PART 1 Fixed and Variable Cost Determinations Unit Cost Calculations IThe projected cost of a lamp is calculated based upon the projected incleases or decIIPases

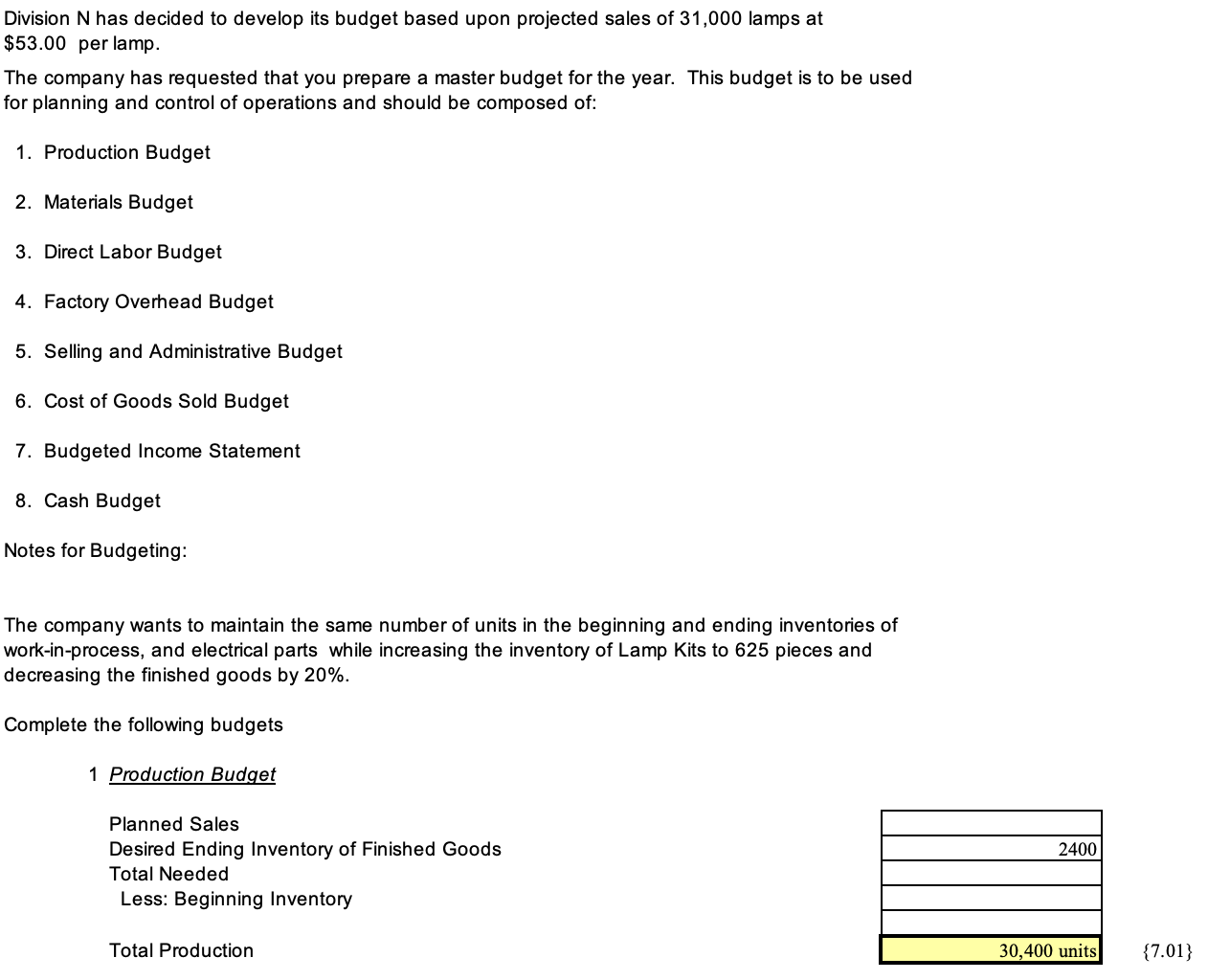

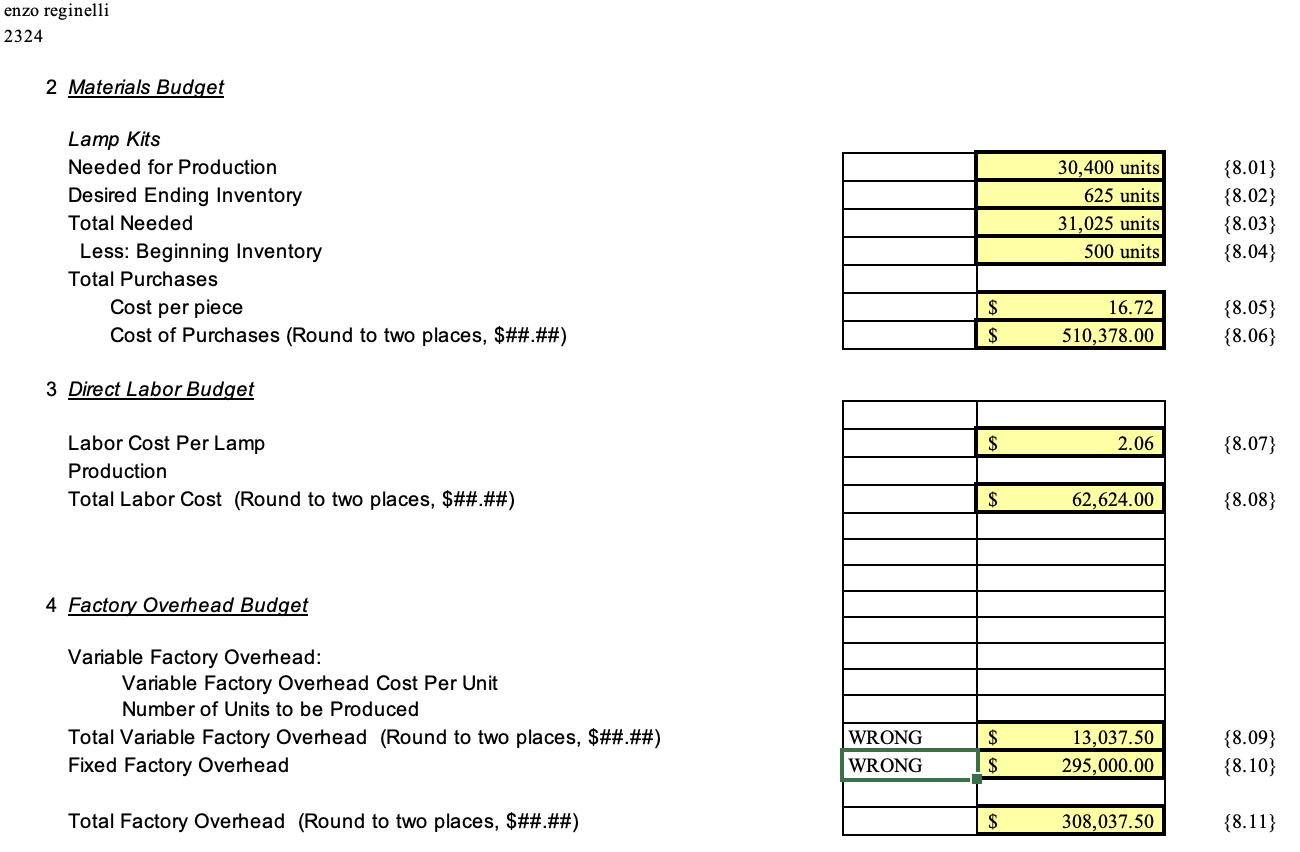

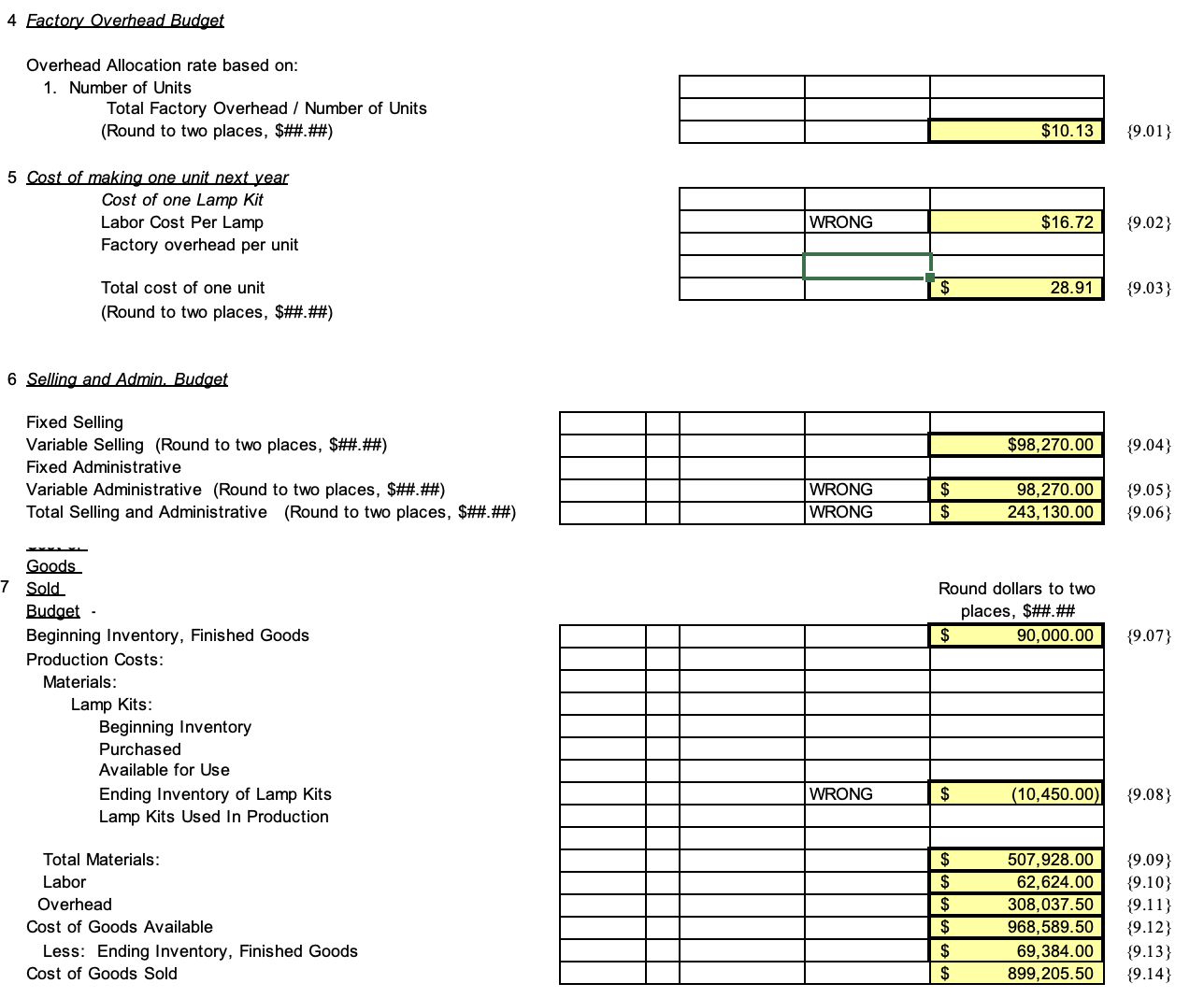

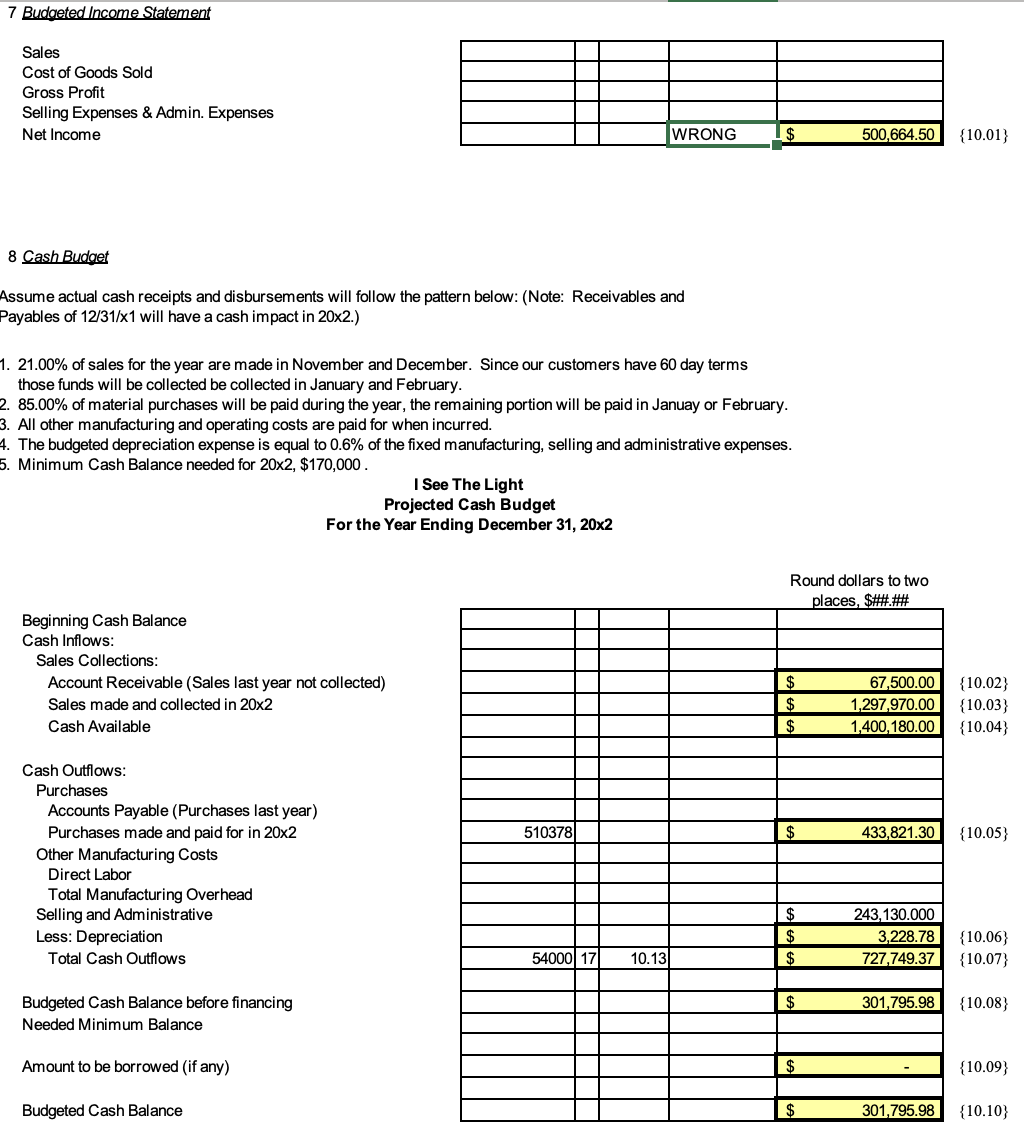

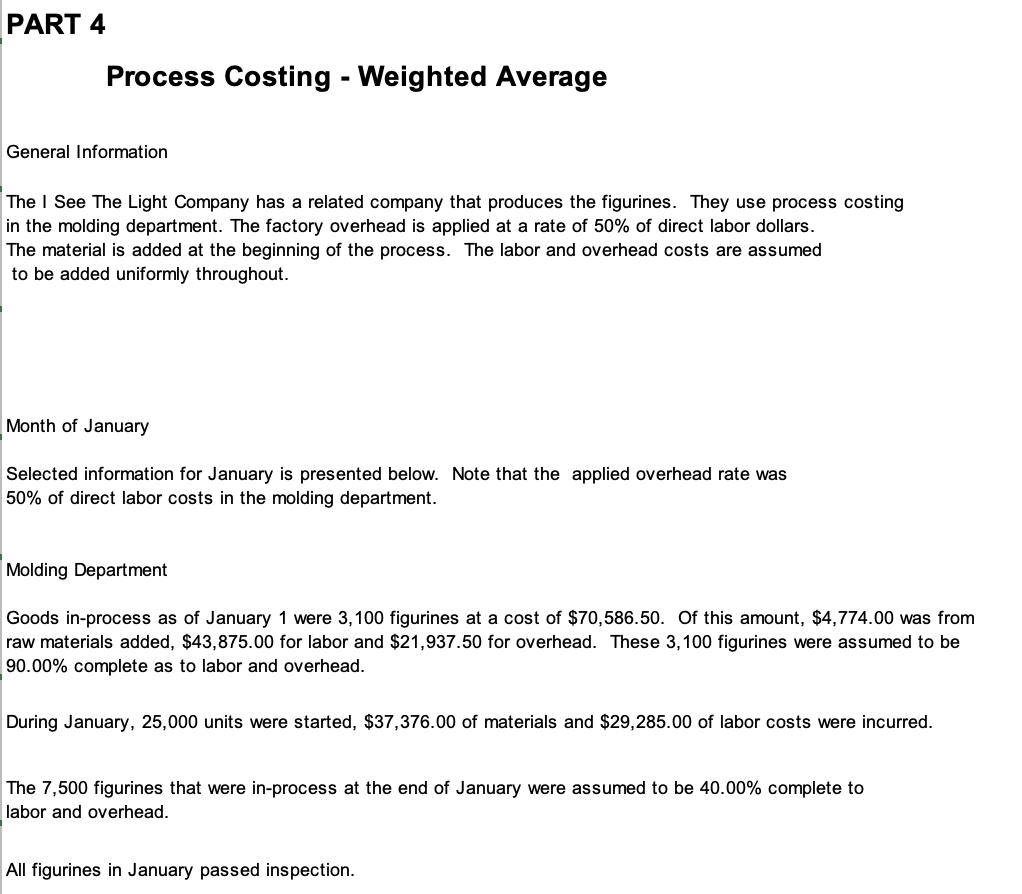

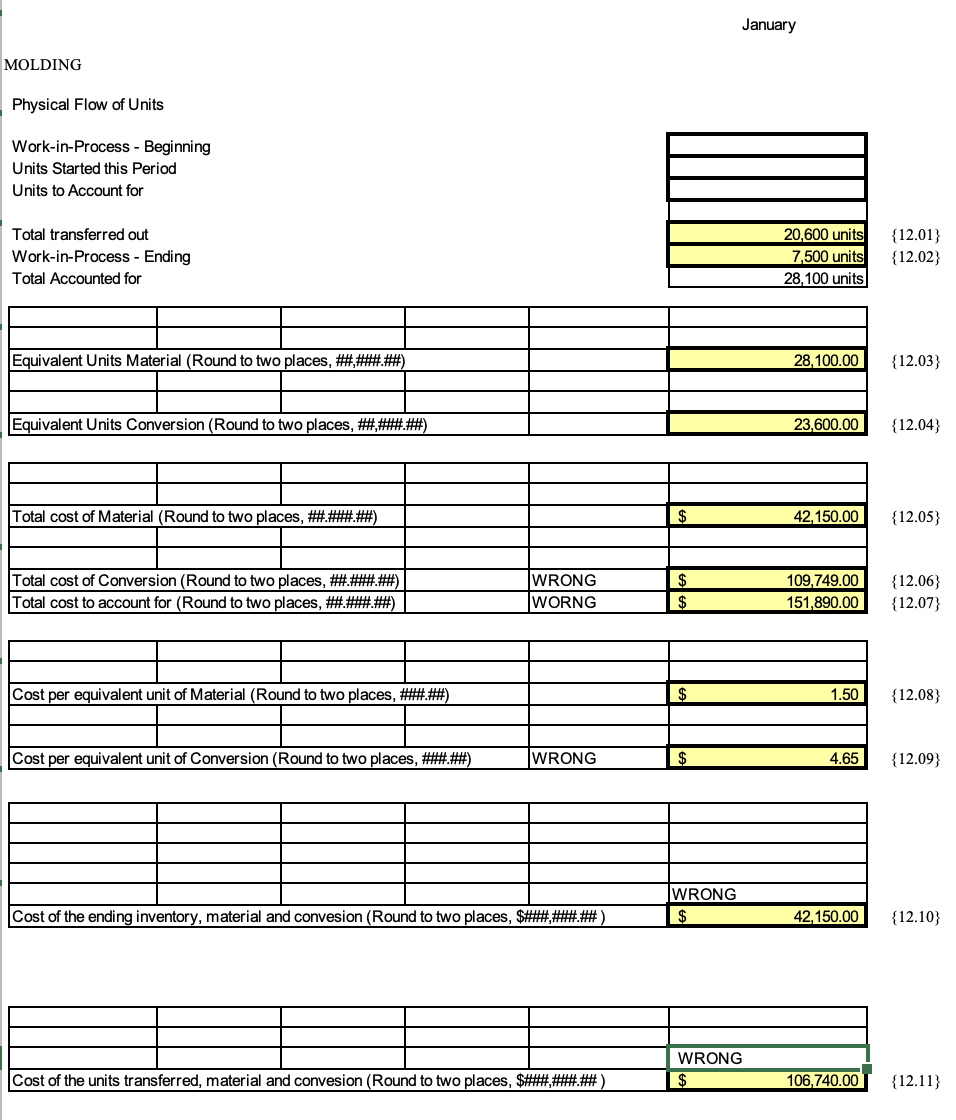

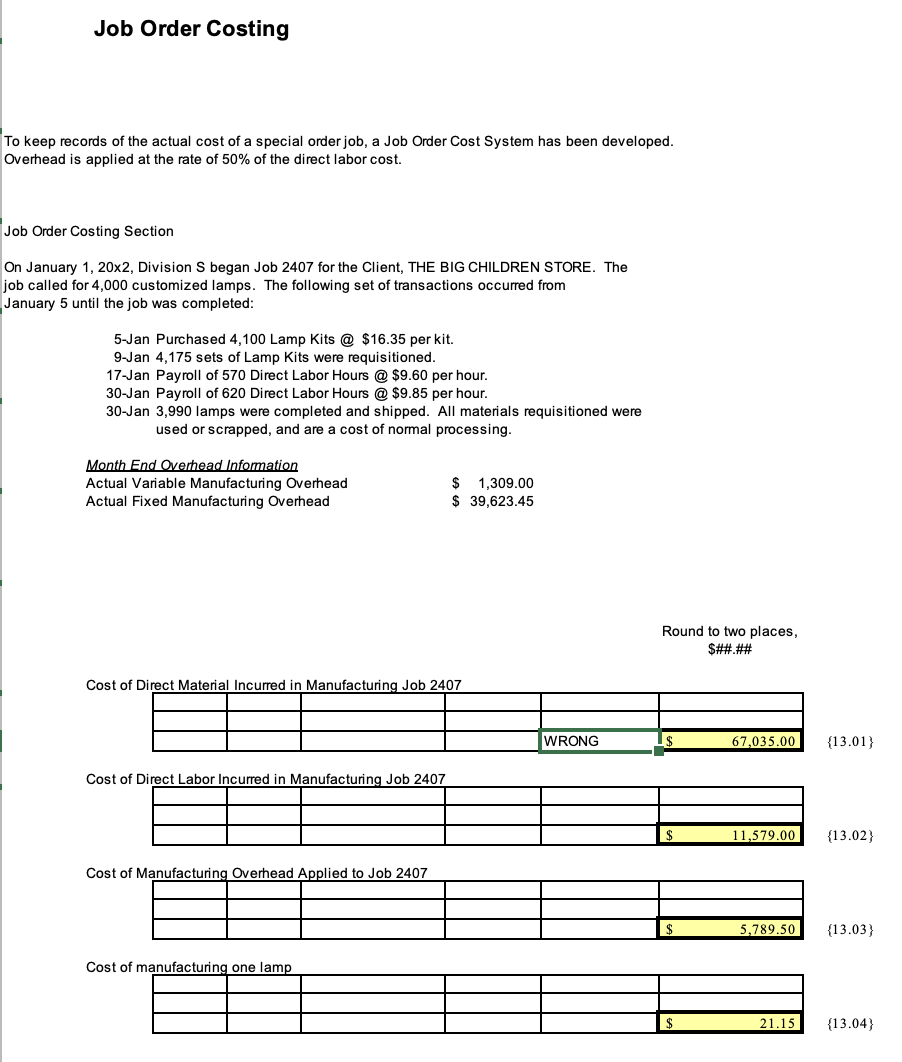

PART 1 Fixed and Variable Cost Determinations Unit Cost Calculations IThe projected cost of a lamp is calculated based upon the projected incleases or decIIPases to current costs. The present costs to manufacture one lamp are: r . Lamp Kit: $16.0000000 per lamp Direct Labor: 2.0000000 per lamp (4 lampsfhr.) Variable Overhead: 2.0000000 per lamp Fixed Overhead: 10.0000000 per lamp (based on normal capacity of 25,000 lamps] Cost per lamp: $30.0000000 per lamp Expected increases for 20x2 IWhen calculating projected increases round to TWO ($0.00) decimal places. 1. Material Costs are expected to increase by 4.50% . 2. Labor Costs are expected to increase by 3.00%. 3. Variable Overhead is expected to increase by 4.00%. 4. Fixed Overhead is expected to increase to $295,000. 5. Fixed Administrative expenses are expected to increase to $50,000. 6. Variable selling expenses (measured on a per lamp basis) are expected to increase by 5.50%. ?'. Fixed selling expenses are expected to be $31,000 in 20x2. 8. Variable administrative expenses (measured a per lamp basis) are expected to increase by 3.00%. On the following schedule develop the following figures: I 1- 20x2 Projected Variable Manufacturing Unit Cost of a lamp. 2- 20x2 Projected Variable Unit Cost per lamp. 3- 20x2 Projected Fixed Costs. I See The Light, Inc Schedule of Projected Costs Variable Manufacturing Unit Cost 20x1 Cost Projected Percent 20x2 Cost Rounded to 2 Increase Decimal Places Lamp Kit 16 4.50% $16.72 (4.01} Labor 3.00% 2.06 (4.02} NN Variable Overhead 4.00% $2.08 (4.03} Projected Variable Manufacturing Cost Per Unit 30 $20.86 (4.04} Total Variable Cost Per Unit 20x1 Cost Projected