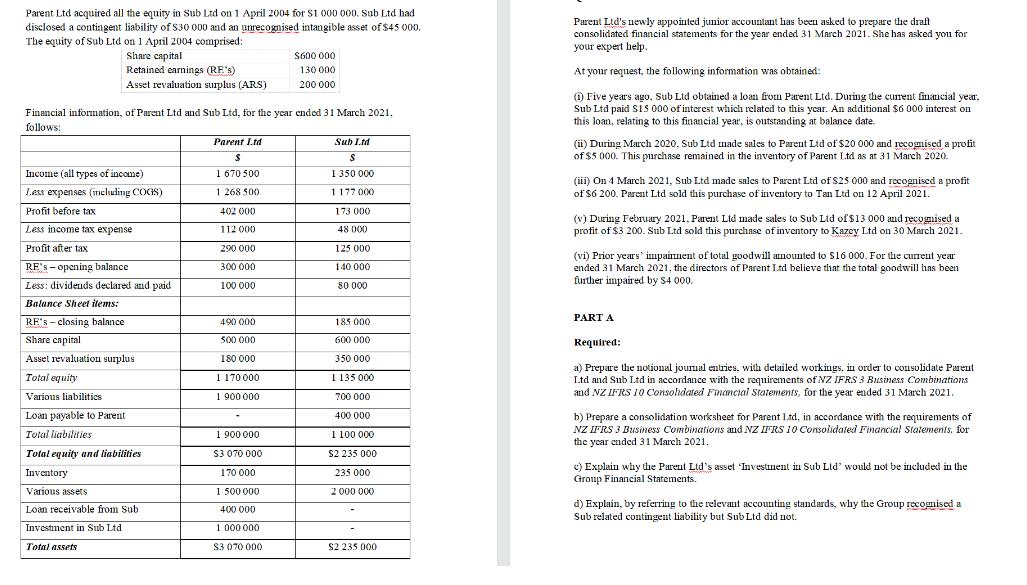

Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

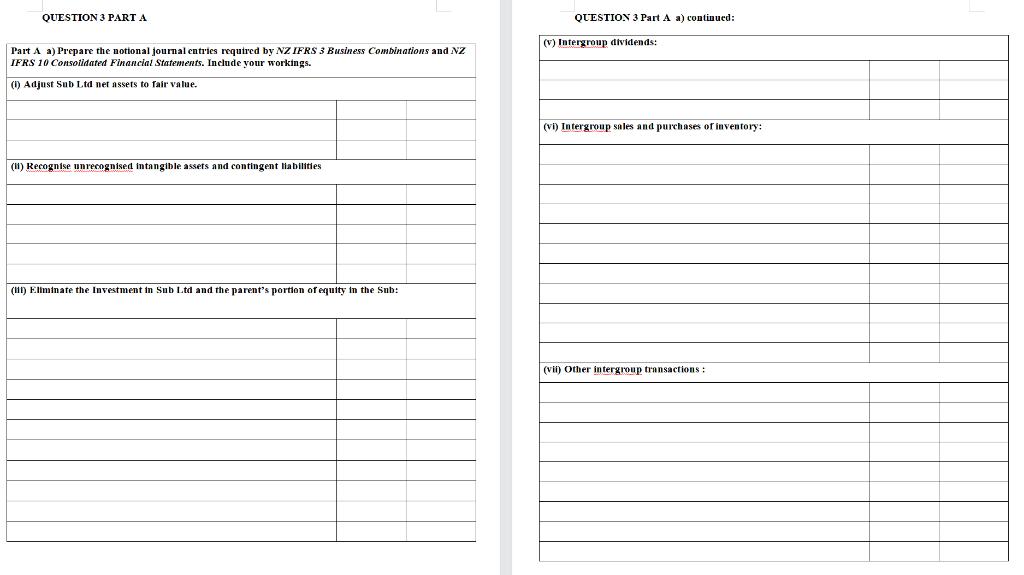

Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000 000. Sub Ltd had disclosed a contingent liability of $30 000 and an unrecognised intangible asset of $45 000. The equity of Sub Ltd on 1 April 2004 comprised: Share capital Retained earnings (RE's) Asset revaluation surplus (ARS) Financial information, of Parent Ltd and Sub Ltd, for the year ended 31 March 2021. follows: Income (all types of income) Less expenses (including COGS) Profit before tax Less income tax expense Profit after tax RE's-opening balance Less: dividends declared and paid Balance Sheet items: RF's closing balance Share capital Asset revaluation surplus Total equity Various liabilities Loan payable to Parent Total liabilities Total equity and liabilities Inventory Various assets Loan receivable from Sub. Investment in Sub Ltd Total assets Parent Ltd $ 1 670 500 1 268 500 402 000 112 000 290 000 300 000 100 000 490 000 500 000 180 000 1 170 000 1900 000 1 900 000 $3 070 000 170 000 1 500 000 400 000 1 000 000 $600 000 130 000 200 000 $3 070 000 Sub Ltd $ 1 350 000 1177 000 173 000 48 000 125 000 140 000 80 000 185 000 600 000 350 000 1 135 000 700 000 400 000 1 100 000 $2 235 000 235 000 2 000 000 $2 235 000 Parent Ltd's newly appointed junior accountant has been asked to prepare the draft consolidated financial statements for the year ended 31 March 2021. She has asked you for your expert help. At your request, the following information was obtained: (1) Five years ago, Sub Ltd obtained a loan from Parent Ltd. During the current financial year. Sub Ltd paid $15 000 of interest which related to this year. An additional $6 000 interest on this loan, relating to this financial year, is outstanding at balance date. (ii) During March 2020, Sub Ltd made sales to Parent Ltd of $20 000 and recognised a profit of $5 000. This purchase remained in the inventory of Parent Ltd as at 31 March 2020. (iii) On 4 March 2021, Sub Ltd made sales to Parent Ltd of $25 000 and recognised a profit of $6 200. Parent Ltd sold this purchase of inventory to Tan Ltd on 12 April 2021. (v) During February 2021, Parent Ltd made sales to Sub Lid of $13 000 and recognised a profit of $3 200. Sub Ltd sold this purchase of inventory to Kazey Ltd on 30 March 2021. (vi) Prior years impainment of total goodwill amounted to $16 000. For the current year ended 31 March 2021, the directors of Parent Ltd believe that the total goodwill has been further impaired by $4 000. PART A Required: a) Prepare the notional joumal entries, with detailed workings, in order to consolidate Parent Ltd and Sub Ltd in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. b) Prepare a consolidation worksheet for Parent Ltd, in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. c) Explain why the Parent Ltd's asset Investment in Sub Ltd' would not be included in the Group Financial Statements. d) Explain, by referring to the relevant accounting standards, why the Group recognised a Sub related contingent liability but Sub Ltd did not. QUESTION 3 PART A Part A a) Prepare the notional journal entries required by NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements. Include your workings. (1) Adjust Sub Ltd net assets fair value. (1) Recognise unrecognised intangible assets and contingent liabilities (111) Eliminate the Investment in Sub Ltd and the parent's portion of equity in the Sub: QUESTION 3 Part A a) continued: (v) Intergroup dividends: (vi) Intergroup sales and purchases of inventory: (vii) Other intergroup