Answered step by step

Verified Expert Solution

Question

1 Approved Answer

page 6-7 Fraud (previously referred to as irregularities) -Intentional misstatements or omissions of amounts or disclosures in financial statements. Audits are concerned with misstatements arising

page 6-7

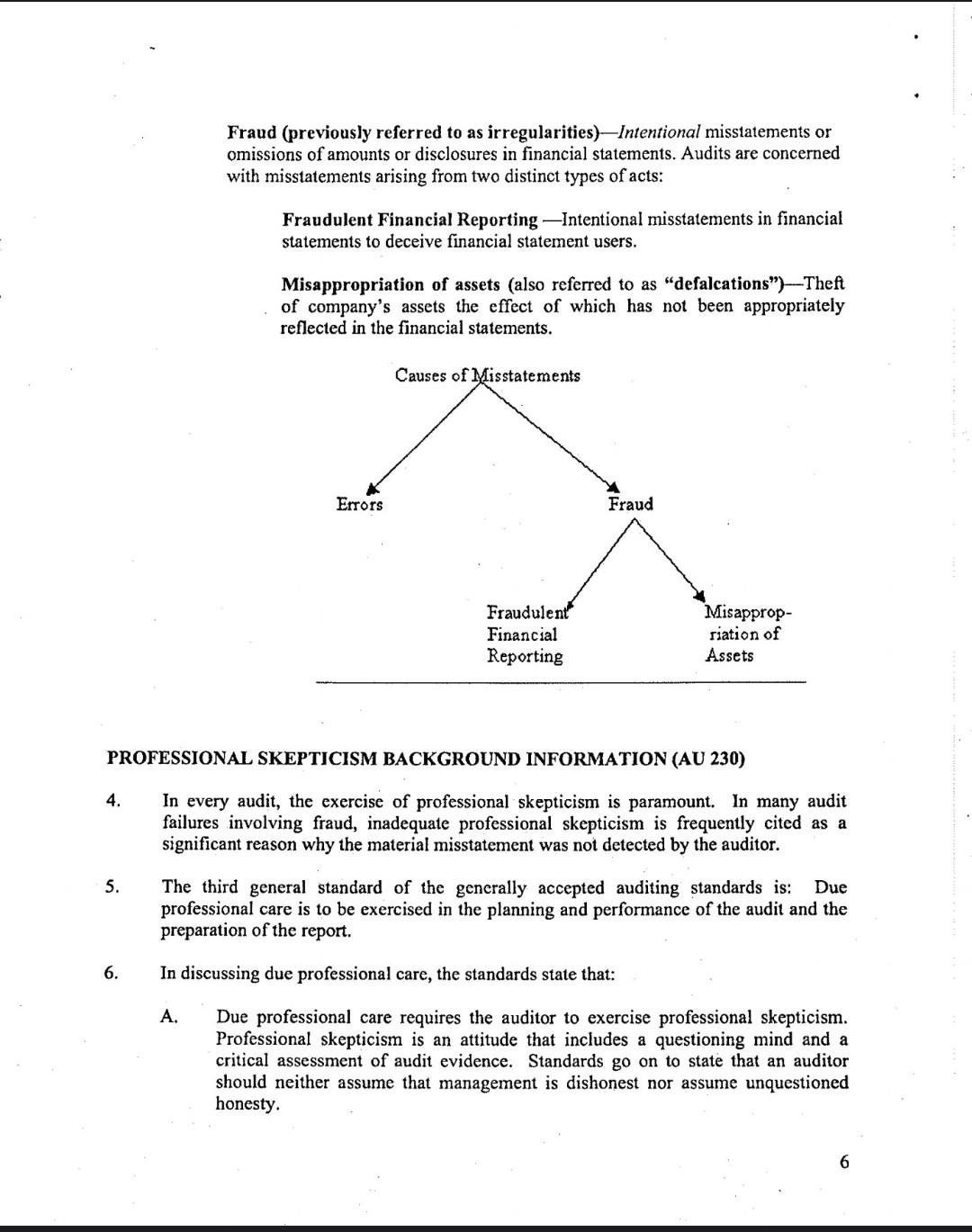

Fraud (previously referred to as irregularities) -Intentional misstatements or omissions of amounts or disclosures in financial statements. Audits are concerned with misstatements arising from two distinct types of acts: Fraudulent Financial Reporting - Intentional misstatements in financial statements to deceive financial statement users. Misappropriation of assets (also referred to as "defalcations")-Theft of company's assets the effect of which has not been appropriately reflected in the financial statements. PROFESSIONAL SKEPTICISM BACKGROUND INFORMATION (AU 230) 4. In every audit, the exercise of professional skepticism is paramount. In many audit failures involving fraud, inadequate professional skepticism is frequently cited as a significant reason why the material misstatement was not detected by the auditor. 5. The third general standard of the generally accepted auditing standards is: Due professional care is to be exercised in the planning and performance of the audit and the preparation of the report. 6. In discussing due professional care, the standards state that: A. Due professional care requires the auditor to exercise professional skepticism. Professional skepticism is an attitude that includes a questioning mind and a critical assessment of audit evidence. Standards go on to state that an auditor should neither assume that management is dishonest nor assume unquestioned honesty. Gathering and objectively evaluating audit evidence requires the auditor to consider the competency and sufficiency of the evidence. Since evidence is gathered and evaluated throughout the audit, professional skepticism should be exercised throughout the audit process. The auditor neither assumes that management is dishonest nor assumes unquestioned honesty. In exercising professional skepticism, the auditor should not be satisfied with less than persuasive evidence because of a belief that management is honestStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Budget Responsibility And National Audit Bill Source Book Edition Current Political Debates Of The UK Parliament 55th Parliament Volume

Authors: Jeff Nelson

1st Edition

3845468017, 978-3845468013