Percent 20x2 Cost Rounded to 2 Increase Decimal Places Variable Selling 3.17 (4.05} N W Variable Administrative 2.06 (4.06} Projected Variable Manufacturing Unit Cost 26.86 (4.04} Projected Total Variable Cost Per Unit 26.09 (4.07} Schedule of Fixed Costs 20x1 Cost 20x2 Cost Projected Percent Increase Fixed Overhead 10 wrong $ 1.80 (4.08) (normal capacity of lamps @ _) Fixed Selling wrong $ 2.00 (4.09) Fixed Administrative wrong 1.24 (4.10} Projected Total Fixed Costs $ 15.04 (4.11 }PART 2 Cost Volume Relationships - Profit Planning Big Al is about to begin work on the budget for 20x2 and they have requested that you prepare an analysis based on the following assumptions. Note: Remember, that we cannot sell part of a lamp, therefore to find the number of units you have to round up to the next complete unit. Furthuremore, to find the required sales in dollars it may be easier to find the number of units and then multiply by the selling price per unit. For 20x2 the selling price per lamp will be $45.00. What is the projected contribution margin and contribution margin ratio for each lamp sold? Contribution Margin per unit (Round to two places, $##.##) $18.91 (5.01} Contribution Margin Ratio (Round to four places, % is two of those places ##.##%) 42.02% (5.02) 2. For 20x2 the selling price per lamp will be $45.00. The desired net income in 20x2 is $200,000 . What would sales in units have to be in 20x2 to reach the profit goal? WRONG Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 30,461 units (5.03} 3. For 20x2 the selling price per lamp will be $45.00. If the fixed cost increase by $55,000.00 how many lamps must be sold to breakeven? WRONG Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 22,793 units (5.04)4. For 20x2 the selling price per lamp will be $45.00. If the variable cost increase by $5.50 a unit how many lamps must be sold to breakeven? WRONG Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 28,039 units (6.01} 5. For 20x2 the selling price per lamp will be $45.00. If the variable cost decreased by $5.50 a unit how many lamps must be sold to