transactions: Parent Ltd acquired all the equity in Sub Ltd on 1 April 2004 for $1 000 000. Sub Ltd had disclosed a contingent liability of $30 000 and an unrecognised intangible asset of $45 000. The equity of Sub Ltd on 1 April 2004 comprised: Share capital Retained earnings (RE's) Asset revaluation surplus (ARS) Financial information, of Parent Ltd and Sub Ltd, for the year ended 31 March 2021. follows: Income (all types of income) Less expenses (including COGS) Profit before tax Less income tax expense Profit after tax RE's-opening balance Less: dividends declared and paid Balance Sheet items: RF's closing balance Share capital Asset revaluation surplus Total equity Various liabilities Loan payable to Parent Total liabilities Total equity and liabilities Inventory Various assets Loan receivable from Sub. Investment in Sub Ltd Total assets Parent Ltd $ 1 670 500 1 268 500 402 000 112 000 290 000 300 000 100 000 490 000 500 000 180 000 1 170 000 1900 000 1 900 000 $3 070 000 170 000 1 500 000 400 000 1 000 000 $600 000 130 000 200 000 $3 070 000 Sub Ltd $ 1 350 000 1177 000 173 000 48 000 125 000 140 000 80 000 185 000 600 000 350 000 1 135 000 700 000 400 000 1 100 000 $2 235 000 235 000 2 000 000 $2 235 000 Parent Ltd's newly appointed junior accountant has been asked to prepare the draft consolidated financial statements for the year ended 31 March 2021. She has asked you for your expert help. At your request, the following information was obtained: (1) Five years ago, Sub Ltd obtained a loan from Parent Ltd. During the current financial year. Sub Ltd paid $15 000 of interest which related to this year. An additional $6 000 interest on this loan, relating to this financial year, is outstanding at balance date. (ii) During March 2020, Sub Ltd made sales to Parent Ltd of $20 000 and recognised a profit of $5 000. This purchase remained in the inventory of Parent Ltd as at 31 March 2020. (iii) On 4 March 2021, Sub Ltd made sales to Parent Ltd of $25 000 and recognised a profit of $6 200. Parent Ltd sold this purchase of inventory to Tan Ltd on 12 April 2021. (v) During February 2021, Parent Ltd made sales to Sub Lid of $13 000 and recognised a profit of $3 200. Sub Ltd sold this purchase of inventory to Kazey Ltd on 30 March 2021. (vi) Prior years impainment of total goodwill amounted to $16 000. For the current year ended 31 March 2021, the directors of Parent Ltd believe that the total goodwill has been further impaired by $4 000. PART A Required: a) Prepare the notional joumal entries, with detailed workings, in order to consolidate Parent Ltd and Sub Ltd in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. b) Prepare a consolidation worksheet for Parent Ltd, in accordance with the requirements of NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements, for the year ended 31 March 2021. c) Explain why the Parent Ltd's asset Investment in Sub Ltd' would not be included in the Group Financial Statements. d) Explain, by referring to the relevant accounting standards, why the Group recognised a Sub related contingent liability but Sub Ltd did not. QUESTION 3 PART A Part A a) Prepare the notional journal entries required by NZ IFRS 3 Business Combinations and NZ IFRS 10 Consolidated Financial Statements. Include your workings. (1) Adjust Sub Ltd net assets fair value. (1) Recognise unrecognised intangible assets and contingent liabilities (111) Eliminate the Investment in Sub Ltd and the parent's portion of equity in the Sub: QUESTION 3 Part A a) continued: (v) Intergroup dividends: (vi) Intergroup sales and purchases of inventory: (vii) Other intergroup transactions:

