Answered step by step

Verified Expert Solution

Question

1 Approved Answer

otherwise. The 'select all that apply' questions require more than one correct answer. Santa's Workshop Inc. is gearing up for the holiday season. The following

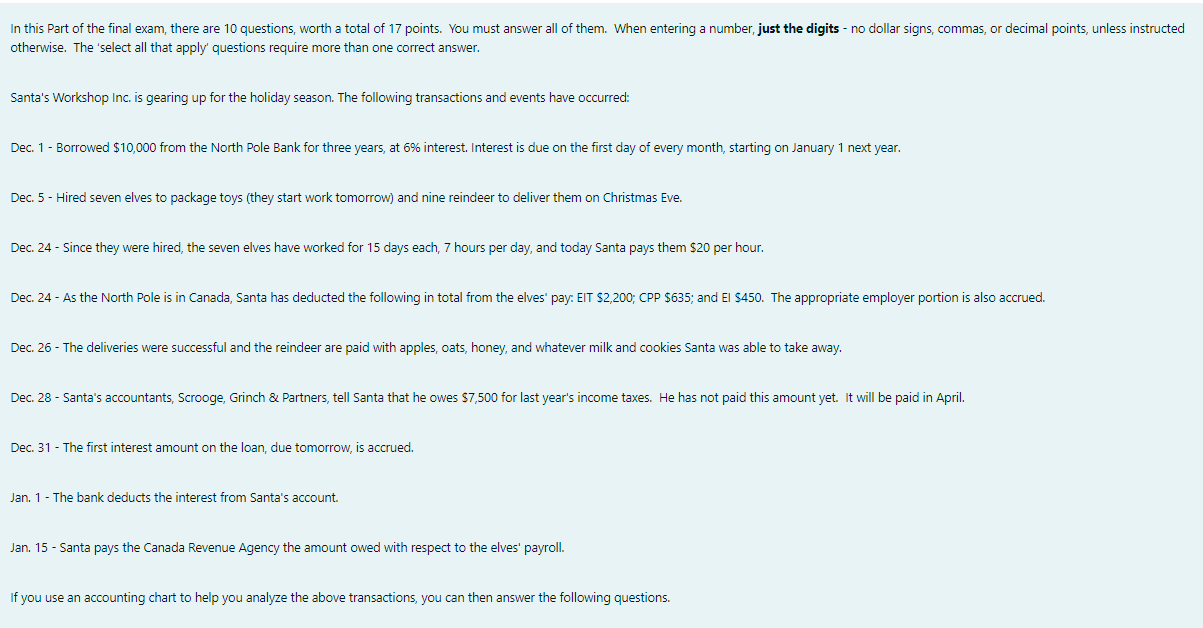

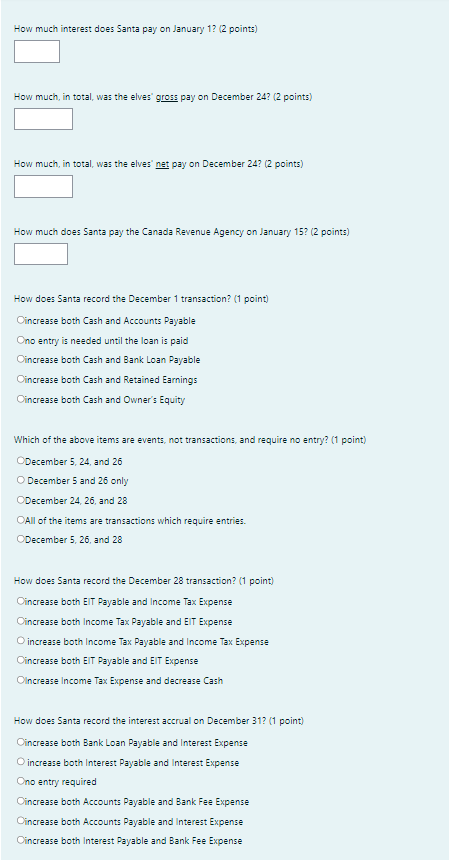

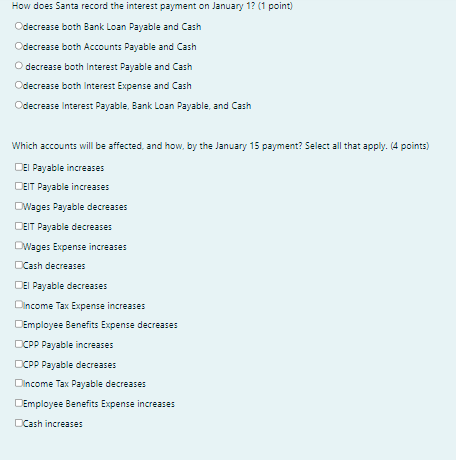

otherwise. The 'select all that apply' questions require more than one correct answer. Santa's Workshop Inc. is gearing up for the holiday season. The following transactions and events have occurred: Dec. 1 - Borrowed $10,000 from the North Pole Bank for three years, at 6% interest. Interest is due on the first day of every month, starting on January 1 next year. Dec. 5 - Hired seven elves to package toys (they start work tomorrow) and nine reindeer to deliver them on Christmas Eve. Dec. 24 - Since they were hired, the seven elves have worked for 15 days each, 7 hours per day, and today Santa pays them $20 per hour. Dec. 26 - The deliveries were successful and the reindeer are paid with apples, oats, honey, and whatever milk and cookies Santa was able to take away. Dec. 28 - Santa's accountants, Scrooge, Grinch \& Partners, tell Santa that he owes $7,500 for last year's income taxes. He has not paid this amount yet. It will be paid in April. Dec. 31 - The first interest amount on the loan, due tomorrow, is accrued. Jan. 1 - The bank deducts the interest from Santa's account. Jan. 15 - Santa pays the Canada Revenue Agency the amount owed with respect to the elves' payroll. If you use an accounting chart to help you analyze the above transactions, you can then answer the following questions. How much interest does Santa pay on January 1 ? ( 2 points) How much, in total, was the elves' gross pay on December 24 ? (2 points) How much, in total, was the elves' net pay on December 24 ? (2 points) How much does Santa pay the Canada Revenue Agency on January 15 ? (2 points) How does Santa record the December 1 transaction? (1 point) increase both Cash and Accounts Payable no entry is needed until the loan is paid increase both Cash and Bank Loan Payable increase both Cash and Retained Earnings increase both Cash and Owner's Equity Which of the above items are events, not transactions, and require no entry? (1 point) December 5,24 , and 26 December 5 and 26 only December 24,26 , and 28 All of the items are transactions which require entries. December 5,26 , and 28 How does Santa record the December 28 transaction? (1 point) increase both EIT Payable and Income Tax Expense increase both Income Tax Payable and EIT Expense increase both Income Tax Payable and Income Tax Expense increase both EIT Payable and EIT Expense Increase Income Tax Expense and decrease Cash How does Santa record the interest accrual on December 31 ? (1 point) increase both Bank Loan Payable and Interest Expense increase both Interest Payable and Interest Expense no entry required increase both Accounts Payable and Bank Fee Expense increase both Accounts Payable and Interest Expense increase both Interest Payable and Bank Fee Expense decrease both Bank Loan Payable and Cash decrease both Accounts Payable and Cash decrease both Interest Payable and Cash decrease both Interest Expense and Cash decrease Interest Payable, Bank Loan Payable, and Cash Which accounts will be affected, and how, by the January 15 payment? Select all that apply. (4 points) El Payable increases EIT Payable increases Wages Payable decreases ElT Payable decreases Nages Expense increases Cash decreases Il Payable decreases Income Tax Expense increases Employee Benefits Expense decreases CPP Payable increases Cop Payable decreases Income Tax Payable decreases Employee Benefits Expense increases Cash increases