breakeven? WRONG Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 15,404 units (6.02} 6. If for 20x2 the selling price per lamp is increased to $50.50 a unit how many lamps must be sold to breakeven? WRONG Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 15,403 units (6.03} 7. If for 20x2 the selling price per lamp is decreased to $39.50 a unit how many lamps must be sold to breakeven? WRONG Breakeven sales in units (Since we cannot sell part of a unit round up to the next unit if needed) 28,039 units {6.04}Division N has decided to develop its budget based upon projected sales of 31.000 lamps at $53.00 per lamp. The company has requested that you prepare a master budget for the year. This budget is to be used for planning and control of operations and should be composed of: 1. Production Budget 2. Materials Budget 3. Direct Labor Budget 4. Factory Overhead Budget 5. Selling and Administrative Budget 6. Cost of Goods Sold Budget 7. Budgeted Income Statement 8. Cash Budget Notes for Budgeting: The company wants to maintain the same number of units in the beginning and ending inventories of work-inprocess. and electrical parts while increasing the inventory of Lamp Kits to 625 pieces and decreasing the finished goods by 20%. Complete the following budgets 1 Production Budget Planned Sales Desired Ending Inventory of Finished Goods Total Needed Less: Beginning Inventory Total Production 30,400 units {7.01} cnzo rcginclli 2324 2 Materials Budget Lamp Kits Needed for Production {8.01} Desired Ending Inventory {8.02} Total Needed {8.03} Less: Beginning Inventory {8.04} Total Purchases Cost per piece _ {8.05} Cost of Purchases (Round to two places, $##.##) {8.06} 3 W _ Labor Cost Per Lamp {8.07} Production _ Total Labor Cost (Round to two places, $##.##) {8.08} 4 Factory Overhead Budget Variable Factory Overhead: Variable Factory Overhead Cost Per Unit Number of Units to be Produced Total Variable Factory Overhead (Round to two places. $##.##) {8.09} Fixed Factory Overhead WRONG S 295,000.00 {8.10} Total Factory Overhead (Round to two places, $##.