| Operating profit (excluding the items listed below) | $91,300 |

| Rental income | 19,000 |

| Interest income: | |

| Municipal bonds (tax-exempt) | 12,000 |

| Corporate bonds | 1,200 |

| Dividend income (all from less-than-20%-owned domestic corporations) | 21,000 |

| Gains and losses on property sales: | |

| Gain on sale of land held as an investment (contributed by Ray six | |

| years ago when its basis was $10,000 and its FMV was $17,000) | 85,000 |

| Long-term capital gains | 8,000 |

| Short-term capital losses | 6,000 |

| Sec. 1231 gain | 10,000 |

| Unrecaptured Sec. 1250 gain | 51,000 |

| Depreciation: | |

| Rental real estate | 11,000 |

| Machinery and equipment | 24,000 |

| Interest expense related to: | |

| Mortgages on rental property | 21,000 |

| Loans to acquire municipal bonds | 1,500 |

| Guaranteed payments to Ray | 25,000 |

| Low-income housing expenditures qualifying for credit | 23,000 |

More Information below:

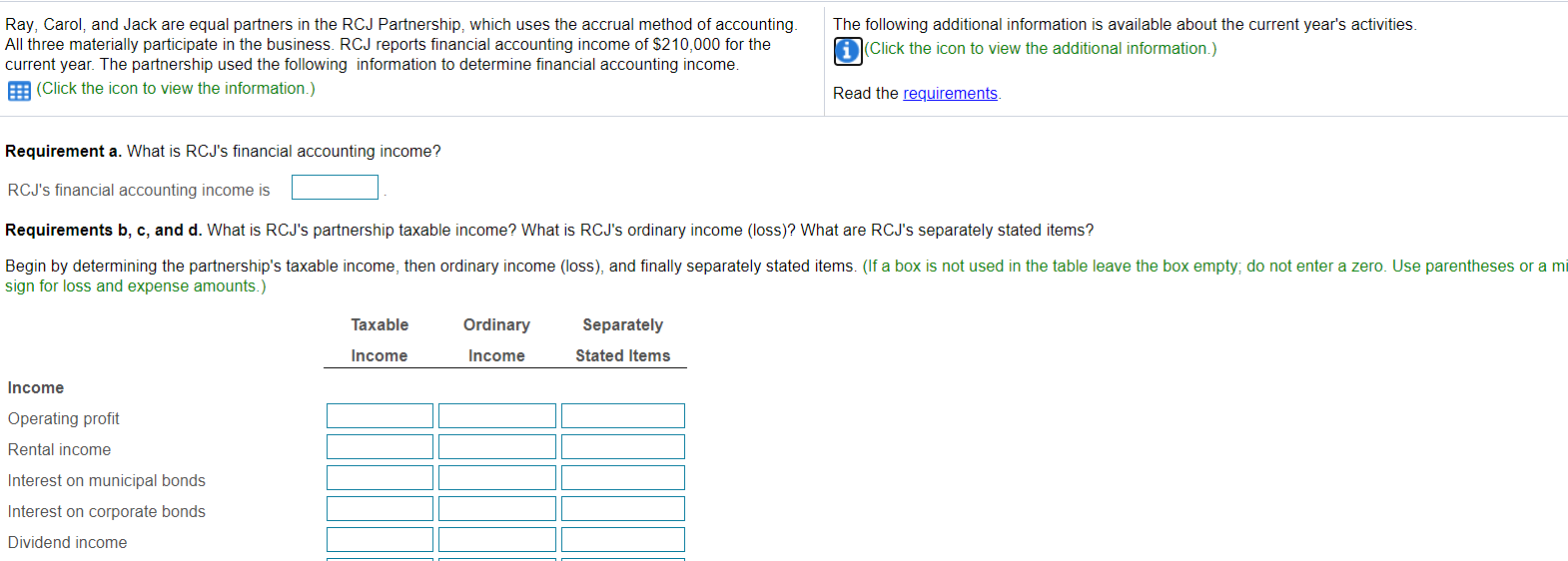

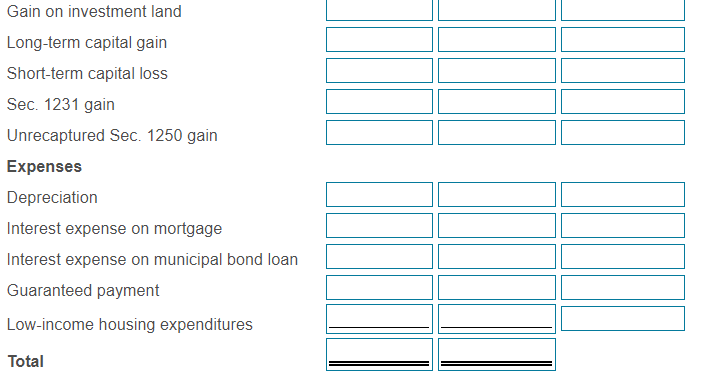

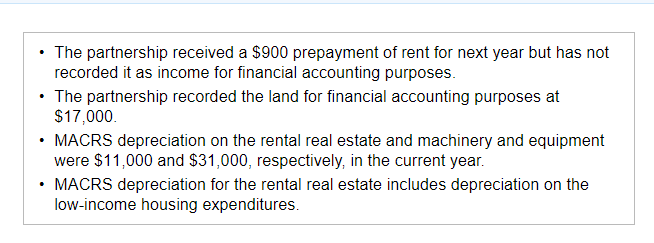

Ray, Carol, and Jack are equal partners in the RCJ Partnership, which uses the accrual method of accounting. All three materially participate in the business. RCJ reports financial accounting income of $210,000 for the current year. The partnership used the following information to determine financial accounting income. (Click the icon to view the information.) The following additional information is available about the current year's activities. Click the icon to view the additional information.) Read the requirements. Requirement a. What is RCJ's financial accounting income? RCJ's financial accounting income is Requirements b, c, and d. What is RCJ's partnership taxable income? What is RCJ's ordinary income (loss)? What are RCJ's separately stated items? Begin by determining the partnership's taxable income, then ordinary income (loss), and finally separately stated items. (If a box is not used in the table leave the box empty, do not enter a zero. Use parentheses or a mi sign for loss and expense amounts.) Taxable Ordinary Separately Income Income Stated Items Income Operating profit Rental income Interest on municipal bonds Interest on corporate bonds Dividend income Gain on investment land Long-term capital gain Short-term capital loss Sec. 1231 gain Unrecaptured Sec. 1250 gain Expenses Depreciation Interest expense on mortgage Interest