otherwise. The 'select all that apply' questions require more than one correct answer. Santa's Workshop Inc. is gearing up for the holiday season. The following transactions and events have occurred: Dec. 1 - Borrowed $10,000 from the North Pole Bank for three years, at 6% interest. Interest is due on the first day of every month, starting on January 1 next year. Dec. 5 - Hired seven elves to package toys (they start work tomorrow) and nine reindeer to deliver them on Christmas Eve. Dec. 24 - Since they were hired, the seven elves have worked for 15 days each, 7 hours per day, and today Santa pays them $20 per hour. Dec. 26 - The deliveries were successful and the reindeer are paid with apples, oats, honey, and whatever milk and cookies Santa was able to take away. Dec. 28 - Santa's accountants, Scrooge, Grinch \& Partners, tell Santa that he owes $7,500 for last year's income taxes. He has not paid this amount yet. It will be paid in April. Dec. 31 - The first interest amount on the loan, due tomorrow, is accrued. Jan. 1 - The bank deducts the interest from Santa's account. Jan. 15 - Santa pays the Canada Revenue Agency the amount owed with respect to the elves' payroll. If you use an accounting chart to help you analyze the above transactions, you can then answer the following questions. How much interest does Santa pay on January 1 ? ( 2 points) How much, in total, was the elves' gross pay on December 24 ? (2 points) How much, in total, was the elves' net pay on December 24 ? (2 points) How much does Santa pay the Canada Revenue Agency on January 15 ? (2 points) How does Santa record the December 1 transaction? (1 point) increase both Cash and Accounts Payable no entry is needed until the loan is paid increase both Cash and Bank Loan Payable increase both Cash and Retained Earnings increase both Cash and Owner's Equity Which of the above items are events, not transactions, and require no entry? (1 point) December 5,24 , and 26 December 5 and 26 only December 24,26 , and 28 All of the items are transactions which require entries. December 5,26 , and 28 How does Santa record the December 28 transaction? (1 point) increase both EIT Payable and Income Tax Expense increase both Income Tax Payable and EIT Expense increase both Income Tax Payable and Income Tax Expense increase both EIT Payable and EIT Expense Increase Income Tax Expense and decrease Cash How does Santa record the interest accrual on December 31 ? (1 point) increase both Bank Loan Payable and Interest Expense increase both Interest Payable and Interest Expense no entry required increase both Accounts Payable and Bank Fee Expense increase both Accounts Payable and Interest Expense increase both Interest Payable and Bank Fee Expense decrease both Bank Loan Payable and Cash decrease both Accounts Payable and Cash decrease both Interest Payable and Cash decrease both Interest Expense and Cash decrease Interest Payable, Bank Loan Payable, and Cash Which accounts will be affected, and how, by the January 15 payment? Select all that apply. (4 points) El Payable increases EIT Payable increases Wages Payable decreases ElT Payable decreases Nages Expense increases Cash decreases Il Payable decreases Income Tax Expense increases Employee Benefits Expense decreases CPP Payable increases Cop Payable decreases Income Tax Payable decreases Employee Benefits Expense increases Cash increases Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started