##) $ 308,037.50 {8.11} 4W Overhead Allocation rate based on: 1. Number of Units Total Factory Overhead I Number of Units (Round to two places, $##.##) 5 : f E . . Cost of one Lamp Kit Labor Cost Per Lamp Factory overhead per unit Total cost of one unit (Round to two places, $##.#) 5555' 535.5 Fixed Selling Variable Selling (Round to two places, swm _- Fixed Administrative -_ Variable Administrative (Round to two places, $##.##) _- Total Selling and Administrative (Round to two places, $##.##) _- Goods. 7 SoLgL Round dollars to two Budget - places, $##.## Beginning Inventory, Finished Goods _- Production Costs: Materials: Lamp Kits: Beginning Inventory Purchased Available for Use Ending Inventory of Lamp Kits Lamp Kits Used In Production Total Materials: Labor Overhead Cost of Goods Available Less; Ending Inventory. Finished Goods Cost of Goods Sold {9.0L} {9.02} {9.03} {9.04} {9.05} {9.06} {9.07} {9.03} {9.09} {9w} {9.I l I {9.I2} {9.I3} {9.I4} 7 Budgeted Income Statement Sales Cost of Goods Sold Gross Profit Selling Expenses & Admin. Expenses Net Income WRONG $ 500,664.50 {10.01} 8 Cash Budget Assume actual cash receipts and disbursements will follow the pattern below: (Note: Receivables and Payables of 12/31/x1 will have a cash impact in 20x2.) 1. 21.00% of sales for the year are made in November and December. Since our customers have 60 day terms those funds will be collected be collected in January and February. 85.00% of material purchases will be paid during the year, the remaining portion will be paid in Januay or February. 3. All other manufacturing and operating costs are paid for when incurred. . The budgeted depreciation expense is equal to 0.6% of the fixed manufacturing, selling and administrative expenses. . Minimum Cash Balance needed for 20x2, $170,000. I See The Light Projected Cash Budget For the Year Ending December 31, 20x2 Round dollars to two places, $##.