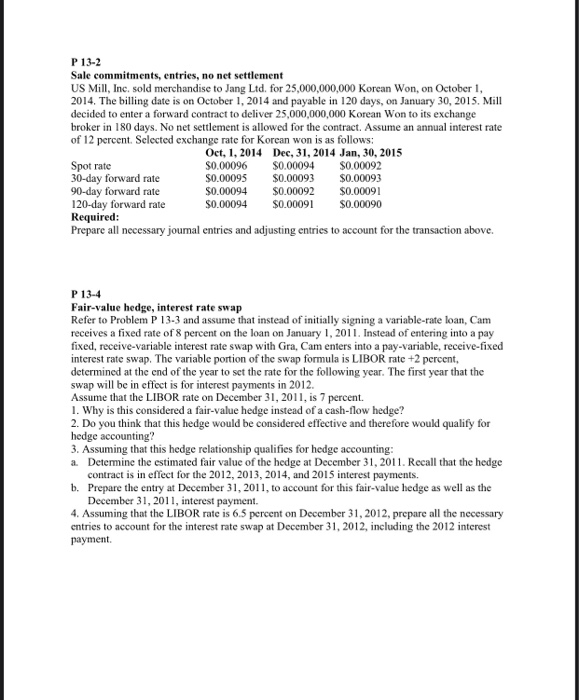

P 13-2 Sale commitments, entries, no net settlement US Mill, Inc. sold merchandise to Jang Ltd. for 25,000,000,000 Korean Won, on October 1, 2014. The billing date is on October 1, 2014 and payable in 120 days, on January 30, 2015. Mill decided to enter a forward contract to deliver 25,000,000,000 Korean Won to its exchange broker in 180 days. No net settlement is allowed for the contract. Assume an annual interest rate of 12 percent. Selected exchange rate for Korean won is as follows: Oct, 1, 2014 Dec, 31, 2014 Jan, 30, 2015 Spot rate $0.00096 $0.00094 50.00092 30-day forward rate $0.00095 $0.00093 $0.00093 90-day forward rate $0.00094 $0.00092 $0.00091 120-day forward rate $0.00094 $0.00091 $0.00090 Required: Prepare all necessary joumal entries and adjusting entries to account for the transaction above. P13-4 Fair-value hedge, interest rate swap Refer to Problem P 13-3 and assume that instead of initially signing a variable-rate loan, Cam receives a fixed rate of 8 percent on the loan on January 1, 2011. Instead of entering into a pay fixed, receive-variable interest rate swap with Gra, Cam enters into a pay-variable, receive-fixed interest rate swap. The variable portion of the swap formula is LIBOR rate +2 percent, determined at the end of the year to set the rate for the following year. The first year that the swap will be in effect is for interest payments in 2012. Assume that the LIBOR rate on December 31, 2011, is 7 percent. 1. Why is this considered a fair-value hedge instead of a cash-flow hedge? 2. Do you think that this hedge would be considered effective and therefore would qualify for hedge accounting? 3. Assuming that this hedge relationship qualifies for hedge accounting: a. Determine the estimated fair value of the hedge at December 31, 2011. Recall that the hedge contract is in effect for the 2012, 2013, 2014, and 2015 interest payments. b. Prepare the entry at December 31, 2011, to account for this fair-value hedge as well as the December 31, 2011, interest payment. 4. Assuming that the LIBOR rate is 6.5 percent on December 31, 2012, prepare all the necessary entries to account for the interest rate swap at December 31, 2012, including the 2012 interest payment P 13-2 Sale commitments, entries, no net settlement US Mill, Inc. sold merchandise to Jang Ltd. for 25,000,000,000 Korean Won, on October 1, 2014. The billing date is on October 1, 2014 and payable in 120 days, on January 30, 2015. Mill decided to enter a forward contract to deliver 25,000,000,000 Korean Won to its exchange broker in 180 days. No net settlement is allowed for the contract. Assume an annual interest rate of 12 percent. Selected exchange rate for Korean won is as follows: Oct, 1, 2014 Dec, 31, 2014 Jan, 30, 2015 Spot rate $0.00096 $0.00094 50.00092 30-day forward rate $0.00095 $0.00093 $0.00093 90-day forward rate $0.00094 $0.00092 $0.00091 120-day forward rate $0.00094 $0.00091 $0.00090 Required: Prepare all necessary joumal entries and adjusting entries to account for the transaction above. P13-4 Fair-value hedge, interest rate swap Refer to Problem P 13-3 and assume that instead of initially signing a variable-rate loan, Cam receives a fixed rate of 8 percent on the loan on January 1, 2011. Instead of entering into a pay fixed, receive-variable interest rate swap with Gra, Cam enters into a pay-variable, receive-fixed interest rate swap. The variable portion of the swap formula is LIBOR rate +2 percent, determined at the end of the year to set the rate for the following year. The first year that the swap will be in effect is for interest payments in 2012. Assume that the LIBOR rate on December 31, 2011, is 7 percent. 1. Why is this considered a fair-value hedge instead of a cash-flow hedge? 2. Do you think that this hedge would be considered effective and therefore would qualify for hedge accounting? 3. Assuming that this hedge relationship qualifies for hedge accounting: a. Determine the estimated fair value of the hedge at December 31, 2011. Recall that the hedge contract is in effect for the 2012, 2013, 2014, and 2015 interest payments. b. Prepare the entry at December 31, 2011, to account for this fair-value hedge as well as the December 31, 2011, interest payment. 4. Assuming that the LIBOR rate is 6.5 percent on December 31, 2012, prepare all the necessary entries to account for the interest rate swap at December 31, 2012, including the 2012 interest payment