Lifestyle Investor

Authors: Justin Donald, Ryan Levesque, Mike Koenigs

1st Edition

1636800130, 978-1636800134