## Beginning Cash Balance Cash Inflows: Sales Collections: Account Receivable (Sales last year not collected) 67,500.00 [10.02} Sales made and collected in 20x2 1,297,970.00 (10.03) Cash Available 1,400, 180.00 {10.04} Cash Outflows: Purchases Accounts Payable (Purchases last year) Purchases made and paid for in 20x2 510378 133,821.30 {10.05} Other Manufacturing Costs Direct Labor Total Manufacturing Overhead Selling and Administrative $ 243, 130.000 Deprecia $ 3,228.78 [10.06} Total Cash Outflows 54000 17 10.13 727,749.37 {10.07} Budgeted Cash Balance before financing $ 301,795.98 {10.08} Needed Minimum Balance Amount to be borrowed (if any) (10.09) Budgeted Cash Balance 301,795.98 {10.10PART 4 Process Costing - Weighted Average General Information IThe I See The Light Company has a related company that produces the figurines. They use process costing in the molding department. The factory overhead is applied at a rate of 50% of direct labor dollars. The material is added at the beginning of the process. The labor and overhead costs are assumed to be added uniformly throughout. IMonth of January Selected information for January is presented below. Note that the applied overhead rate was 50% of direct labor costs in the molding department. I Molding Department Goods in-process as of January 1 were 3,100 figurines at a cost of $70,586.50. Of this amount, $4,774.00 was from raw materials added, $43,875.00 for labor and $21,937.50 for overhead. These 3,100 figurines were assumed to be .90'00% complete as to labor and overhead. During January, 25,000 units were started, $37,376.00 of materials and $29,285.00 of labor costs were incurred. The 7,500 figurines that were in-process at the end of January were assumed to be 40.00% complete to Ilabor and overhead. All figurines in January passed inspection. January MOLDING Physical Flow of Units Work-in-Process - Beginning Units Started this Period Units to Account for Total transferred out 20,600 units (12.01} Work-in-Process - Ending 7,500 units {12.02} Total Accounted for 28, 100 units Equivalent Units Material (Round to two places, ##,###.## 28, 100.00 {12.03} Equivalent Units Conversion (Round to two places, ##,###.##) 23,600.00 (12.04) Total cost of Material (Round to two places, ##.###.## $ 42, 150.00 {12.05} Total cost of Conversion (Round to two places, ##.###.##) WRONG 109,749.00 (12.06) Total cost to account for ( Round to two places, ##.