expense on municipal bond loan Guaranteed payment Low-income housing expenditures Total The partnership received a $900 prepayment of rent for next year but has not recorded it as income for financial accounting purposes. The partnership recorded the land for financial accounting purposes at $17,000 MACRS depreciation on the rental real estate and machinery and equipment were $11,000 and $31,000, respectively, in the current year. MACRS depreciation for the rental real estate includes depreciation on the low-income housing expenditures. Ray, Carol, and Jack are equal partners in the RCJ Partnership, which uses the accrual method of accounting. All three materially participate in the business. RCJ reports financial accounting income of $210,000 for the current year. The partnership used the following information to determine financial accounting income. (Click the icon to view the information.) The following additional information is available about the current year's activities. Click the icon to view the additional information.) Read the requirements. Requirement a. What is RCJ's financial accounting income? RCJ's financial accounting income is Requirements b, c, and d. What is RCJ's partnership taxable income? What is RCJ's ordinary income (loss)? What are RCJ's separately stated items? Begin by determining the partnership's taxable income, then ordinary income (loss), and finally separately stated items. (If a box is not used in the table leave the box empty, do not enter a zero. Use parentheses or a mi sign for loss and expense amounts.) Taxable Ordinary Separately Income Income Stated Items Income Operating profit Rental income Interest on municipal bonds Interest on corporate bonds Dividend income Gain on investment land Long-term capital gain Short-term capital loss Sec. 1231 gain Unrecaptured Sec. 1250 gain Expenses Depreciation Interest expense on mortgage Interest expense on municipal bond loan Guaranteed payment Low-income housing expenditures Total The partnership received a $900 prepayment of rent for next year but has not recorded it as income for financial accounting purposes. The partnership recorded the land for financial accounting purposes at $17,000 MACRS depreciation on the rental real estate and machinery and equipment were $11,000 and $31,000, respectively, in the current year. MACRS depreciation for the rental real estate includes depreciation on the low-income housing expenditures