Expert Answer:

Answer rating: 100% (QA)

ANSWER Why Parents Ltds asset Investment in Sub Ltd not included in the group financial statements C... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-0273744443

14th Edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these business communication questions

-

On 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £6,000 cash. The fair value of the net assets in Daughter Ltd was their book value. Required: Prepare the...

-

In August 2018 Delz Ltd acquired all the equity shares of Eba Ltd, a large cable communications provider in Kenya. Eba Ltd is audited by a different audit practice where your firm has no...

-

On 1 July 2023, Gordon Ltd acquired all the issued shares (cum div.) of Henry Ltd for $528000. At that date, the financial statements of Henry Ltd showed the following information. Share capital...

-

The difference between case law and common is which of the following? O Common law creates law and case law interprets existing law. There is no difference. Case law is criminal law and common law is...

-

One of Vasudevan's divisions has above average risk and so a divisional weighted average cost of capital of 20%. This division has current sales of $600,000, operating income of $250,000, total net...

-

Show that Gordan's and Stiemke's theorems are special cases of Tucker's theorem.

-

Wash alumina solids to remove \(\mathrm{NaOH}\) from the entrained liquid. Underflow from the settler tank is \(20.0 \mathrm{vol} \%\) solid and \(80.0 \mathrm{vol} \%\) liquid. Two feeds to the...

-

Multiple Choice Questions 1. A computer manufacturer has two divisions: one serving residential customers and one serving business customers. If an incentive conflict arises between the two...

-

Creating an endowment Personal Finance Problem On completion of her introductory finance course, Marla Le was so pleased with the amount of useful and interesting knowledge she gained that she...

-

Process costing becomes more complicated when there are both beginning and ending work in process (BWIP and EWIP) inventories. The costs stored in BWIP were incurred during the prior period. A...

-

Describe the creation of the Federal Government under the new United States Constitution

-

In the course of auditing the financial statements of the Lowe Company for the year ended December 31, 19X2, you request that your client's attorney furnish a legal representation letter. The...

-

What is the difference between an RFP and an RFQ? Give an example of the appropriate use of each. How does procurement planning differ for government projects versus those in private industry?

-

What are the advantages of resource leveling?

-

In an audit of the Cotula Corporation as at December 31, 19X4, you have learned that the following situation exists. No entry in respect thereto has been made in the accounting records. What entry...

-

What is stakeholder engagement? What can project managers do to engage stakeholders? Can they use any techniques that your teachers have used to engage students in classes? Why or why not?

-

Critically evaluate the effectiveness of government regulation and industry standards in promoting ethical business practices. Discuss the role of stakeholders in holding businesses accountable for...

-

For liquid water the isothermal compressibility is given by; where r and b are functions of temperature only. If 1 kg of water is compressed isothermally and reversibly from I to 500 bar at 60(C. how...

-

(a) On 1 January 20X7 Parent Ltd acquired all the ordinary shares in Daughter Ltd for £16,200 cash. The fair value of the net assets in Daughter Ltd was their book value. (b) The purchase...

-

Summer plc acquired 60% of the common shares of Winter Ltd on 30 September 20X1 and gained control. At the date of acquisition, the balance of retained earnings of Winter was 35,000. At 31 December...

-

(a) The following ratios have been extracted from an analysis of the consolidated accounts of three companies North, South and East: Required: Comment on the respective performance of each of the...

-

Excise taxes are considered regressive because lowerincome people spend a(n) _________ fraction of their incomes on such taxes than do higher-income people.

-

If a higher-income person paid the same taxes as a lower-income person, that tax would be considered _________.

-

Federal income tax is a good example of the _________ principle.

Study smarter with the SolutionInn App