###.##) WORNG 151,890.00 {12.07} Cost per equivalent unit of Material (Round to two places, ###.##) $ 1.50 (12.08} Cost per equivalent unit of Conversion (Round to two places, ###.##) WRONG $ 4.65 {12.09} WRONG Cost of the ending inventory, material and convesion (Round to two places, $###,###.##) $ 42, 150.00 (12.10} WRONG Cost of the units transferred, material and convesion (Round to two places, $###,###.##) $ 106,740.00 {12.11}Job Order Costing To keep records of the actual cost of a special order job, a Job Order Cost System has been developed. Overhead is applied at the rate of 50% of the direct labor cost. Job Order Costing Section On January 1, 20x2, Division S began Job 2407 for the Client, THE BIG CHILDREN STORE. The job called for 4,000 customized lamps. The following set of transactions occurred from January 5 until the job was completed: 5-Jan Purchased 4, 100 Lamp Kits @ $16.35 per kit. 9-Jan 4,175 sets of Lamp Kits were requisitioned 17-Jan Payroll of 570 Direct Labor Hours @ $9.60 per hour. 30-Jan Payroll of 620 Direct Labor Hours @ $9.85 per hour. 30-Jan 3,990 lamps were completed and shipped. All materials requisitioned were used or scrapped, and are a cost of normal processing. Month End Overhead Information Actual Variable Manufacturing Overhead 1,309.00 Actual Fixed Manufacturing Overhead 39,623.45 Round to two places, S##.## Cost of Direct Material Incurred in Manufacturing Job 2407 WRONG 67,035.00 (13.01} Cost of Direct Labor Incurred in Manufacturing Job 2407 $ 11,579.00 (13.02} Cost of Manufacturing Overhead Applied to Job 2407 5,789.50 (13.03} Cost of manufacturing one lamp 21.15 (13.04}Standard Job Order Costing - Variance Analysis Special order lamps are manufactured in division S. Because of the precise nature of the process a standard cost system has been developed. The following standards are used for the special orders: Standards Lamp Kits $ 16.000000 per lamp Direct Labor 2.400000 per lamp (4 lamps/hr.) Variable Overhead 0.250000 per lamp (4 lamps/hr.) ** Fixed Overhead 10.000000_per lamp Total $ 28.650000 ** Fixed overhead is based on expected production of 4,010 customized lamps each month. To keep records of the actual cost of a job, a Job Order Cost System has been developed. Entries are made to the Job Order System at actual cost (overhead is applied based on actual labor hours) while entries are made to the accounting system at standard. Variance analysis is used to analyze the differences. Job Order Costing Section On January 1, 20x2, Division S began Job 1101 for the Client, THE BIG CHILDREN STORE. The job called for 4,000 customized lamps. The following set of transactions occurred from January 5 until the job was completed: 5-Jan Purchased 4, 100 Lamp Kits @ $16.35 per kit. 9-Jan 4,175 sets of Lamp Kits were requisitioned. 17-Jan Payroll of 570 Direct Labor Hours @ $9.60 per hour. 30-Jan Payroll of 620 Direct Labor Hours @ $9.85 per hour. 30-Jan 3,990 lamps were completed and shipped. All materials requisitioned were used or scrapped. Month End Overhead Information Actual Variable Overhead 1,309.00 Actual Fixed Overhead 39,623.45How many Lamps were completed? Note: Show favorable variances as negative numbers Round dollars to two places, $##.## What was the total material price variance for the Lamp Kits purchased? $ 1,435.00 {15.01} What was the material usage variance for Lamp Kits? $ 2,960.00 {15.02} What was the direct labor efficiency variance ? $ 1,848.00 {15.03} What was the direct labor rate variance? $ 155.00 {15.04}Note: Show favorable variances as negative numbers What was the variable overhead efficiency variance ? 192.50 {16.01} What was the variable OH spending variance ? 119.00 {16.02} What is the fixed OH volume (denominator) variance? 200.00 {16.03} What is the fixed OH spending variance? (476.55) {16.04}Capital Decision Making Big Al gives his worker's a one hour lunch and two fifteen minute breaks each day. He believes that a cold soda machine would be appreciated by his workers, and an appreciated worker is a good worker. He has priced a machine at a national member only warehouse for $2,200. The machine should be usable for 5 years, after which it would be inefficient, obsolete and would have to be disposed of at the lump. Big Al believes that 10 cans a day will be purchased. The plant is open five days a week, 50 weeks per year. A case of soda (24 cans) costs $6.48 and Big Al believes that a price of $.70 per can would win him good will. What is the estimated annual sales in cans of soda? 2,500 cans (17.01} What is the contribution margin per can of soda? (rounded to two places, $#.##) I $ 0.43 (17.02} How many cans of soda must be sold each year to breakeven? (Round up to zero places, ###,### cans) WRONG 5,116 cans (17.03} Annual incremental cash inflows from the soda machine? (rounded to two places, $#.##) $ 1,075.00 (17.04} What is the payback period in years? (rounded to two places, #.## years) 2.05 years (17.05} If the time value of money is 12% per year what is the net present value? Use the tables on page 18. $ 1,675.38 (17.06} What is the internal rate of return. Pick the closest interest rate from the tables on page 18. 40.00% (17.07}| See The Light Projected Income Statement For the Period Ending December 31. 20x1 Sales 25,000 lamps @ $45.00 $ 1,125,000.00 Cost of Goods Sold @ $30.00 T50,000.00 Gross Profit $ 3?5,000.00 Selling Expenses: Fixed $ 23,000.00 Variable (Commission perunit) @ $3.00 75,000.00 $ 98,000.00 Administrative Expenses: Fixed $ 42,000.00 Variable @ $2 .00 50,000.00 92 ,000.00 Total Selling and Administrative Expenses: 190,000.00 Net Profit $ 185,000.00 | See The Light Projected Balance Sheet As of December 31. 20x1 CurrentAssets Cash $ 34,710.00 Accounts Receivable 67,500.00 Inventory Raw Material Lamp Kits 500 @ $16.00 8,000.00 Work in Process 0 Finished Goods 3000 @ $30.00 90,000.00 Total Current Assets $ 200,210.00 Fixed .A S sets Equipment $ 20,000.00 Accumulated Depreciation 6,800.00 Total Fixed Assets 1 3,200.00 Total Assets $ 213,410.00 Current Liabilities Accounts Payable I S 54.000.00 II Total Liabilities $ 54,000.00 Stockholder's Equity Common Stock $ 12,000.00 Retained Earnings 14?,410.00 Total Stockholders Equity 159 410.00 Total Liabilities and Stockholder's Equity $ 213,410.00

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance